HSBC 2006 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

83

robust, rising 11 per cent. Unemployment fell by

0.5 per cent to 4.9 per cent in 2005, with 2 million

new jobs created. The Federal Reserve’s favoured

inflation measure, the core personal consumption

expenditure deflator, was contained, rising 2 per cent

in 2005. Headline inflation in 2005 was higher due

to increased energy prices, as the full year consumer

price index rose 3.4 per cent. The Federal Reserve

raised interest rates eight times during the year, from

2.25 per cent to 4.25 per cent. 10-year bond yields

and equity markets rose moderately during 2005 as

the US dollar strengthened, ending the year at

US$1.18 to the euro compared with US$1.35 at the

end of 2004.

Canada’s growth was 2.9 per cent in 2005, as

strong employment growth and, late in the year,

rising earnings, boosted consumer spending. The

unemployment rate fell to 6.4 per cent, the lowest

level since 1976. In the second half of the year,

exports rose, boosted by strong global demand. In

the energy sector, investment and profits rose

strongly as oil prices soared, with the positive

economic impact being most pronounced in Western

Canada. Gasoline prices lifted headline inflation to a

peak of 3.4 per cent in September, but it fell back

sharply and core inflation was 1.6 per cent by the

year-end. Having been kept on hold for much of the

year, interest rates were raised by 75 basis points

between September and December. The BoC has

indicated that further increases may be required.

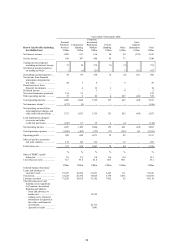

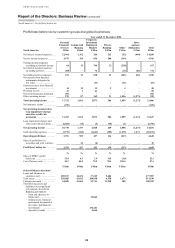

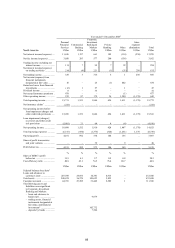

Review of business performance

HSBC’s operations in North America reported a pre-

tax profit of US$5,915 million, compared with

US$5,268 million in 2004, representing an increase

of 12 per cent. On an underlying basis, pre-tax

profits grew by 11 per cent and represented around

28 per cent of HSBC’s equivalent total profit. In the

US, the benefits from strong deposit growth in

Personal Financial Services were partly negated by

narrowing spreads on lending in the rising interest

rate environment. In Commercial Banking, growth in

pre-tax profits was largely driven by lending and

deposit balance growth and improved liability

interest margins. In Corporate, Investment Banking

and Markets, growth in revenues was offset by

investment expenditure to build the platform and

infrastructure required for future growth.

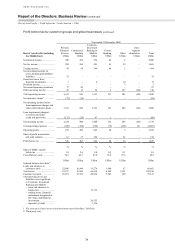

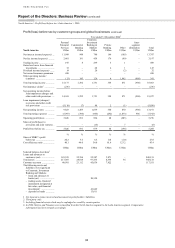

The commentary that follows is on an

underlying basis.

Personal Financial Services, including the

consumer finance business, generated a pre-tax

profit of US$4,181 million, 9 per cent higher than in

2004. Under IFRSs, from 1 January 2005, HSBC

changed the accounting treatment for certain debt

issued and related interest rate swaps. This did not

change the underlying economics of the transactions.

The resulting revenues of US$618 million in 2004

are excluded from the following commentary. In

addition, interest income earned on mortgage

balances held on HSBC’s balance sheet pending sale

into the US secondary mortgage market was reported

under trading income. In 2004 this was reported in

net interest income. This difference in treatment is

also excluded from the following commentary.

In the US, profit before tax rose 28 per cent to

US$3,853 million. The rise in profit was largely

driven by widening deposit spreads, strong deposit

and customer loan growth and higher fee income,

partly offset by lower asset spreads due to higher

funding costs. Loan impairment charges fell,

notwithstanding the higher charges due to the

combined effects of hurricane Katrina and changes

in bankruptcy legislation. Profit before tax in Canada

rose 93 per cent as net interest income increased due

to strong asset and liability growth and widening

deposit spreads.

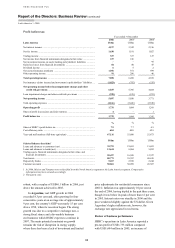

Net interest income grew by 3 per cent to

US$11,636 million, mainly from increases in both

the US and Canada. In the US, net interest income

rose by 3 per cent, largely driven by higher deposit

balances and widening deposit spreads. Average

loan balances grew strongly, in particular from prime

and non-prime residential mortgages. With ongoing

strong demand for unsecured lending, the credit

card, private label card and personal non-credit card

portfolios continued to grow. The benefits of strong

asset growth were largely offset by lower spreads as

interest rates rose.

Additional resources were focused on the core

retail banking business in the US as high priority

was given to growing the deposit base. Investment in

the retail branch network continued, to ensure a

presence in locations with high growth potential.

During the year, 27 new branches were opened, each

tailored to meet the needs of the local market. The

launch of two new deposit products, HSBC’s first

national savings product, ‘Online Savings’, and

‘HSBC Premier Savings’, augmented by a 45 per

cent rise in new personal account openings, led to a

4 per cent growth in average deposit balances to

US$26.7 billion.

Overall, average mortgage balances, including

US$3.3 billion held for resale, rose by 27 per cent to

US$112.1 billion. This was due to the significant

expansion of ARMs originated during 2004 in the

US bank and strong growth within the mortgage

services and branch-based consumer lending