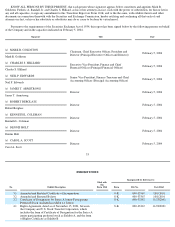

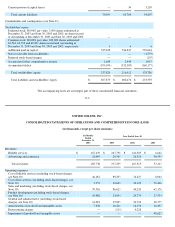

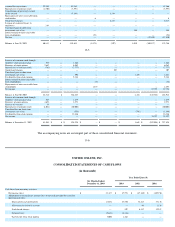

Classmates.com 2003 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2003 Classmates.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

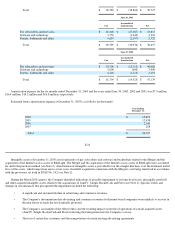

F-10

asset is impaired include significant decreases in the market value of an asset, significant underperformance relative to expected historical or

projected future results of operations, a change in the extent or manner in which an asset is used, significant declines in the Company's stock

price for a sustained period, shifts in technology, loss of key management or personnel, changes in the Company's operating model or strategy

and competitive forces.

If events and circumstances indicate that the carrying amount of an asset may not be recoverable and the expected undiscounted future

cash flows attributable to the asset are less than the carrying amount of the asset, an impairment loss equal to the excess of the asset's carrying

value over its fair value is recorded. Fair value is determined based on the present value of estimated expected future cash flows using a

discount rate commensurate with the risk involved, quoted market prices or appraised values, depending on the nature of the assets. During the

year ended June 30, 2001, the Company recorded an impairment charge of $48.6 million (see Note 4).

Goodwill— The Company adopted SFAS No. 142, Goodwill and Other Intangible Assets , on July 1, 2002. Under SFAS No. 142,

goodwill is no longer amortized, but is tested for impairment at a reporting unit level on an annual basis and between annual tests if an event

occurs or circumstances change that would more likely than not reduce the fair value of a reporting unit below its carrying amount. Events or

circumstances which could trigger an impairment review include a significant adverse change in legal factors or in the business climate, an

adverse action or assessment by a regulator, unanticipated competition, a loss of key personnel, significant changes in the manner of our use of

the acquired assets or the strategy for our overall business, significant negative industry or economic trends, significant declines in our stock

price for a sustained period or significant underperformance relative to expected historical or projected future results of operations. For

purposes of financial reporting and impairment testing in accordance with SFAS No. 142, the Company operates in one principal business

segment, a provider of Internet access services.

In testing for a potential impairment of goodwill, the estimated fair value of the Company is compared with book value, including

goodwill. If the estimated fair value exceeds book value, goodwill is considered not to be impaired and no additional steps are necessary. If,

however, the fair value of the Company is less than book value, then the carrying amount of the goodwill is compared with its implied fair

value. The estimate of implied fair value of goodwill may require independent valuations of certain internally generated and unrecognized

intangible assets such as our pay subscriber base, software and technology and patents and trademarks. If the carrying amount of our goodwill

exceeds the implied fair value of that goodwill, an impairment loss would be recognized in an amount equal to the excess. In accordance with

SFAS No. 142, the Company performed a goodwill impairment test during the June 2003 quarter and concluded that, at that time, there was no

impairment of goodwill. There were no events or changes in circumstances that triggered an impairment test in the six months ended

December 31, 2003.

The Company recorded a $1.4 million reduction in goodwill during the December 2003 quarter in connection with the release of the

deferred tax valuation allowance (see Note 4).

Business Combinations —All of the Company's acquisitions have been accounted for as purchase business combinations. Under the

purchase method of accounting, the cost, including transaction costs, is allocated to the underlying net assets, based on their respective

estimated fair values. The excess of the purchase price over the estimated fair values of the net assets acquired is recorded as goodwill.

The judgments made in determining the estimated fair value and expected useful lives assigned to each class of assets and liabilities

acquired can significantly impact net income. Consequently, to the extent a longer-lived asset is ascribed greater value under the purchase

method than a shorter-lived asset, there may be less amortization recorded in a given period.

F-11

Determining the fair value of certain assets and liabilities acquired is subjective in nature and often involves the use of significant

estimates and assumptions. The Company utilizes a one-

year period following the consummation of acquisitions to finalize estimates of the fair

value of assets and liabilities acquired. Two areas, in particular, that require significant judgment are estimating the fair value and related useful

lives of identifiable intangible assets. To assist in this process, the Company may obtain appraisals from valuation specialists for certain

intangible assets. While there are a number of different methods used in estimating the value of acquired intangibles, there are two approaches

primarily used: the discounted cash flow and market comparison approaches. Some of the more significant estimates and assumptions inherent

in the two approaches include: projected future cash flows (including timing); discount rate reflecting the risk inherent in the future cash flows;

perpetual growth rate; determination of appropriate market comparables; and the determination of whether a premium or a discount should be

applied to comparables. Most of the above assumptions are made based on available historical information.

Revenue Recognition —The Company applies the provisions of SEC Staff Accounting Bulletin ("SAB") No. 104,

Revenue Recognition in

Financial Statements,

which provides guidance on the recognition, presentation and disclosure of revenue in financial statements filed with the

SEC. SAB No. 104 outlines the basic criteria that must be met to recognize revenue and provides guidance for disclosure related to revenue

recognition policies. In general, the Company recognizes revenue related to its billable services and advertising products when (i) persuasive