Asus 2013 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2013 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

31

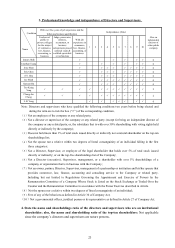

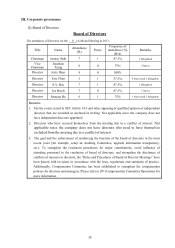

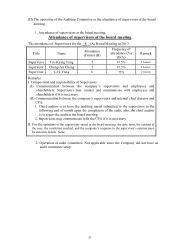

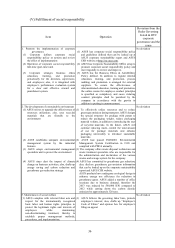

(II) The operation of the Auditing Committee or the attendance of supervisors at the board

meeting:

1. Attendance of supervisors at the board meeting

Attendance of supervisors at the board meeting

The attendance of Supervisors for the 8 (A) Board Meeting in 2013:

Title Name Attendance

(Times) (B)

Frequency of

attendance (%)

(B/A)

Remark

Supervisor Tze-Kaing Yang 7 87.5% 1 leaves

Supervisor Chung-Jen Cheng 7 87.5% 1 leaves

Supervisor L.H. Yang 6 75% 2 leaves

Remarks:

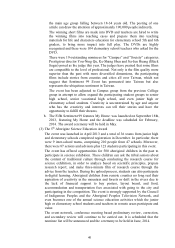

I. Composition and responsibility of Supervisors:

(I) Communication between the company’s supervisors and employees and

shareholders: Supervisors may contact and communicate with employees and

shareholders if it is necessary.

(II) Communication between the company’s supervisors and internal chief director and

CPA:

1. Chief auditor is to have the auditing report submitted to the supervisors in the

following end of month upon the completion of the audit; also, the chief auditor

is to report the audit at the board meeting.

2. Supervisors may communicate with the CPA if it is necessary.

II. For the opinions of the supervisors stated in the board meeting, the date, term, the content of

the case, the resolution reached, and the company’s response to the supervisor’s opinion must

be stated in details: None.

2. Operation of audit committee: Not applicable since the Company did not have an

audit committee setup.