HSBC 2006 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

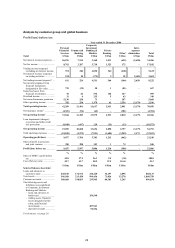

33

cent. On an underlying basis, pre-tax profits grew by

8 per cent. Underlying net operating income

increased by 9 per cent, in line with operating

expenses. Commercial Banking delivered a third

successive year of growth, driven by strong balance

sheet growth in the UK and organic expansion in

Turkey. Record profits in Private Banking were

driven by strong client asset inflows, a more

sophisticated product mix and lending growth.

Corporate, Investment Banking and Markets made

encouraging gains in trading activities, and operating

expenses rose in line with net operating income. In

Personal Financial Services, net operating income

growth slowed as HSBC tightened its underwriting

criteria on unsecured credit. An emphasis on deposit,

wealth and insurance products contributed to an

increase in costs, which were driven by

infrastructure investment both in the physical

environment and direct channels.

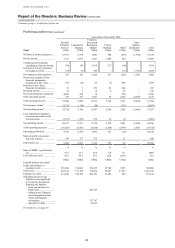

The following commentary is on an underlying

basis.

Personal Financial Services reported a pre-tax

profit of US$1,909 million, 2 per cent lower than in

2005. Net operating income rose by 4 per cent and

loan impairment charges increased by slightly more

than revenues as increasing numbers of debtors

sought formal protection from their obligations.

Costs grew by 7 per cent, reflecting investment in

infrastructure throughout the region, and the cost

efficiency ratio rose by 1.2 percentage points to

59.2 per cent.

In the UK, HSBC responded to concerns over

high levels of consumer indebtedness and the growth

in personal bankruptcies and IVAs by adopting more

selective underwriting criteria and reducing credit

origination. Revenues from credit-related insurance

declined as a consequence. In response, HSBC

increased its focus on non credit-related income

streams, particularly savings and high-value current

accounts. Strong balance growth in these products

was achieved through marketing initiatives,

competitive pricing and the success of innovative

propositions such as the packaged ‘Plus’ and

‘Passport’ current accounts, the latter supported by

the implementation during the year of a more refined

approach to customer segmentation.

Considerable strategic attention was given to

enhancing product distribution and channel

management. The branch refurbishment programme

continued and improvements were made to direct

banking, notably the introduction of self-service

machines and the upgrading of cash machine service

offerings. HSBC’s internet offering was also

enhanced to offer personalised content and sales

capabilities, with improved customer accessibility.

In France, a marked improvement in brand

awareness after the 2005 rebranding to ‘HSBC

France’, supported by competitive pricing, aided the

recruitment of target customers and consequential

balance sheet growth, most notably in residential

property lending. Despite this growth, there was a

decline in profit before tax, due to competitive

pressures on margin and the time lag between

incurring costs on customer acquisition and earning

incremental revenue from future opportunities to

cross-sell.

In Turkey profit before tax declined by 2 per

cent, as revenue growth was offset by investment

costs. Organic development was furthered by the

opening of 37 new branches during the year,

bringing the total to 193, and a number of marketing

initiatives to build brand awareness. Balance sheet

and revenue growth accelerated as a result, as did

customer recruitment. Overall customer numbers

stood at 2.3 million at the end of 2006.

Net interest income increased by 5 per cent to

US$5,653 million, substantially from balance sheet

growth throughout the region.

In the UK, net interest income was driven by

growth in savings, deposit and current accounts, with

higher balances achieved through targeted sales and

marketing efforts. Interest income from credit cards

and mortgages also increased.

A focus on liabilities helped boost new UK

savings account volumes markedly in a buoyant yet

highly competitive savings market. HSBC’s

competitive internet-based products were the key

driver of growth. Cash invested in First Direct’s

‘e-savings’ product trebled; balances in HSBC’s

‘Online Saver’ increased sixfold. Overall, average

savings balances, excluding money market

investments, increased by 28 per cent and net

interest income rose by 25 per cent.

Current account balances in the UK increased

by 6 per cent to US$26.0 billion. Within this, the

proportion of value-added packaged current accounts

attracting fees rose significantly. The number of

HSBC’s fee-based accounts more than doubled

during 2006. In aggregate, packaged current account

balances increased by 25 per cent and represented

nearly half of the overall increase in current

accounts. Spreads remained broadly in line with

2005.

Average UK credit card balances rose by 5 per

cent, to US$13.7 billion, driven by promotional

campaigns and marketing. Growth was strongest in