Allstate 2015 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2015 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

120 www.allstate.com

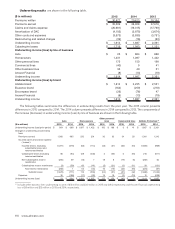

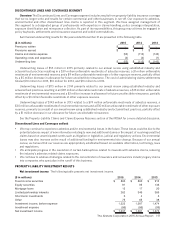

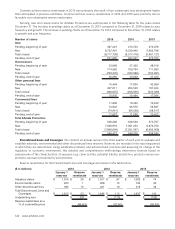

2014 Prior year reserve reestimates

($ in millions) 2004 &

prior 2005 2006 2007 2008 2009 2010 2011 2012 2013 Total

Allstate brand $ (38) $ (10) $ (11) $ 2 $ (20) $ 37 $ (86) $ (35) $ (99) $ 89 $ (171)

Esurance brand — — — — — — — (9) 6 (13) (16)

Encompass brand 2 1 — 1 (1) (2) (2) (5) (6) 3 (9)

Total Allstate Protection (36) (9) (11) 3 (21) 35 (88) (49) (99) 79 (196)

Discontinued Lines and

Coverages 112 — — — — — — — — — 112

Total Property‑Liability $ 76 $ (9) $ (11) $ 3 $ (21) $ 35 $ (88) $ (49) $ (99) $ 79 $ (84)

2013 Prior Year Reserve Reestimates

($ in millions) 2003 &

prior 2004 2005 2006 2007 2008 2009 2010 2011 2012 Total

Allstate brand $ 56 $ 5 $ (33) $ (44) $ (45) $ (32) $ (59) $ (16) $ (70) $ 18 $ (220)

Esurance brand — — — — — — — — — — —

Encompass brand 2 1 1 (1) (1) (5) (4) (4) (14) (18) (43)

Total Allstate Protection 58 6 (32) (45) (46) (37) (63) (20) (84) — (263)

Discontinued Lines and

Coverages 142 — — — — — — — — — 142

Total Property‑Liability $ 200 $ 6 $ (32) $ (45) $ (46) $ (37) $ (63) $ (20) $ (84) $ — $ (121)

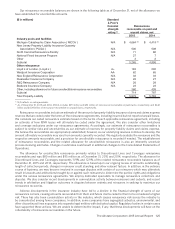

Allstate brand prior year reserve reestimates were $38 million unfavorable in 2015, $171 million favorable in 2014

and $220 million favorable in 2013. In 2015, this was primarily due to severity development for bodily injury coverage for

recent years that was more than expected and litigation settlements from older years. In 2014, this was primarily due to

severity development that was better than expected. In 2013, this was primarily due to severity development that was

better than expected and catastrophe reserve reestimates.

These trends are primarily responsible for revisions to loss development factors, as described above, used to predict

how losses are likely to develop from the end of a reporting period until all claims have been paid. Because these

trends cause actual losses to differ from those predicted by the estimated development factors used in prior reserve

estimates, reserves are revised as actuarial studies validate new trends based on the indications of updated development

factor calculations.

The impact of these reestimates on the Allstate brand underwriting income is shown in the table below.

($ in millions) 2015 2014 2013

Reserve reestimates $ 38 $ (171) $ (220)

Allstate brand underwriting income 1,812 2,235 2,551

Reserve reestimates as a % of underwriting income (2.1)% 7.7% 8.6%

Esurance brand prior year reserve reestimates were $17 million favorable in 2015 and $16 million favorable in 2014.

In 2015 and 2014, this was primarily due to severity development that was better than expected for liability coverages.

There were no prior year reserve reestimates for Esurance in 2013.