Cigna 2015 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2015 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

PART II

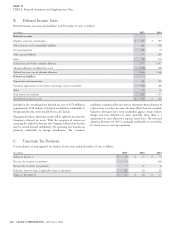

ITEM 8. Financial Statements and Supplementary Data

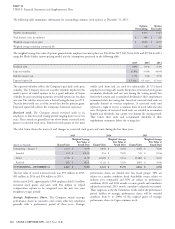

Derivative Financial Instruments

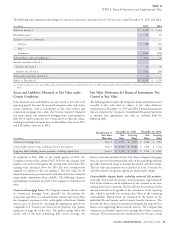

The Company uses derivative financial instruments to manage the

Interest Rate Fair Value Hedges.

characteristics of investment assets (such as duration, yield, currency

The Company entered into centrally-cleared interest rate swap

and liquidity) to meet the varying demands of the related insurance

contracts to convert a portion of the interest rate exposure on its

and contractholder liabilities (such as paying claims, investment

long-term debt from fixed to variable rates to more closely align

returns and withdrawals) and to hedge interest rate risk of its

interest expense with interest income received on its cash equivalent

long-term debt. The Company has written and purchased GMIB

and short-term investment balances. The variable rates are

reinsurance contracts in its run-off reinsurance business that are

benchmarked to LIBOR.

accounted for as freestanding derivatives. For information on the

Company’s accounting policy for derivative financial instruments, see Using fair value hedge accounting, the fair values of the swap contracts

Note 2. Derivatives in the Company’s separate accounts are excluded are reported in other assets, including other intangibles or accounts

from the following discussion because associated gains and losses payable, accrued expenses and other liabilities. As the critical terms of

generally accrue directly to separate account policyholders. these swaps match those of the long-term debt being hedged, the

carrying value of the hedged debt is adjusted to reflect changes in its

Collateral and termination features. The Company routinely fair value driven by LIBOR. The effects of those adjustments on other

monitors exposure to credit risk associated with derivatives and operating expenses are offset by the effects of corresponding changes

diversifies the portfolio among approved dealers of high credit quality in the swaps’ fair value, including interest expense for the difference

to minimize this risk. As of December 31, 2015, the Company had between the variable and fixed interest rates.

$16 million in cash on deposit representing the upfront margin

required for the Company’s centrally-cleared derivative instruments. Under the terms of these contracts, the Company provides upfront

Certain of the Company’s over-the-counter derivative instruments margin and settles fair value changes and net interest between variable

contain provisions requiring either the Company or the counterparty and fixed interest rates daily with the clearinghouse. Net interest cash

to post collateral or demand immediate payment depending on the flows are reported in operating activities.

amount of the net liability position and predefined financial strength As of December 31, 2015 and 2014, the notional values of these

or credit rating thresholds. Collateral posting requirements vary by derivative instruments were $750 million.

counterparty. The net asset or liability positions of these derivatives

were not material as of December 31, 2015 or 2014. As of and for the years ended December 31, 2015 and 2014, the

effects of these derivative instruments on the Consolidated Financial

Statements were not material.

Investment Cash Flow Hedges.

The Company uses interest rate, foreign currency, and combination

GMIB.

(interest rate and foreign currency) swap contracts to hedge the

interest and foreign currency cash flows of its fixed maturity bonds to The Company’s run-off reinsurance business has written reinsurance

match associated insurance liabilities. contracts with issuers of variable annuities that provide annuitants

with certain guarantees of minimum income benefits resulting from

Using cash flow hedge accounting, fair values are reported in other the level of variable annuity account values compared with a

long-term investments or accounts payable, accrued expenses and contractually guaranteed amount (‘‘GMIB liabilities’’). According to

other liabilities. Changes in fair value are reported in accumulated the contractual terms of the written reinsurance contracts, payment by

other comprehensive income and amortized into net investment the Company depends on the actual account value in the underlying

income or reported in other realized investment gains and losses as mutual funds and the level of interest rates when the contractholders

interest or principal payments are received. elect to receive minimum income payments. The Company has

Under the terms of these various contracts, the Company periodically purchased retrocessional coverage (‘‘GMIB assets’’) for these contracts,

exchanges cash flows between variable and fixed interest rates or including the agreement with Berkshire in 2013, effectively exiting

between two currencies for both principal and interest. Foreign this business. See Note 7 for further details.

currency and combination swaps are primarily Euros, Australian The fair value effects of GMIB contracts on the financial statements

dollars, Canadian dollars, Japanese yen and British pounds and have are included in Note 10 and their volume of activity is included in

terms for periods of up to six years. Net interest cash flows are Note 23. Cash flows on these contracts are reported in operating

reported in operating activities. activities.

The notional values of these cash flow swaps were $131 million as of

December 31, 2015 and $145 million as of December 31, 2014.

GMDB and GMIB Hedge Programs.

As of and for the years ended December 31, 2015 and 2014, the The Company’s dynamic hedge programs were discontinued at the

effects of these derivative instruments on the Consolidated Financial time of the Berkshire reinsurance transaction in 2013. These hedge

Statements were not material. No amounts were excluded from the programs generated losses (included in other revenues) of $39 million

assessment of hedge effectiveness and no gains or losses were in 2013.

recognized due to hedge ineffectiveness.

94 CIGNA CORPORATION - 2015 Form 10-K

NOTE 12