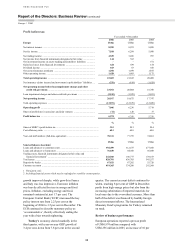

HSBC 2006 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

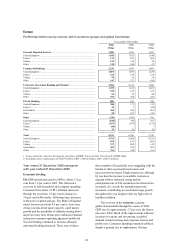

Competitive environment / Europe > 2006

30

consolidate. Within the banking sector, consolidation

continued in 2006, with a greater focus on national

networks and retail branch banking.

The Group’s principal US subsidiaries, HSBC

Bank USA and HSBC Finance, faced vigorous

competition from a wide array of financial

institutions. These include banks, thrifts, insurance

companies, credit unions, mortgage lenders and

brokers, and non-bank suppliers of consumer credit

and other financial services. Many of these

institutions are not subject to US banking industry

regulation, unlike HSBC. This gives some of them

cost and product advantages and thus increases

competitive pressure. HSBC competes by expanding

its customer base through portfolio acquisitions or

alliances, co-branding opportunities and direct sales

channels, by offering a very wide variety of

consumer loan products and by maintaining a strong

service orientation.

The slowing US housing market has had an

adverse effect on sub-prime mortgage originators

and lenders, including HSBC. Numerous sub-prime

lenders have exited the industry or have announced

that they are exploring alternatives. Investment

banks have been active purchasers of distressed

competitors in an attempt to vertically integrate

origination platforms to feed secondary market

demands.

The six largest banks in Canada dominate the

country’s financial services industry. Despite this,

the market remains very competitive with

comparable financial products and services offered

by other banks, insurance companies and other

institutions. Merger activity among the largest banks

in Canada remains possible but, without such

consolidation, growth opportunities for the larger

banks will continue to exist mainly outside of

Canada.

Latin America

Mexico’s financial system remains highly

concentrated. Five banks dominate the industry,

controlling some 80 per cent of banking assets. Of

these five, four (including HSBC) are foreign-

owned. In 2006, new banking licences were granted

to 13 bank and non-bank institutions. This will

increase competition, mainly in customer segments

in which banking is currently under-represented.

These segments also represent potential growth areas

for the existing five major banks in the medium to

long term.

There is increasing regulatory pressure on

banking and pension management fees and

commissions, which has constrained growth in

non-funds income. As a result, competition is fierce

in consumer lending, as financial institutions seek to

build alternative income streams despite difficulties

in establishing reliable consumer credit histories.

HSBC seeks to differentiate through customer

service, and is well positioned to capitalise on

economic growth with its extensive branch and ATM

network, and growing young customer base.

In Brazil, concentration in the industry

increased, with the top ten banking groups

accounting for some 70 per cent of assets and

87 per cent of branches at 31 December 2006 (2005:

68 per cent and 86 per cent respectively). These top

ten banking groups consist mainly of state-owned,

privately owned and large foreign banks (including

HSBC), and the most significant change in the

Brazilian financial system was the growing market

share of the larger privately owned banks through

consolidation in the industry and partnerships

established with national retailers.

Improvements in the macro-economic

environment, particularly in increased solvency and

liquidity in the market and in monetary policy, have

benefited the consumer through constraining

inflationary growth. Notwithstanding persistently

high interest rates, consumer borrowing has

increased. However, total lending as a percentage of

Gross Domestic Product (‘GDP’) remained low in

international terms at 34 per cent. This, together with

the fact that within the economically active

population an estimated 40 million people have

limited access to financial services, indicates that the

outlook for further growth is positive.

In Argentina, HSBC’s direct competition comes

primarily from international financial groups that

provide an equivalent range of banking, insurance,

pension and annuity products and services. Given the

growth experienced over recent years in the

Argentine economy, there has been resurgent

demand for credit products, coupled with increases

in deposits. The strong recovery in consumer

confidence is reflected in the level of private sector

loans and private deposits that grew by 40 per cent

and 22 per cent respectively compared with 2005.

The life and annuities market increased by 17 per

cent in terms of assets, while pension funds

collections increased by 30 per cent.