HSBC 2006 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

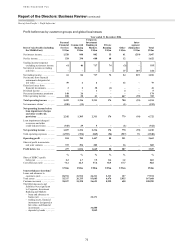

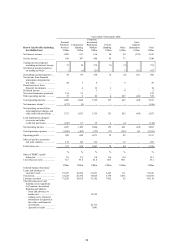

63

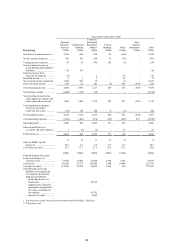

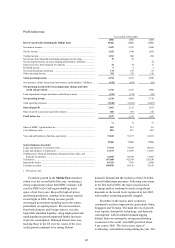

competitive pricing and customer retention initiatives

contributed to a rise in customer numbers and

resulted in a 22 per cent increase in average mortgage

balances. In India, mortgage balances rose by 27 per

cent, benefiting from increased marketing and direct

sales efforts, while in Malaysia, the successful

promotion of Homesmart, a flexible offset mortgage

product, enabled HSBC to increase average mortgage

balances by 10 per cent and widen spreads in a

highly competitive market.

Personal lending balances increased by 22 per

cent, partly as a result of significant growth in

HSBC’s consumer finance business in India,

Australia and Indonesia. In Indonesia, HSBC opened

28 dedicated consumer finance outlets while, in

India, 25 new outlets were opened in branches. In

Australia, consumer finance was developed in

partnership with well known international retailers

such as IKEA and Bang & Olufsen, together with

established local retailers including Clive Peeters and

Bing Lee. HSBC signed a number of exclusive

supplier agreements with retailers and, as a result, the

number of retail distribution outlets grew to more

than 1,100, which enabled HSBC to increase its

market share. In Malaysia, the success of HSBC’s

instalment loan product, ‘Anytime Money’, which

was re-launched in 2005, contributed to a 93 per cent

rise in average personal lending balances. In the

Middle East, HSBC focused on promoting a select

portfolio of products following a product

simplification exercise instigated in the fourth quarter

of 2005 which led to a 22 per cent rise in personal

lending balances. Investments in HSBC’s South

Korean operations had immediate results and

personal lending balances more than doubled.

Net fee income rose by 24 per cent to

US$524 million. Regional card fees were 30 per cent

higher, reflecting solid growth in cardholder

spending while, in Indonesia, higher card fee income

was a consequence of a rise in delinquencies.

The robust performance of regional stock

markets during 2006 contributed to strong demand

for investment products and led to the launch of new

investment funds, which together generated a 27 per

cent increase in investment fee income, including

custody and broking fees. Growth was particularly

strong in South Korea, Taiwan, India and Singapore.

Sales of investment products, including unit trusts,

bonds and structured products, increased by 19 per

cent to US$8.0 billion and funds under management

grew by 19 per cent to US$8.6 billion.

HSBC continued to develop its regional

insurance business by launching medical insurance in

Singapore and establishing a Takaful joint venture in

Malaysia, offering Shariah-compliant insurance

products. In the Middle East, cardholder credit

insurance was launched in the fourth quarter of

2006. These product launches were supported by

increased marketing activity and targeted investment

to increase HSBC’s presence and market share.

Consequently, the number of policies in force at the

end of 2006 rose by 89 per cent to 800,000 and

insurance fee income and insurance premiums rose

by 12 per cent and 4 per cent respectively.

Other operating income increased by

US$71 million due to gains on the sale of HSBC’s

Australian stockbroking, margin lending and

mortgage broker businesses. Additionally, HSBC

established a joint venture with Global Payments Inc.

to manage the majority of the bank’s Asian card

acquiring business. This was transferred to the joint

venture in July 2006, realising a gain of

US$10 million in the region’s Personal Financial

Services business.

Loan impairment charges and other credit risk

provisions more than doubled to US$545 million,

mainly due to higher charges for personal lending in

Taiwan and Indonesia. In Taiwan, regulatory changes

restricted collection activities and eased repayment

terms for delinquent borrowers. These changes,

coupled with a deteriorating credit environment, led

to a US$160 million increase in loan impairment

charges related mainly to the credit card portfolio,

most of which were recognised in the first half of

2006. In Indonesia, changes in minimum repayment

amounts, along with hardship following a significant

reduction in the government subsidy of fuel prices,

led to increased delinquency rates on credit cards,

also mainly in the first half of 2006. Elsewhere in the

region, credit quality was broadly stable and growth

in impairment charges followed increases in credit

card and personal lending balances.

Operating expenses increased by 26 per cent to

US$1,593 million, largely tracking revenue growth.

Expansion of the branch network and development of

sales and support functions led to higher staff

numbers and, together with higher performance-

related incentive payments, contributed to a rise in

staff costs. The new branch openings increased

premises and equipment costs. The establishment of

a number of consumer finance businesses and HSBC

Direct’s introduction in Taiwan were also factors in

the rise in operating expenses.

Marketing costs rose as HSBC increased

advertising and promotional activity directed to

attracting new customers, enlarging HSBC’s share of

the credit card, mortgage and unsecured personal

lending markets and increasing deposit balances. In