HSBC 2006 Annual Report Download - page 237

Download and view the complete annual report

Please find page 237 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

235

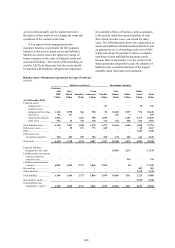

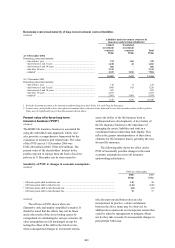

4 Comprises solvency and unencumbered assets.

5 Excludes financial assets of insurance underwriting associates, Erisa, S.A. and Ping An Insurance.

6 Comprises mainly loans and advances to banks and cash.

In life linked insurance, premium income less

charges levied is invested in unit-linked funds.

HSBC manages the financial risk of this product by

holding appropriate assets in segregated funds or

portfolios to which the liabilities are linked. This

substantially transfers the financial risk to the

policyholder. The assets held to support life linked

liabilities represented 41.7 per cent of the total

financial assets of HSBC’s insurance underwriting

subsidiaries at the end of 2006 (2005: 35.9 per cent).

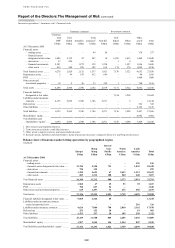

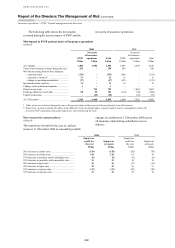

Market risk

(Audited)

Market risk can be further sub-categorised into

interest rate risk, equity risk and foreign exchange

risk. Each of these categories is discussed further

below.

Interest rate risk

(Audited)

HSBC’s insurance underwriting subsidiaries are

exposed to interest rate risk when there is a

mismatch in terms of duration or yields between the

assets and liabilities. Examples of interest rate risk

exposure are as follows:

• a fall in market interest rates results in lower

yields on the assets supporting guaranteed

investment returns payable to policyholders;

and

• a rise in market interest rates results in a

reduction in the value of the fixed income

securities portfolio which may result in losses if,

as a result of an increase of the level of

surrenders, the corresponding fixed income

securities have to be sold.

HSBC manages the interest rate risk arising

from its insurance underwriting subsidiaries by

establishing limits centrally. These govern the

sensitivity of the net present values of expected cash

flows from subsidiaries’ assets and liabilities to a

one basis point parallel upward shift in the discount

curve used to calculate values. Adherence to these

limits is monitored by local ALCOs.

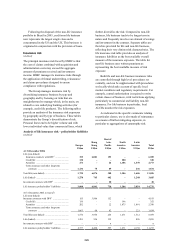

Interest rate risk is also assessed by measuring

the impact of defined movements in interest yield

curves on the profits after tax and net assets of the

insurance underwriting subsidiaries. An immediate

and permanent movement in interest yield curves as

at 31 December 2006 in all territories in which

HSBC’s insurance subsidiaries operate would have

the following impact on the profit for the year and

net assets at that date:

(Audited) 2006 2005

Impact on

profit for

the year

Impact on

net assets

Impact on

profit for

the year

Impact on

net assets

US$m US$m US$m US$m

+ 100 basis points shift in yield curves ........................ (13) (111) (46) (122)

– 100 basis points shift in yield curves ......................... 24 103 63 181

The interest rate sensitivities set out above are

illustrative only and employ simplified scenarios. It

should be noted that the effects may not be linear

and therefore the results cannot be extrapolated. The

sensitivities do not incorporate actions that could be

taken by management to mitigate the effect of the

interest rate movements, nor do they take account of

any resultant changes in policyholder behaviour.

The majority of interest rate exposure arises

within insurance underwriting subsidiaries in the

UK, the US and Hong Kong.

HSBC’s insurance underwriting subsidiaries are

also exposed to the risk that the yield on assets held

may fall short of the return guaranteed on certain

contracts issued to policyholders. This investment

return guarantee risk is managed by matching assets

held to liability requirements. In addition, a

provision is established when analysis indicates that,

over the life of the contracts, the returns from the

designated assets may not be adequate to cover the

related liabilities.

The guarantees offered to policyholders in

respect of certain insurance products are divided into

broad categories as follows:

• annuities in payment;

• deferred annuities: these consist of two phases –

the savings and investing phase, and the

retirement income phase;