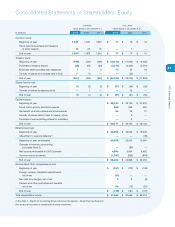

CVS 2013 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2013 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

67

2013 Annual Report

New Accounting Pronouncements

In July 2012, the FASB issued Accounting Standards Update (“ASU”) 2012-02,

Testing Indefinite-Lived Intangible

Assets for Impairment

(“ASU 2012-02”). ASU 2012-02 allows entities to use a qualitative approach to determine

whether the existence of events and circumstances indicates that it is more likely than not that the indefinite-lived

intangible asset is impaired. If, after assessing the totality of events and circumstances, an entity concludes that it

is not more likely than not that the indefinite-lived intangible asset is impaired, then the entity is not required to take

further action. However, if an entity concludes otherwise, then it is required to determine the fair value of the indefi-

nite-lived intangible asset and perform the quantitative impairment test by comparing the fair value with the carrying

amount and recognize an impairment loss, if any, to the extent the carrying value exceeds its fair value. ASU 2012-02

is effective for annual and interim impairment tests performed for fiscal years beginning after September 15, 2012.

The adoption of ASU 2012-02 did not have a material effect on the Company’s consolidated financial statements.

In February 2013, the FASB issued ASU 2013-02,

Reporting of Amounts Reclassified Out of Accumulated Other

Comprehensive Income

(“ASU 2013-02”). ASU 2013-02 adds new disclosure requirements for items reclassified

out of accumulated other comprehensive income. The additional disclosures include: (1) changes in accumulated

other comprehensive income balances by component and (2) significant items reclassified out of accumulated other

comprehensive income. The changes in accumulated other comprehensive income balance by component will be

disaggregated to separately present reclassification adjustments and current-period other comprehensive income.

Significant items reclassified out of accumulated other comprehensive income by component are required to be

presented either on the face of the statement of income or as separate disclosure in the notes to the financial state-

ments. These additional disclosures may be presented before-tax or net-of-tax as long as the income tax benefit or

expense attributed to each component of other comprehensive income and reclassification adjustments is presented

in the financial statement or in the notes to the financial statements. ASU 2013-02 is effective for interim and annual

periods beginning after December 15, 2012 and should be applied prospectively. The adoption of ASU 2013-02 did

not have a material effect on the Company’s consolidated financial statements. The expanded disclosures have been

included in Note 1 to these consolidated financial statements.

2 Changes in Accounting Principle

Effective January 1, 2012, the Company changed its methods of accounting for prescription drug inventories in the

RPS. Prior to 2012, the Company valued prescription drug inventories at the lower of cost or market on a first-in,

first-out (“FIFO”) basis in retail pharmacies using the retail inventory method and in distribution centers using the FIFO

cost method. Effective January 1, 2012, all prescription drug inventories in the RPS have been valued at the lower of

cost or market using the weighted average cost method. These changes affected approximately 51% of consolidated

inventories as of January 1, 2012.

These changes were made primarily to bring all of the pharmacy operations of the Company to a common inventory

valuation methodology and to provide the Company with better information to manage its retail pharmacy operations.

The Company believes the weighted average cost method is preferable to the retail inventory method and the FIFO

cost method because it results in greater precision in the determination of cost of revenues and inventories by specific

drug product and results in a consistent inventory valuation method for all of the Company’s prescription drug

inventories as the PSS’s mail service and specialty pharmacies were already on the weighted average cost method.

Most of these mail service and specialty pharmacies in the PSS were acquired in the Company’s 2007 acquisition of

Caremark Rx, Inc.