HSBC 2006 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

North America > 2006

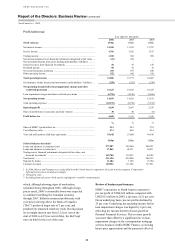

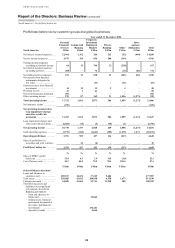

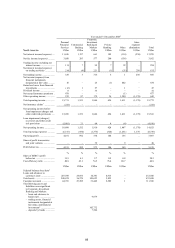

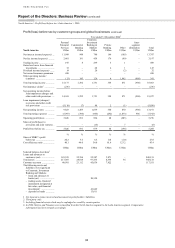

80

consequently higher in the second half of 2006 as

these portfolios seasoned, coinciding with the

weakening housing market.

In Canada, loan impairment charges were 38 per

cent higher. This primarily reflected the non-

recurrence of loan impairment releases from core

banking operations, which occurred in 2005, as well

as growth in both secured and unsecured lending

balances and higher delinquency rates in the motor

vehicle finance business.

Operating expenses grew by 12 per cent

to US$7,379 million. In the US, costs of

US$6,706 million were 11 per cent higher than in

2005. In the consumer finance business, the rise

was driven by increased headcount to support

incremental collections activity, and greater

volumes. Higher costs were incurred in marketing

cards to support the launch of new co-branded

credit cards, greater levels of mailing and other

promotional campaigns in the cards and retail

services businesses. IT and administrative expenses

grew in support of higher asset balances. A lower

level of deferred origination costs in the mortgage

services business, due to a decline in volumes,

contributed further to the cost growth.

In HSBC Bank USA, expense growth was

primarily driven by branch staff costs from

additional headcount recruited to support investment

in business expansion and new branch openings.

Greater emphasis placed on increasing the quality

and number of branch staff dedicated to sales and

customer relationship activities, which changed the

staff mix, also contributed to cost growth. The

continued promotion of the on-line savings product,

new branch openings and branding initiatives at the

John F. Kennedy International and LaGuardia

airports in New York led to a rise in marketing costs.

IT costs also grew following significant investment

expenditure incurred on several key network

efficiency projects.

In Canada, costs rose by 19 per cent, mainly due

to higher staff and marketing costs. Staff costs grew

by 13 per cent, with increased headcount supporting

expansion of the consumer finance business and

bank distribution network. Continuing investment in

growing the wealth management business and higher

incentive costs reflecting improved revenues also

contributed to the increase. Marketing costs grew

following external campaigns to improve brand

awareness.

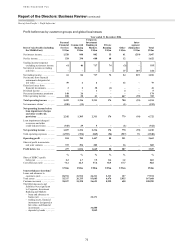

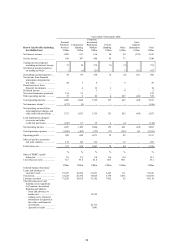

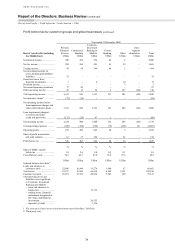

Commercial Banking’s pre-tax profits rose by

4 per cent to US$957 million, largely driven by

lending and deposit growth and higher fee income,

partly offset by increased loan impairment charges.

Costs rose mainly from geographical expansion in

the US and branch and business expansion in

Canada. The cost efficiency ratio worsened by

2.1 percentage points, as costs grew faster than

revenues.

Net interest income grew by 15 per cent to

US$1,362 million. In the US, net interest income

was 13 per cent higher, as HSBC continued to

expand its geographical presence, notably in Boston,

Connecticut, New Jersey, Philadelphia, Washington

D.C., Chicago and Los Angeles. Average deposit

balances rose by 30 per cent, aided by geographical

expansion and greater focus placed on generating

balances from commercial real estate companies and

middle market customers. In particular, there was an

increased emphasis on attracting high margin

balances from cash management sales activities.

Rising interest rates encouraged customers to

transfer funds to higher yielding products and the

resulting change in product mix led to a narrowing

of liability spreads.

The 7 per cent growth in average lending

balances was principally led by greater volumes

generated from small business and middle market

customers. This was achieved by a combination of

geographical expansion, increased marketing activity

and the recruitment of additional small-business

relationship managers. Asset spreads narrowed due

to competitive pricing pressures, particularly in the

middle market customer segment, which partly

offset the income benefits from higher lending

volumes.

In Canada, net interest income increased by

14 per cent. The strong economy encouraged

continued business investment by customers and

this, in conjunction with HSBC’s reputation for

customer service and relationship management,

helped generate a 15 per cent growth in average

lending balances. Loan spreads were broadly in line

with 2005. There was a 35 per cent improvement in

average deposit balances, driven by various factors

including the acquisition of new customers,

strengthening relationships with existing ones, and

enhancing payment and cash management products.

Deposit spreads widened as interest rates rose,

augmenting the income benefits from higher

balances.

Net interest income in Bermuda grew by

42 per cent, partly due to interest rate rises which

widened deposit spreads. Deposit balances increased

by 26 per cent, while increased cross-sales activity

contributed to a 26 per cent rise in average lending

balances.