HSBC 2006 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

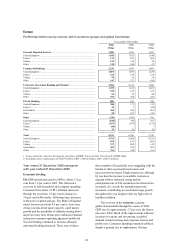

Europe > 2006

34

M&S branded cards, which represented 4 percentage

points of the increase, driven by an increased sales

focus which included extensive media advertising.

This was partly offset by declining balances within

the store cards business and the cards business of

HFC Bank Ltd (‘HFC’), reflecting HSBC’s more

restricted credit appetite. Spreads increased modestly

compared with 2005.

Average UK mortgage balances rose by 11 per

cent to US$68.9 billion, primarily in fixed rate

mortgages. Growth was achieved through

competitive pricing and targeted marketing

strategies, including the launch of new fixed,

discount and tracker-rate mortgages during the year.

A slight narrowing of spreads reflected a change in

mix away from variable rate mortgages to fixed rate

mortgages, and the competitive positioning referred

to above.

Average unsecured lending balances in the UK

declined by 4 per cent, reflecting HSBC’s decision

to contain growth through stricter underwriting

criteria. Spreads narrowed, following the

introduction in 2005 of preferential pricing for

lower-risk customers, and a change in mix towards

higher-value but lower-yielding loans.

In France, net interest income fell by 8 per cent.

Spreads narrowed as older higher-yielding

investments matured, while competitive pricing

reduced lending yields, particularly in the residential

mortgage market. These pressures on margin were

only partially offset by strong balance sheet growth.

Marketing campaigns building on the ‘HSBC

France’ brand aided strong sales and customer

recruitment, most notably in residential property

lending and current accounts and also increased

future cross-selling opportunities.

In Turkey, net interest income rose by 14 per

cent. Lending grew strongly, substantially funded by

deposit growth. Overall, deposit balances rose by

over 50 per cent, largely driven by customer

recruitment aided by the branch network expansion

referred to above. Spreads widened following

increases in overnight interest rates and the value of

funds rose as a consequence. Marketing initiatives

and cross-sales with credit card customers helped

more than double average unsecured lending

balances. Mortgage lending was also strong, with a

60 per cent increase in balances. Credit card

balances rose by 22 per cent, with growth dampened

by credit calming measures imposed by government

regulation.

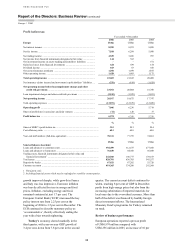

Net fee income increased by 8 per cent to

US$2,533 million. In the UK, rising sales of fee-

earning packaged current accounts, travel money and

investment products drove fee growth. Fees from

unsecured lending also rose. These benefits were

partly offset by lower creditor protection income,

reflecting the steps taken by HSBC to constrain

lending growth. Reduced loan sales and smaller

average loans (the result of this initiative) led to both

lower insurance sales and a reduction in average

premiums.

In France, banking fees rose through higher

sales of packaged current accounts. Transactional

and overdraft fees and insurance distribution fees

also increased, reflecting growth in the customer

base. In Turkey, strong growth in lending volumes

and, to a lesser extent, credit cards, helped drive fee

income growth. Additional sales staff were recruited

to reinforce the emphasis on wealth management,

and the launch of new pension products also helped

boost fees.

In 2006, MasterCard became publicly listed

through an IPO, and the US$37 million gain from

financial investments mainly reflected Personal

Financial Services’ share of the proceeds of the IPO.

Responding to changes in work and shopping

patterns among its customers and the increasing

acceptance of direct channels. HSBC appraised its

UK property portfolio during the year, and higher

other operating income reflected Personal Financial

Services’ share of revenue from branch sale and

lease-back transactions. Personal Financial Services’

US$37 million share of income on the sale of

HSBC’s stake in The Cyprus Popular Bank was also

included within other operating income.

Lower sales of life and creditor repayment

protection, which were driven by the constraints on

personal lending growth referred to above, and a

change in reinsurance arrangements at the end of

2005, contributed to the decrease in net earned

insurance premiums. Lower sales of investment-

linked insurance products, together with the effect of

market movements on related insurance and

investment assets, contributed to the decline in net

income from financial instruments designated at fair

value. This was largely offset by a corresponding

decrease in net insurance claims and movements in

policyholders’ liabilities.

Loan impairment charges and other credit risk

provisions of US$1,838 million were 6 per cent

higher than in 2005, largely reflecting lending

growth in the region.

In the UK, the 8 per cent rise in loan impairment

charges was broadly in line with lending growth.

Actions taken on underwriting and collection

activities mitigated a continuation of the rising trend