Westjet 2011 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2011 Westjet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

Management’s Discussion and Analysis of Financial Results 2011

│

significant reduction in guest traffic on our network could have a material adverse effect on our business, results from

operations and financial condition.

Governmental fee increases discourage air travel.

All commercial service airports in Canada are regulated by the federal government. Airport authorities continue to implement

or increase various user fees that impact travel costs for guests, including landing fees for airlines and airport improvement

fees. Airport authorities generally have the unilateral discretion to implement and adjust such fees. The combined increased

fees, and increases in rents under various lease agreements between airport authorities and the Government of Canada,

which in many instances are passed through to air carriers and air travellers, may negatively impact travel, in particular,

discretionary travel.

Increases in air navigation fees in Canada could have a negative impact on our business and our financial results.

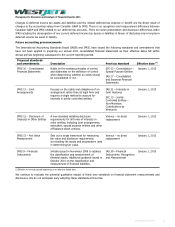

ACCOUNTING

Critical accounting estimates and judgments

The preparation of consolidated financial statements in conformity with IFRS requires management to make both judgments

and estimates that could materially affect the amounts recognized in the financial statements. By their nature, judgments and

estimates may change in light of new facts and circumstances in the internal and external environment. The following

judgments and estimates are those deemed by management to be material to the preparation of the financial statements.

Judgments

(i) Componentization

The componentization of the our assets, namely aircraft, are based on management’s judgment of what costs constitute a

significant cost in relation to the total cost of an asset and whether these costs have similar or dissimilar patterns of

consumption and useful lives for purposes of calculation depreciation and amortization. The components chosen by

management have a material effect on the balances of property, plant and equipment and intangible assets as well as the

provision for depreciation and amortization recorded in earnings each period.

(ii) Depreciation and amortization

Depreciation and amortization methods for aircraft and related components as well as other property, plant and equipment

and intangible assets are based on management’s judgment of the most appropriate method to reflect the pattern of an

asset’s future economic benefit expected to be consumed by us. Among other factors, these judgments are based on industry

standards, manufacturers’ guidelines and company specific history and experience.

(iii) Impairment

Assessment of impairment is based on management’s judgment of whether there are sufficient internal and external factors

that would indicate that an asset or cash generating unit (CGU) is impaired. The determination of CGUs are also based on

management’s judgment and are an assessment of the smallest group of assets that generate cash inflows independently of

other assets. Factors considered include whether an active market exists for the output produced by the asset or group of

assets as well as how management monitors and makes decisions about operations.

(iv) Lease classification

Assessing whether a lease is a finance lease or an operating lease is based on management’s judgment of the criteria applied

in IAS 17 – Leases. The most prevalent leases are those for aircraft. Management has determined that all of our leased

aircraft are operating leases.

WestJet Annual Report 2011 48