HSBC 2006 Annual Report Download - page 418

Download and view the complete annual report

Please find page 418 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

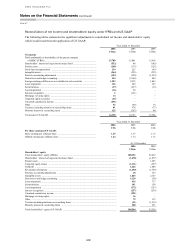

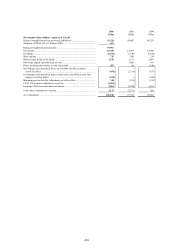

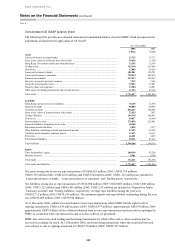

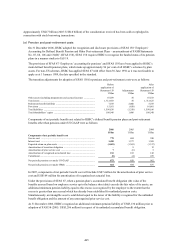

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

Note 47

416

Revaluation of property

IFRSs

• As allowed by the transition rules of IFRS 1, HSBC elected to adopt the value of all its properties held for its

own use as at 1 January 2004 as their ‘deemed cost’ at that date. Assets are carried at cost less any accumulated

depreciation and impairment losses. Freehold land is not depreciated.

• Investment properties are carried at current market values with gains or losses thereon recognised in the income

statement for the period. Investment properties are not depreciated.

US GAAP

• US GAAP does not permit revaluations of property, including investment property, although it requires

recognition of asset impairment. Any realised surplus or deficit is, therefore, reflected in net income upon

disposal of the property. Depreciation is charged on all properties based on cost.

Impact

• Under IFRSs, the value of property held for own use reflects revaluation surpluses recorded prior to 1 January

2004. Consequently, the values of tangible fixed assets and shareholders' equity are lower under US GAAP than

under IFRSs.

• There is a correspondingly lower depreciation charge and higher net income under US GAAP, partially offset by

higher gains (or smaller losses) on the disposal of fixed assets.

• For investment properties, net income under US GAAP does not reflect the gain or loss recorded under IFRSs

for the period.

Restructuring provisions

IFRSs

• In accordance with IAS 37, ‘Provisions, Contingent Liabilities and Contingent Assets’, provisions are made for

any direct costs arising from a business that management is committed to restructure, sell or terminate; has a

detailed formal plan and has raised a valid expectation of carrying out that plan.

US GAAP

• SFAS 146, ‘Accounting for Costs Associated with Exit or Disposal Activities’, requires that the fair value of a

liability for a cost associated with an exit or disposal activity be recognised when the liability is incurred.

Accordingly, provisions are recognised upon the implementation of the restructuring plan.

Impact

• The recognition of costs associated with plans to restructure and streamline operations is earlier under IFRSs

than under US GAAP, for example, where there is a time lag between developing and communicating a formal

plan, and putting it into practice. This resulted in marginally higher net income and shareholders’ equity under

US GAAP in 2005.

Consolidation of special purpose entities or variable interest entities

IFRSs

• Under the IASB’s Standing Interpretations Committee (‘SIC’) Interpretation 12 (‘SIC-12’), a special purpose

entity (‘SPE’) should be consolidated when the substance of the relationship between an enterprise and the SPE

indicates that the SPE is controlled by that entity.

US GAAP

• FASB Interpretation No. 46 (revised December 2003), ‘Consolidation of Variable Interest Entities’ (‘FIN 46R’),

requires consolidation of variable interest entities (‘VIE’s) in which HSBC is the primary beneficiary and

disclosures in respect of all other VIEs in which it has a significant variable interest.

• A VIE is an entity in which equity investors hold an investment that does not possess the characteristics of a

controlling financial interest or does not have sufficient equity at risk for the entity to finance its activities.