HSBC 2006 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: Financial Review (continued)

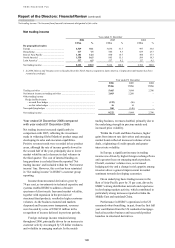

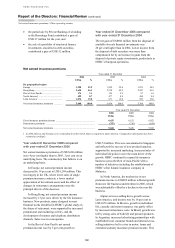

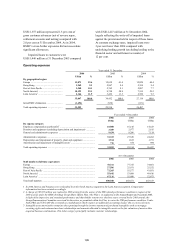

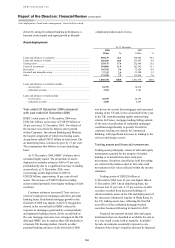

Loan impairment charges / Operating expenses

138

in delinquency and loss severity, projecting the

probable impact of re-pricing ARMs, and

incorporating the effect of re-pricing on parallel

second lien loans. Further details are provided on

page 189. Credit delinquency in other parts of the

mortgage portfolio and in other US businesses rose

modestly, driven by unusually low levels at the end

of 2005, and growing loan maturity in 2006.

Partially offsetting the effects of credit deterioration

were a decline in bankruptcy filings following the

surge at the end of 2005, relatively low

unemployment and a fall in exposure estimated to

result from hurricane Katrina.

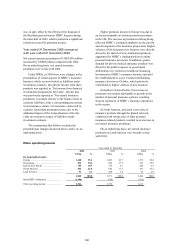

In Latin America, the rise in impairment charges

by 24 per cent to US$938 million was largely

recorded in Mexico and, to a lesser extent, Brazil

and Argentina. In Mexico, strong loan growth,

particularly in 2006, led to increased loan

impairment charges. In Brazil, the credit weaknesses

seen in 2005 and the first half of 2006, particularly

in the consumer market, were mitigated by changes

to underwriting procedures. Net charges in Brazil

increased by 7 per cent compared with 54 per cent in

2005 and declined in the second half of 2006

compared with the first half. In Argentina, net

charges rose as a result of the non-recurrence of

releases and recoveries in 2005.

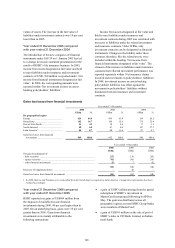

The aggregate outstanding customer loan

impairment allowances at 31 December 2006 of

US$13,578 million represented 1.6 per cent of gross

customer advances (net of reverse repos and

settlement accounts), compared with 1.5 per cent at

the same time in 2005.

Impaired loans to customers were

US$13,785 million at 31 December 2006 compared

with US$11,446 million at 31 December 2005. On a

constant currency basis, impaired loans were 14 per

cent higher than in 2005 compared with lending

growth (excluding loans to the financial sector and

settlement accounts) of 10 per cent.

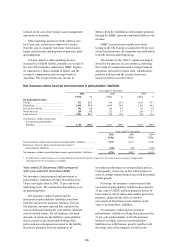

Year ended 31 December 2005 compared

with year ended 31 December 2004

During 2005, the underlying growth in customer

lending excluding loans to the financial sector and

the impact of grossing adjustments required from

1 January 2005 under IFRSs, was 12 per cent.

Personal lending accounted for 63 per cent of this

increase, principally in mortgages, credit cards and

other personal lending products. At 31 December

2005, personal lending accounted for 56 per cent of

the customer loan portfolio, in line with 2004. The

proportion of the portfolio attributable to corporate

and commercial lending was augmented by the

IFRSs adjustment noted above. Residential

mortgages comprised 56 per cent of the personal

lending portfolio.

The charge for loan impairment adjusts the

balance sheet allowance for loan impairment to the

level that management deems adequate to absorb

actual and inherent losses in the Group’s loan

portfolios. The majority of the Group’s loan

impairment charges were determined on a portfolio

basis, employing statistical calculations using roll

rate methodologies. The total charge for loan

impairment and other credit risk provisions in 2005

was US$7,801 million compared with a total charge

of US$6,191 million in 2004, a rise of 26 per cent.

This reflected:

• underlying growth in lending of 12 per cent;

• a weakening credit environment in the UK and

Brazil but an improved credit experience in the

US; and

• the non-recurrence of the 2004 net release of

general provision of US$498 million.

In the US, the underlying trend in loan

impairment charges was favourable compared with

2004, notwithstanding the negative effect on loan

impairment charges of hurricane Katrina and a surge

in personal bankruptcies in October ahead of new

legislation making such declarations more onerous.

This was due to a change in portfolio mix towards

higher quality lending and a positive economic

environment.

In the UK, credit costs rose following an

expansion in personal lending, which was

accompanied by an increase in delinquencies as the

economy slowed during 2005. This was evidenced

by rising personal bankruptcy, caused in part by

legislative changes which facilitated debt

reconstruction procedures, an increase in

unemployment and higher levels of personal debt. In

Hong Kong, the credit environment remained

benign, with falling bankruptcies contributing to a

modest reduction in loan impairment allowances in

the personal sector. A fall in releases in the corporate

sector, however, contributed to a modest charge for

loan impairment as compared with a net release in

2004. In the Rest of Asia-Pacific, continuing releases

and recoveries partly offset the impact of lending

growth in the region. Higher charges in the personal

sector in Brazil followed intense competitive

pressure in the consumer segment, where significant

increases in the availability of credit led to customers

becoming over-indebted.

The aggregate customer loan impairment

allowances at 31 December 2005 of