Wells Fargo 2010 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2010 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

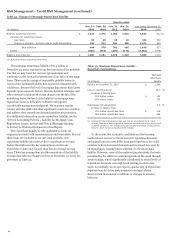

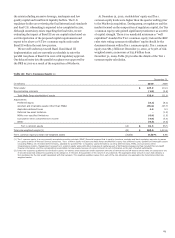

Our significant accounting policies (see Note 1 (Summary of

Significant Accounting Policies) to Financial Statements in this

Report) are fundamental to understanding our results of

operations and financial condition because they require that we

use estimates and assumptions that may affect the value of our

assets or liabilities and financial results. Six of these policies are

critical because they require management to make difficult,

subjective and complex judgments about matters that are

inherently uncertain and because it is likely that materially

different amounts would be reported under different conditions

or using different assumptions. These policies govern:

Critical Accounting Policies

• the allowance for credit losses;

• purchased credit-impaired (PCI) loans;

• the valuation of residential mortgage servicing rights

(MSRs);

• liability for mortgage loan repurchase losses;

• the fair valuation of financial instruments; and

• income taxes.

Management has reviewed and approved these critical

accounting policies and has discussed these policies with the

Board’s Audit and Examination Committee.

Allowance for Credit Losses

The allowance for credit losses, which consists of the allowance

for loan losses and the allowance for unfunded credit

commitments, is management’s estimate of credit losses

inherent in the loan portfolio at the balance sheet date, excluding

loans carried at fair value. We develop and document our

allowance methodology at the portfolio segment level. Our loan

portfolio consists of a commercial loan portfolio segment and a

consumer loan portfolio segment.

We employ a disciplined process and methodology to

establish our allowance for credit losses. The total allowance for

credit losses considers both impaired and unimpaired loans.

While our methodology attributes portions of the allowance to

specific portfolio segments, the entire allowance for credit losses

is available to absorb credit losses inherent in the total loan

portfolio. No single statistic or measurement determines the

adequacy of the allowance for credit losses.

COMMERCIAL PORTFOLIO SEGMENT The allowance for credit

losses for unimpaired commercial loans is estimated through the

application of loss factors to loans based on credit risk rating for

each loan. In addition, the allowance for credit losses for

unfunded commitments, including letters of credit, is estimated

by applying these loss factors to loan equivalent exposures. The

loss factors reflect the estimated default probability and quality

of the underlying collateral. The loss factors used are statistically

derived through the observation of historical losses incurred for

loans within each credit risk rating over a relevant specified

period of time. As appropriate, we adjust or supplement these

loss factors and estimates to reflect other risks that may be

identified from current conditions and developments in selected

portfolios.

The allowance also includes an amount for estimated credit

losses on impaired loans such as nonaccrual loans and loans that

have been modified in a TDR, whether on accrual or nonaccrual

status.

CONSUMER PORTFOLIO SEGMENT Loans are pooled generally

by product type with similar risk characteristics. Losses are

estimated using forecasted losses to represent our best estimate

of inherent loss based on historical experience, quantitative and

other mathematical techniques over the loss emergence period.

Each business group exercises significant judgment in the

determination of the credit loss estimation model that fits the

credit risk characteristics of its portfolio. We use both internally

developed and vendor supplied models in this process. We often

use roll rate or net flow models for near-term loss projections,

and vintage-based models, behavior score models, and time

series or statistical trend models for longer-term projections.

Management must use judgment in establishing additional input

metrics for the modeling processes, considering further

stratification into sub-product, origination channel, vintage, loss

type, geographic location and other predictive characteristics. In

addition, we establish an allowance for consumer loans modified

in a TDR, whether on accrual or nonaccrual status.

The models used to determine the allowance are validated by

an independent internal model validation group operating in

accordance with Company policies.

OTHER ACL MATTERS An allowance for impaired consumer and

commercial loans that have been modified in a TDR is measured

based on an estimate of cash flows, both principal and interest,

expected to be collected or an assessment of the fair value of

collateral underlying the impaired loan, if applicable.

Management exercises significant judgment to develop these

estimates.

Commercial and consumer PCI loans may require an

allowance subsequent to their acquisition. This allowance

requirement is due to probable decreases in expected principal

and interest cash flows (other than due to decreases in interest

rate indices and changes in prepayment assumptions).

The allowance for credit losses for both portfolio segments

includes an amount for imprecision or uncertainty that may

change from period to period. This amount represents

management’s judgment of risks inherent in the processes and

assumptions used in establishing the allowance. This imprecision

considers economic environmental factors, modeling

assumptions and performance, process risk, and other subjective

factors, including industry trends.

SENSITIVITY TO CHANGES Changes in the allowance for credit

losses and, therefore, in the related provision expense can

materially affect net income. The establishment of the allowance

for credit losses relies on a consistent quarterly process that

requires significant management review and judgment.

Management considers changes in economic conditions,

customer behavior, and collateral value, among other influences.

From time to time, economic factors or business decisions, such

84