Advance Auto Parts 2008 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2008 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

37

and liabilities upon adoption. Therefore, this adoption did not have a material effect on our financial position, results

of operations or cash flows.

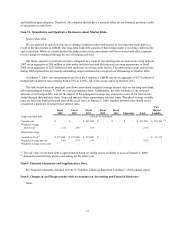

Item 7A. Quantitative and Qualitative Disclosures about Market Risks.

Interest Rate Risk

We are exposed to cash flow risk due to changes in interest rates with respect to our long-term bank debt as a

result of the movements in LIBOR. Our long-term bank debt consists of borrowings under a revolving credit facility

and a term loan. While we cannot predict the impact interest rate movements will have on our bank debt, exposure

to rate changes is managed through the use of hedging activities.

Our future exposure to interest rate risk is mitigated as a result of our entering into an interest rate swap in fiscal

2007 on an aggregate of $50 million of debt under our term loan and four interest rate swap agreements in fiscal

2006 on an aggregate of $225 million of debt under our revolving credit facility. The interest rate swaps entered into

during 2006 replaced the previously outstanding swaps terminated as a result of our refinancing in October 2006.

At January 3, 2009, our outstanding swaps fixed the Company’s LIBOR rate on an aggregate of $275 million of

hedged debt at interest rates ranging from 4.01% to 4.98%. All of the swaps expire in October 2011.

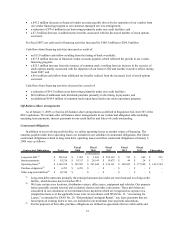

The table below presents principal cash flows and related weighted average interest rates on our long-term bank

debt outstanding at January 3, 2009, by expected maturity dates. Additionally, the table includes (i) the notional

amounts of our hedged debt, and (ii) the impact of the anticipated average pay and receive rates of our interest rate

swaps through their maturity dates. Expected maturity dates approximate contract terms. Weighted average variable

rates are based on implied forward rates in the yield curve at January 3, 2009. Implied forward rates should not be

considered a predictor of actual future interest rates.

Fair

Fiscal Fiscal Fiscal Fiscal Fiscal Market

2009 2010 2011 2012 2013 Thereafter Total Liabilit

y

Long-term bank debt: (dollars in thousands)

Variable rate -$ -$ 451,500$ -$ -$ -$ 451,500$ 370,500$

(1)

Weighted average

interest rate 2.1% 2.6% 3.3% - - - 2.5% -

Interest rate swap:

Variable to fixed

(2)

275,000$ 275,000$ 275,000$ -$ - - - 21,979$

Weighted average pay rate 3.6% 3.1% 2.4% - - - 3.0% -

Weighted average receive rate - - - - - - - -

(1) The fair value of our bank debt is approximated based on similar issues available to us as of January 3, 2009.

(2) Amounts presented may not be outstanding for the entire year.

Item 8. Financial Statements and Supplementary Data.

See financial statements included in Item 15 “Exhibits, Financial Statement Schedules” of this annual report.

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure.

None.