Allstate 2015 Annual Report Download - page 251

Download and view the complete annual report

Please find page 251 of the 2015 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

The Allstate Corporation 2015 Annual Report 245

All states require domiciled insurance companies to prepare statutory-basis financial statements in conformity

with the NAIC Accounting Practices and Procedures Manual, subject to any deviations prescribed or permitted by the

applicable insurance commissioner and/or director. Statutory accounting practices differ from GAAP primarily since they

require charging policy acquisition and certain sales inducement costs to expense as incurred, establishing life insurance

reserves based on different actuarial assumptions, and valuing certain investments and establishing deferred taxes on a

different basis.

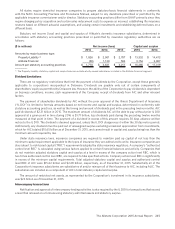

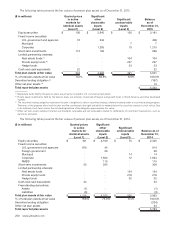

Statutory net income (loss) and capital and surplus of Allstate’s domestic insurance subsidiaries, determined in

accordance with statutory accounting practices prescribed or permitted by insurance regulatory authorities are as

follows:

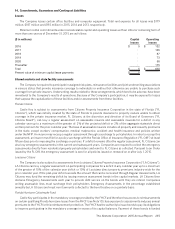

($ in millions) Net income (loss) Capital and surplus

2015 2014 2013 2015 2014

Amounts by major business type:

Property‑Liability (1) $ 1,826 $ 2,501 $ 2,707 $ 13,332 $ 14,412

Allstate Financial (56) 1,130 504 3,154 2,907

Amount per statutory accounting practices $ 1,770 $ 3,631 $ 3,211 $ 16,486 $ 17,319

(1) The Property-Liability statutory capital and surplus balances exclude wholly-owned subsidiaries included in the Allstate Financial segment.

Dividend Limitations

There are no regulatory restrictions that limit the payment of dividends by the Corporation, except those generally

applicable to corporations incorporated in Delaware. Dividends are payable only out of certain components of

shareholders’ equity as permitted by Delaware law. However, the ability of the Corporation to pay dividends is dependent

on business conditions, income, cash requirements of the Company, receipt of dividends from AIC and other relevant

factors.

The payment of shareholder dividends by AIC without the prior approval of the Illinois Department of Insurance

(“ILDOI”) is limited to formula amounts based on net income and capital and surplus, determined in conformity with

statutory accounting practices, as well as the timing and amount of dividends paid in the preceding twelve months. AIC

paid dividends of $2.31 billion in 2015. The maximum amount of dividends AIC will be able to pay without prior IL DOI

approval at a given point in time during 2016 is $1.71 billion, less dividends paid during the preceding twelve months

measured at that point in time. The payment of a dividend in excess of this amount requires 30days advance written

notice to the IL DOI. The dividend is deemed approved, unless the IL DOI disapproves it within the 30day notice period.

Additionally, any dividend must be paid out of unassigned surplus excluding unrealized appreciation from investments,

which for AIC totaled $10.65 billion as of December31, 2015, and cannot result in capital and surplus being less than the

minimum amount required by law.

Under state insurance laws, insurance companies are required to maintain paid up capital of not less than the

minimum capital requirement applicable to the types of insurance they are authorized to write. Insurance companies are

also subject to risk-based capital (“RBC”) requirements adopted by state insurance regulators. A company’s “authorized

control level RBC” is calculated using various factors applied to certain financial balances and activity. Companies that

do not maintain adjusted statutory capital and surplus at a level in excess of the company action level RBC, which is

two times authorized control level RBC, are required to take specified actions. Company action level RBC is significantly

in excess of the minimum capital requirements. Total adjusted statutory capital and surplus and authorized control

level RBC of AIC were $15.62 billion and $2.48 billion, respectively, as of December31, 2015. Substantially all of the

Corporation’s insurance subsidiaries are subsidiaries of and/or reinsure all of their business to AIC, including ALIC. The

subsidiaries are included as a component of AIC’s total statutory capital and surplus.

The amount of restricted net assets, as represented by the Corporation’s investment in its insurance subsidiaries,

was $23 billion as of December31, 2015.

Intercompany transactions

Notification and approval of intercompany lending activities is also required by the IL DOI for transactions that exceed

a level that is based on a formula using statutory admitted assets and statutory surplus.