HSBC 2006 Annual Report Download - page 410

Download and view the complete annual report

Please find page 410 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

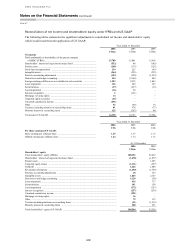

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

Note 47

408

Non-trading transactions

• Non-trading transactions, which were those undertaken for hedging purposes as part of HSBC’s risk

management strategy against cash flows, assets, liabilities or positions, were measured on an accrual basis.

Non-trading transactions included qualifying hedges and positions that synthetically altered the characteristics

of specified financial instruments.

• Non-trading transactions were accounted for on an equivalent basis to the underlying assets, liabilities or net

positions. Any gains or losses arising were recognised on the same basis as those arising from the related assets,

liabilities or positions.

• To qualify as a hedge, a derivative was required effectively to reduce the price, foreign exchange or interest rate

risk of the asset, liability or anticipated transaction to which it was linked and be capable of designation as a

hedge at inception of the derivative contract. Accordingly, changes in the market value of the derivative were

required to be highly correlated to changes in the market value of the underlying hedged item at inception of the

hedge and over the life of the hedge contract. If these criteria were met, the derivative was accounted for on the

same basis as the underlying hedged item. Derivatives used for hedging purposes included swaps, forwards and

futures. Interest rate swaps were also used to alter synthetically the interest rate characteristics of financial

instruments. In order to qualify for synthetic alteration, a derivative instrument had to be linked to specific

individual, or pools of similar, assets or liabilities by the notional principal and interest rate risks of the

associated instruments, and had to achieve a result that was consistent with defined risk management objectives.

If these criteria were met, accruals based accounting was applied, i.e. income or expense was recognised and

accrued to the next settlement date in accordance with the contractual terms of the agreement.

• Any gain or loss arising on the termination of a qualifying derivative was deferred and amortised to earnings

over the original life of the terminated contract. Where the underlying asset, liability or position was sold or

terminated, the qualifying derivative was immediately marked to market and any gain or loss arising was taken

to the income statement.

US GAAP

• The accounting under SFAS 133 ‘Accounting for derivative instruments and hedging activities’ is generally

consistent with that under IAS 39, which HSBC has followed in its IFRSs reporting from 1 January 2005, as

described above. However, specific assumptions regarding hedge effectiveness under US GAAP are not

permitted by IAS 39.

• The requirements of SFAS 133 have been effective from 1 January 2001.

• During 2006, HSBC’s US operating subsidiaries discontinued the use of the ‘shortcut method’. The US GAAP

‘shortcut method’ permits an assumption of zero ineffectiveness in hedges of interest rate risk with an interest

rate swap provided specific criteria have been met. IAS 39 does not permit such an assumption, requiring a

measurement of actual ineffectiveness at each designated effectiveness testing date.

• However, IFRSs allow greater flexibility in the designation of the hedged item. Under US GAAP, all contractual

cash flows must form part of the designated relationship, whereas IAS 39 permits the designation of identifiable

benchmark interest cash flows only.

• Certain issued structured notes are classified as trading liabilities under IFRSs, but not under US GAAP. Under

IFRSs, these notes will be held at fair value, with changes in fair value reflected in the income statement. Under

US GAAP, if the embedded derivative would otherwise require bifurcation, an irrevocable election may be made

to initially and subsequently measure the entire issued note at fair value, with changes in fair value recognised

through income. This election is made under US GAAP when the underlying issued notes are classified as

trading liabilities under IFRS. If the embedded derivative is clearly and closely related to the host contract, the

issued note will be held at amortised cost in its entirety, with changes in the amortised cost reflected in the

income statement.

• Under US GAAP, derivatives receivable and payable with the same counterparty may be reported net on the

balance sheet when there is an executed ISDA Master Netting Arrangement covering enforceable jurisdictions.

These contracts do not meet the requirements for offset under IAS 32 and hence are presented gross on the

balance sheet under IFRSs.