Wells Fargo 2010 Annual Report Download - page 182

Download and view the complete annual report

Please find page 182 of the 2010 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

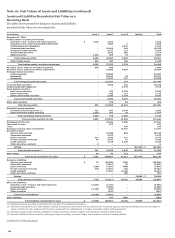

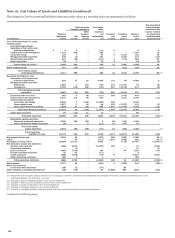

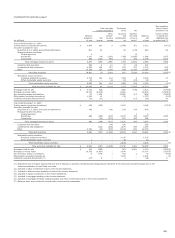

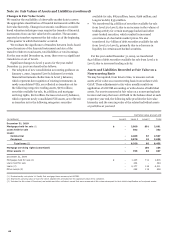

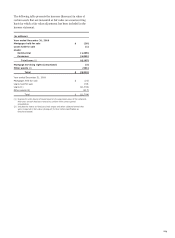

Note 16: Fair Values of Assets and Liabilities (continued)

We incorporate lack of liquidity into our fair value

measurement based on the type of asset or liability measured

and the valuation methodology used. For example, for certain

residential MHFS and certain securities where the significant

inputs have become unobservable due to illiquid markets and

vendor or broker pricing is not used, we use a discounted cash

flow technique to measure fair value. This technique

incorporates forecasting of expected cash flows (adjusted for

credit loss assumptions and estimated prepayment speeds)

discounted at an appropriate market discount rate to reflect the

lack of liquidity in the market that a market participant would

consider. For other securities where vendor or broker pricing is

used, we use either unadjusted broker quotes or vendor prices or

vendor or broker prices adjusted by weighting them with

internal discounted cash flow techniques to measure fair value.

These unadjusted vendor or broker prices inherently reflect any

lack of liquidity in the market as the fair value measurement

represents an exit price from a market participant viewpoint.

Following are descriptions of the valuation methodologies

used for assets and liabilities recorded at fair value on a

recurring or nonrecurring basis and for estimating fair value for

financial instruments not recorded at fair value.

Assets

SHORT-TERM FINANCIAL ASSETS

Short-term financial assets

include cash and due from banks, federal funds sold and

securities purchased under resale agreements and due from

customers on acceptances. These assets are carried at historical

cost. The carrying amount is a reasonable estimate of fair value

because of the relatively short time between the origination of

the instrument and its expected realization.

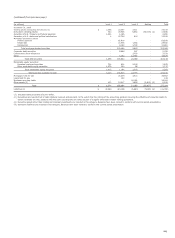

TRADING ASSETS (EXCLUDING DERIVATIVES) AND

SECURITIES AVAILABLE FOR SALE Trading assets and

securities available for sale are recorded at fair value on a

recurring basis. Fair value measurement is based upon quoted

prices in active markets, if available. Such instruments are

classified within Level 1 of the fair value hierarchy. Examples

include exchange-traded equity securities and some highly liquid

government securities such as U.S. Treasuries. When

instruments are traded in secondary markets and quoted market

prices do not exist for such securities, we generally rely on

internal valuation techniques or on prices obtained from

independent pricing services or brokers (collectively, vendors) or

combination thereof.

Trading securities are mostly valued using trader prices that

are subject to independent price verification procedures. The

majority of fair values derived using internal valuation

techniques are verified against multiple pricing sources,

including prices obtained from independent vendors. Vendors

compile prices from various sources and often apply matrix

pricing for similar securities when no price is observable. We

review pricing methodologies provided by the vendors in order

to determine if observable market information is being used,

versus unobservable inputs. When evaluating the

appropriateness of an internal trader price compared with

vendor prices, considerations include the range and quality of

vendor prices. Vendor prices are used to ensure the

reasonableness of a trader price; however valuing financial

instruments involves judgments acquired from knowledge of a

particular market and is not perfunctory. If a trader asserts that

a vendor price is not reflective of market value, justification for

using the trader price, including recent sales activity where

possible, must be provided to and approved by the appropriate

levels of management.

Similarly, while securities available for sale traded in

secondary markets are typically valued using unadjusted vendor

prices or vendor prices adjusted by weighting them with internal

discounted cash flow techniques, these prices are reviewed and,

if deemed inappropriate by a trader who has the most knowledge

of a particular market, can be adjusted. Securities measured with

these internal valuation techniques are generally classified as

Level 2 of the hierarchy and often involve using quoted market

prices for similar securities, pricing models, discounted cash

flow analyses using significant inputs observable in the market

where available or combination of multiple valuation techniques.

Examples include certain residential and commercial MBS,

municipal bonds, U.S. government and agency MBS, and

corporate debt securities.

Security fair value measurements using significant inputs

that are unobservable in the market due to limited activity or a

less liquid market are classified as Level 3 in the fair value

hierarchy. Such measurements include securities valued using

internal models or combination of multiple valuation techniques

such as weighting of internal models and vendor or broker

pricing, where the unobservable inputs are significant to the

overall fair value measurement. Securities classified as Level 3

include certain residential and commercial MBS, asset-backed

securities collateralized by auto leases or loans and cash

reserves, CDOs and CLOs, and certain residual and retained

interests in residential mortgage loan securitizations. CDOs are

valued using the prices of similar instruments, the pricing of

completed or pending third party transactions or the pricing of

the underlying collateral within the CDO. Where vendor or

broker prices are not readily available, management's best

estimate is used.

MORTGAGES HELD FOR SALE (MHFS) We carry substantially all

of our residential MHFS portfolio at fair value. Fair value is

based on independent quoted market prices, where available, or

the prices for other mortgage whole loans with similar

characteristics. As necessary, these prices are adjusted for typical

securitization activities, including servicing value, portfolio

composition, market conditions and liquidity. Most of our MHFS

are classified as Level 2. For the portion where market pricing

data is not available, we use a discounted cash flow model to

estimate fair value and, accordingly, classify as Level 3.

LOANS HELD FOR SALE (LHFS) LHFS are carried at the lower of

cost or market value, or at fair value for certain portfolios that

we intend to hold for trading purposes. The fair value of LHFS is

based on what secondary markets are currently offering for

portfolios with similar characteristics. As such, we classify those

loans subjected to nonrecurring fair value adjustments as

Level 2.

180