Qantas 2006 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2006 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

101

Qantas Annual Report 2006

Notes to the Financial Statements

for the year ended 30 June 2006

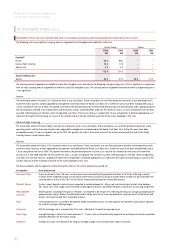

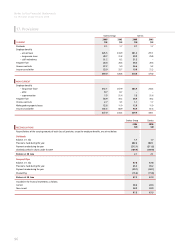

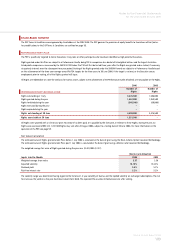

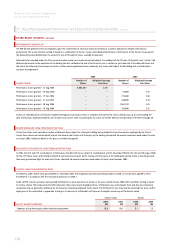

23. Contingent Liabilities

Details of contingent liabilities, where the probability of future payments is not considered remote, are set out below. The Directors are of the opinion that

provisions are not required with respect to these matters, as it is not probable that a future sacrifice of economic benefits will be required or the amount is not

capable of reliable measurement.

Qantas Group Qantas

2006

$M

2005

$M

2006

$M

2005

$M

Guarantees and letters of comfort to support operating lease commitments

and other arrangements entered into with other parties by controlled entities 24.7 22.5 24.7 22.5

Guarantees and letters of comfort to support leveraged and operating lease

commitments to other parties on behalf of associates and jointly controlled entities 0.3 0.1 0.3 0.1

General guarantees in the normal course of business 119.9 122.4 119.9 122.4

Contingent liabilities relating to current and threatened litigation 9.5 17.0 9.3 15.9

154.4 162.0 154.2 160.9

TERMINAL FUEL FACILITIES

The Qantas Group, together with other airlines, has entered into various agreements in order to facilitate the funding and installation of jet turbine fuel

hydrant systems and terminal equipment facilities at Los Angeles and Honolulu Airports. The airlines have jointly and severally agreed to repay any unpaid

balance (including interest) of the loans totalling $337.8 million (2005: $186.2 million) in the event the agreements are terminated prior to expiry of the loans.

AIRCRAFT FINANCING

As part of the financing arrangements for the acquisition of aircraft, the Qantas Group has provided certain guarantees and indemnities to various lenders

and equity participants in leveraged lease transactions. In certain circumstances, including the insolvency of major international banks, the Qantas Group may

be required to make payments under these guarantees. The Qantas Group has guaranteed that the lessors will receive all of the funds due to them under the

lease arrangements.

Qantas and certain controlled entities have entered into asset value underwriting arrangements with lenders under certain aircraft secured financings. These

arrangements protect the value of the aircraft security to the lenders to a pre-determined level. This is reflected by the balance of aircraft security deposits held

with certain financial institutions.

The Qantas Group has provided standard tax indemnities to the equity investors in certain leveraged leases. The indemnities effectively guarantee the after-tax

rate of return of the investors and the Qantas Group may be subject to additional financing costs on future lease payments if certain assumptions made at the

time of entering the transactions, including assumptions as to the rate of income tax, subsequently become invalid.

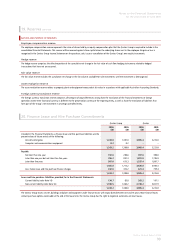

FREIGHT INVESTIGATION

As part of its investigation into alleged price fixing in the air cargo market, particularly relating to fuel and other surcharges, the US Department of Justice

(DOJ) has served subpoenas to produce documents on a number of cargo operators. As part of this investigation a subpoena was served on Qantas Freight in

the USA in May 2006. The ACCC, the European Commission (EC) and other regulators are conducting similar investigations.

In addition to ensuring compliance with the DOJ subpoena, Qantas immediately undertook a detailed review of its cargo operations to review whether it had,

at all times, complied with the law. During this investigation, Qantas has learnt that the practice adopted by the cargo industry to fix and impose fuel

surcharges may have breached relevant international competition laws. Qantas is co-operating fully with all regulators and will be providing them with all

relevant information to permit them to undertake their investigations. At this stage, it is not possible to quantify any liability associated with this matter.

CONSTRUCTION DISPUTE

Qantas was issued with a notice of dispute in March 2005 in relation to a contract let by Qantas for design and construction of a Heavy Maintenance Hangar

at Brisbane Airport. Proceedings were commenced against Qantas in respect of one aspect of those claims. In the Directors’ opinion, disclosure of any further

information would be prejudicial to the interests of Qantas.

UNREALISED GAINS/LOSSES – BACK-TO-BACK HEDGES

Where long-term borrowings are held in foreign currencies in which Qantas derives surplus net revenue, off-setting forward foreign exchange contracts have

been used to match the cash flows arising under the borrowings with the expected revenue surpluses used to hedge the borrowings. To the extent a gain or

loss is incurred, and the cash flow hedge is deemed effective, this is deferred in the hedge reserve until the net revenue is realised. As at 30 June 2006, total

unrealised exchange gains on hedges of net revenue designated to service long-term debt were $184.8 million (2005: $228.4 million gains).