CVS 2013 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2013 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

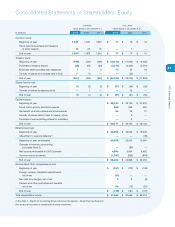

59

2013 Annual Report

Corporate Segment –

The Corporate Segment provides management and administrative services to support the

Company. The Corporate Segment consists of certain aspects of the Company’s executive management, corporate

relations, legal, compliance, human resources, corporate information technology and finance departments.

Principles of consolidation – The consolidated financial statements include the accounts of the Company and

its majority owned subsidiaries. All intercompany balances and transactions have been eliminated.

Use of estimates – The preparation of financial statements in conformity with accounting principles generally

accepted in the United States of America requires management to make estimates and assumptions that affect the

reported amounts in the consolidated financial statements and accompanying notes. Actual results could differ from

those estimates.

Fair value hierarchy – The Company utilizes the three-level valuation hierarchy for the recognition and disclosure

of fair value measurements. The categorization of assets and liabilities within this hierarchy is based upon the lowest

level of input that is significant to the measurement of fair value. The three levels of the hierarchy consist of the

following:

• Level 1 – Inputs to the valuation methodology are unadjusted quoted prices in active markets for identical assets or

liabilities that the Company has the ability to access at the measurement date.

• Level 2 – Inputs to the valuation methodology are quoted prices for similar assets and liabilities in active markets,

quoted prices in markets that are not active or inputs that are observable for the asset or liability, either directly or

indirectly, for substantially the full term of the instrument.

• Level 3 – Inputs to the valuation methodology are unobservable inputs based upon management’s best estimate

of inputs market participants could use in pricing the asset or liability at the measurement date, including assump-

tions about risk.

Cash and cash equivalents – Cash and cash equivalents consist of cash and temporary investments with maturities

of three months or less when purchased. The Company invests in short-term money market funds, commercial paper

and time deposits, as well as other debt securities that are classified as cash equivalents within the accompanying

consolidated balance sheets, as these funds are highly liquid and readily convertible to known amounts of cash.

These investments are classified within Level 1 of the fair value hierarchy because they are valued using quoted

market prices.

Short-term investments – The Company’s short-term investments consist of certificate of deposits with initial

maturities of greater than three months when purchased. These investments, which were classified as available-for-

sale within Level 1 of the fair value hierarchy, were carried at fair value, which approximated historical cost at

December 31, 2013 and 2012.

Fair value of financial instruments – As of December 31, 2013, the Company’s financial instruments include

cash and cash equivalents, short-term investments, accounts receivable, accounts payable and short-term debt.

Due to the short-term nature of these instruments, the Company’s carrying value approximates fair value. The

carrying amount and estimated fair value of total long-term debt was $13.4 billion and $14.2 billion, respectively,

as of December 31, 2013. The fair value of the Company’s long-term debt was estimated based on quoted rates

currently offered in active markets for the Company’s debt, which is considered Level 1 of the fair value hierarchy.

The Company had outstanding letters of credit, which guaranteed foreign trade purchases, with a fair value of

$3.6 million as of December 31, 2013. There were no outstanding derivative financial instruments as of December 31,

2013 and 2012.