HSBC 2006 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

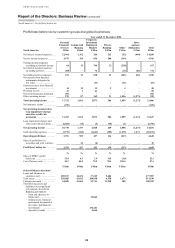

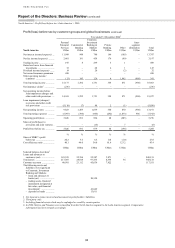

93

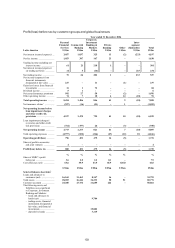

8 per cent. On an underlying basis, pre-tax profits

rose by 5 per cent. Growth in profitability was

constrained by the non-recurrence of one-off

coverage bond receipts and other items related to the

2001 sovereign debt default and subsequent

pesification in Argentina, which added

US$122 million to 2005 profits. In addition, a gain

of US$89 million from the sale of the property and

casualty insurance business, HSBC Seguros de

Automoveis e Bens Limitada, to HDI Seguros S.A.,

was recorded in 2005. Excluding these prior year

profits, and on an underlying basis, profit before tax

increased by 21 per cent, with net operating income

increasing by 15 per cent and operating expenses by

12 per cent. Corporate, Investment Banking and

Markets delivered a strong performance, driven by

growth in fee and trading income, with notable

success in bringing Latin American borrowers to

global capital markets. Commercial Banking also

grew well as domestic economies expanded. During

2006, HSBC made two significant acquisitions in the

region. In May, HSBC acquired the Argentine

banking operations of Banca Nazionale del Lavoro

SpA (‘Banca Nazionale’) to build its distribution

capabilities and, in November, Grupo Banistmo in

Central America, adding markets in five countries

new to the Group.

The following commentary is on an underlying

basis.

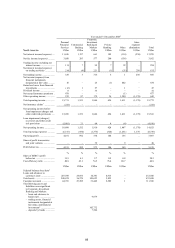

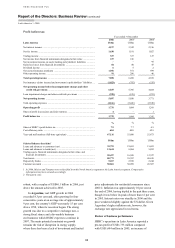

Personal Financial Services reported a pre-tax

profit of US$800 million, a rise of 1 per cent over

2005, which had benefited from a US$89 million

gain on the sale of the Group’s property and casualty

insurance business in Brazil. Adjusting for this, pre-

tax profits grew by 16 per cent, driven by 12 per cent

growth in revenues and 10 per cent growth in costs.

The underlying improvement in revenues was led by

strong asset and deposit growth together with higher

fee income, offset in part by consequential expense

growth and a rise in impairment charges as the loan

book both grew and seasoned.

In Mexico, profit before tax rose by 10 per cent.

During 2006, 56,000 Personal Financial Services

customers were transferred to the Commercial

Banking customer group, where HSBC is better

placed to meet their banking requirements. Adjusting

for this, profits were 20 per cent higher, driven by

strong balance sheet growth and improved fee

income.

Adjusting for the gain in 2005 from the sale of

the property and casualty business, pre-tax profits

were 46 per cent higher in Brazil. The strong

domestic economy stimulated robust growth in

lending and a rise in the number of current account

holders. During the year, a new and innovative

internet banking service ‘Meu HSBC’ was introduced

to Personal Financial Services customers, allowing

them to conduct different types of transactions

online using the same password as their ATM card.

In Argentina, profit before tax was marginally

higher, with strong balance sheet growth, higher fees

and improved revenues from the insurance business.

This was largely offset by increased loan impairment

charges and cost growth incurred in support of

business expansion as HSBC prepared for an

improving domestic economic environment.

Net interest income rose by 11 per cent to

US$3,057 million, largely from balance sheet growth

partly offset by lower deposit spreads.

In Mexico, net interest income increased by

12 per cent to US$1,218 million. Adjusting for the

effect of customer account transfers to Commercial

Banking, net interest income rose by 20 per cent,

driven by strong growth in credit card and mortgage

balances and increases in deposits which were

generated by the ongoing success of the ‘Tu Cuenta’

product. Overall, asset spreads improved as the

relative increase in higher margin card balances led to

a favourable change in the product mix. By contrast,

deposit spreads narrowed as interest rates declined.

Excluding customer account transfers, average

deposit balances in Mexico rose by 10 per cent.

HSBC continued to be one of the market leaders with

respect to balance growth, despite fierce competition

from other banks, improving its market share by

35 basis points. A strong increase in low-cost

deposits was reflective of the continuing success of

‘Tu Cuenta’, the first integrated financial services

product of its kind offered locally, with nearly

400,000 new accounts opened in 2006. HSBC

Premier performed well as 84,000 new customers

were added during the year. Premier deposits

represented over one third of the total personal

deposit base at 31 December 2006. The income

benefit from higher deposit balances was partly

mitigated by reduced spreads in the falling interest

rate environment, notwithstanding the positive shift

in mix from growth in non-interest bearing deposit

balances.

The credit card market in Mexico was buoyant in

2006 and HSBC’s business performed very

successfully with average balances doubling to

US$886 million. Various initiatives were

implemented to develop the business, most notably

cross-sales to ‘Tu Cuenta’ customers, targeted

customer relationship campaigns to existing clients,

successful portfolio management strategies and

promotions, development of new sales channels and