Logitech 2012 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2012 Logitech annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

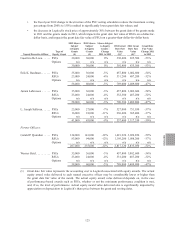

OTHER COMPENSATION POLICIES

Derivatives

We do not permit certain persons designated by the Company as insiders, including officers and directors, to

trade in puts, calls, warrants or other derivative Logitech securities traded on an exchange or in any other organized

securities market.

Recovery of compensation for restatements and misconduct

In June 2010, the Compensation Committee adopted a policy regarding the recovery of compensation paid

to an executive officer or the principal accounting officer of the Company. Under the terms of the policy we may

recover bonus amounts, equity awards or other incentive compensation awarded or paid within the prior three years

to a covered officer if the Compensation Committee determines the compensation was based on any performance

goals that were met or exceeded as a result, in whole or in part, of the officer’s fraud or misconduct, or the officer

knew at the time of the existence of fraud or misconduct that resulted in performance goals being met or exceeded,

and a lower amount would otherwise have been awarded or paid to the officer. In addition, under the policy Logitech

may recover gains realized on the exercise of stock options or on the sale of vested shares by an executive officer

or the principal accounting officer if, within three years after the date of the gains or sales, Logitech discloses the

need for a significant financial restatement, other than a financial restatement solely because of revisions to US

GAAP, and the Compensation Committee determines that the officer’s fraud or misconduct caused or partially

caused the need for the restatement, or the covered officer knew at the time of the existence of fraud or misconduct

that resulted in the need for such restatement.

In addition, our 2006 Stock Incentive Plan and our Management Performance Bonus Plan provide that awards

under the plans are suspended or forfeited if the plan participant, whether or not an executive officer:

• has committed an act of embezzlement, fraud or breach of fiduciary duty;

• makes an unauthorized disclosure of any Logitech trade secret or confidential information; or

• induces any customer to breach a contract with Logitech.

Any decision to suspend or cause a forfeiture of any award held by an executive officer under the 2006 Stock

Incentive Plan or the Management Performance Bonus Plan is subject to the approval of the Board of Directors.

Additional tax and accounting considerations

U.S. Tax Code Section 162(m)

We are limited by Section 162(m) of the U.S. Tax Code, or Section 162(m), to a deduction for U.S. federal

income tax purposes of up to $1 million of compensation paid to our CEO and any of our three most highly

compensated executive officers, other than our Chief Financial Officer, in a taxable year. Compensation above

$1 million may be deducted if, by meeting certain technical requirements, it can be classified as “performance-

based compensation.” The Compensation Committee considers the implications of Section 162(m) in setting and

determining executive officer long-term equity incentive award grants and in setting short-term cash incentive

award compensation.

The Logitech International S.A. 2006 Stock Incentive Plan approved by our shareholders in 2006 permits

certain grants of awards under that plan to qualify as “performance-based compensation.” Bonuses paid to executives

under the Bonus Plan may similarly qualify under Section 162(m). Although the Compensation Committee uses

the requirements of Section 162(m) as a guideline, deductibility is not the sole factor it considers in assessing the

appropriate levels and types of executive compensation, and it will elect to forego deductibility when the Committee

believes it to be in the best interests of the Company and its shareholders.

132