Qantas 2006 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2006 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

|

|

130

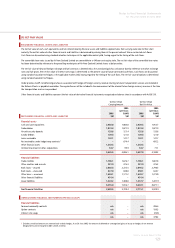

Notes to the Financial Statements

for the year ended 30 June 2006

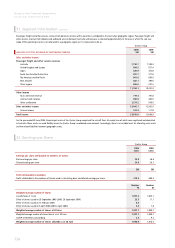

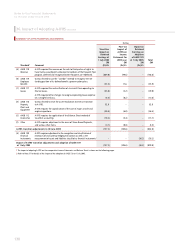

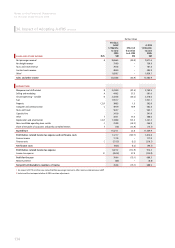

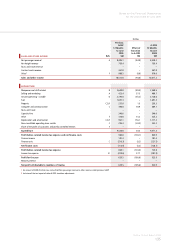

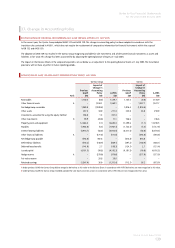

36. Impact of Adopting A-IFRS continued

SUMMARY OF A-IFRS TRANSITION ADJUSTMENTS

Qantas

Standard1Comment

Transition

Impact on

Retained

Earnings at

1 July 2004

$M

(Dr)/Cr

Post-tax

Impact of

A-IFRS on

Income

Statement for

2005 year

$M

(Dr)/Cr

Impact on

Retained

Earnings on

Adoption

of AASB 139

at 1 July 2005

$M

(Dr)/Cr

Total

$M

(A) AASB 118

Revenue

A-IFRS required the revenue on the sale to third parties of rights to

have Qantas award points allocated to members of the Frequent Flyer

program, deferred and recognised when the points are redeemed. (669.0) (99.6) – (768.6)

(B) AASB 119

Employee

Benefits

Qantas elected to use the "corridor" method to recognise the net

funding position of its defined benefit superannuation plans.

(53.5) 17.6 – (35.9)

(C) AASB 117

Leases

A-IFRS required the reclassification of six aircraft from operating to

finance leases. (45.8) (3.2) – (49.0)

A-IFRS required other changes to recognise operating leases expense

on a straight line basis. (6.4) (8.2) – (14.6)

(D) AASB 116

Property,

Plant and

Equipment

Qantas elected to reset the asset revaluation reserve on transition

to A-IFRS. 82.9 – – 82.9

A-IFRS requires the capitalisation of the cost of major aircraft and

engine inspections. (50.4) (6.0) – (56.4)

(E) AASB 112

Income Tax

A-IFRS requires the application of the Balance Sheet method of

tax-effect accounting. (10.3) (5.4) – (15.7)

(F) Other A-IFRS requires adjustment in the areas of Share-Based Payments,

and various other items. (4.7) (0.8) – (5.5)

A-IFRS transition adjustments to 30 June 2005 (757.2) (105.6) – (862.8)

(G) AASB 139

Financial

Instruments

A-IFRS requires adjustment to the recognition and classifi cation of

revenue, fuel and currency hedging transactions as well as the

measurement of assets and liabilities classifi ed as fi nancial instruments.

2 – – (36.2) (36.2)

Impact of A-IFRS transition adjustments and adoption of AASB 139

at 1 July 2005 (757.2) (105.6) (36.2) (899.0)

1 The impact of adopting A-IFRS on the comparative Income Statements and Balance Sheet is shown on the following pages.

2 Refer to Note 37 for details of the impact of the adoption of AASB 139 at 1 July 2005.