Asus 2013 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2013 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

103

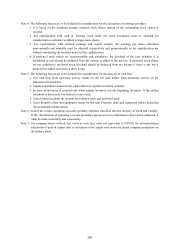

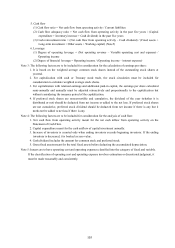

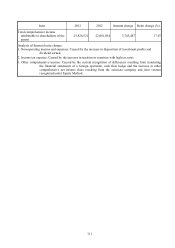

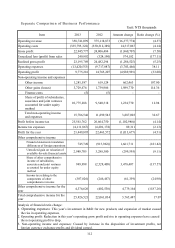

5. Cash flow

(1) Cash flow ratio = Net cash flow from operating activity / Current liabilities

(2) Cash flow adequacy ratio = Net cash flow from operating activity in the past five years / (Capital

expenditure + Inventory increase + Cash dividend) in the past five years

(3) Cash reinvestment ratio = (Net cash flow from operating activity – Cash dividend) / (Fixed assets +

Long-term investment + Other assets + Working capital) (Note5)

6. Leverage:

(1) Degree of operating leverage = (Net operating revenue – Variable operating cost and expense) /

Operating income

(2) Degree of financial leverage = Operating income / (Operating income – interest expense)

Note 3: The following factors are to be included for consideration for the calculation of earnings per share:

1. It is based on the weighted average common stock shares instead of the outstanding stock shares at

yearend.

2. For capitalization with cash or Treasury stock trade, the stock circulation must be included for

consideration to calculate weighted average stock shares.

3. For capitalization with retained earnings and additional paid-in capital, the earnings per share calculated

semi-annually and annually must be adjusted retroactively and proportionally to the capitalization but

without considering the issuance period of the capitalization.

4. If preferred stock shares are nonconvertible and cumulative, the dividend of the year (whether it is

distributed or not) should be deducted from net income or added to the net loss. If preferred stock shares

are not cumulative, preferred stock dividend should be deducted from net income if there is any but it

needs not be added to net loss if there is any.

Note 4: The following factors are to be included for consideration for the analysis of cash flow:

1. Net cash flow from operating activity meant for the net cash inflow from operating activity on the

Statement of Cash Flow.

2. Capital expenditure meant for the cash outflow of capital investment annually.

3. Increase of inventory is counted only when ending inventory exceeds beginning inventory. If the ending

inventory is decreased, it is booked as zero value.

4. Cash dividend includes the amount for common stock and preferred stock.

5. Gross fixed assets meant for the total fixed assets before deducting the accumulated depreciation.

Note 5: Issuers are to have operating cost and operating expenses classified into the category of fixed and variable.

If the classification of operating cost and operating expense involves estimation or discretional judgment, it

must be made reasonably and consistently.