HSBC 2006 Annual Report Download - page 230

Download and view the complete annual report

Please find page 230 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

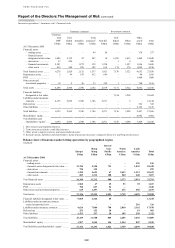

HSBC HOLDINGS PLC

Report of the Directors: The Management of Risk (continued)

Insurance operations > Life insurance / Non-life insurance / Insurance risk

228

Risk management of insurance

operations

(Audited)

Within its service proposition, HSBC offers its

customers a wide range of insurance products, many

of which complement other bank and consumer

finance products.

Both life and non-life insurance is underwritten,

principally in the UK, Hong Kong, Mexico, Brazil,

the US and Argentina.

Life insurance business

(Audited)

There are a number of major sub-categories of life

assurance business, of which the main ones are

discussed below:

Life insurance contracts with discretionary

participation features allow policyholders to

participate in the profits generated from such

business in addition to providing cover on death. The

largest portfolio, which is in Hong Kong, is a book

of endowment and whole-life policies, with annual

bonuses awarded to policyholders. Market risk is

managed in conjunction with other risks through the

investment policy and adjustment to bonus rates. In

practice this means that the majority of the market

risk is borne by policyholders. The main risk

associated with this product is the value of assigned

assets falling below that required to support benefit

payments. HSBC manages this risk by conducting

regular actuarial investigations on the sustainability

of the bonus rates.

Credit life insurance provides protection in the

event of death or unemployment. Credit life

insurance business is written for banking and finance

products. The insurance risk relates to mortality and

morbidity risk which is restricted to the duration of

the loans advanced. Claims experience is required to

be monitored and premium rates adjusted

accordingly.

Annuities are contracts providing regular

payments of income from capital investment for

either a fixed period or during the annuitant’s

lifetime. Deferred annuities are those whose

payments to the annuitant begin at a designated

future date while, for immediate annuities, payments

begin on inception of the policy. The principal risks

of annuity business relate to mortality and market

risk, the latter arising from the need to match

investments to the anticipated cash flow profile of

the policies. The investment strategy seeks to match

the anticipated cash flow profile, and the mortality

risk is regularly monitored.

Term assurance provides cover in the event of

death. Critical illness cover provides cover in the

event of critical illness. The major components of

the ‘Term assurance and other long-term contracts’

category are term assurance and critical illness

policies written in the UK. The principal risks are in

respect of mortality and morbidity. These risks are

managed through a combination of underwriting

practices, premium adjustment in light of changes in

experience and reinsurance.

Linked life insurance business pays benefits to

the policyholder which is typically determined by

reference to the value of the investments supporting

the policy. For linked life insurance business, the

market risk is substantially borne by policyholders.

The principal risk retained by HSBC relates to

expenses incurred in managing this product. They

are recovered by management charges deducted

from the policyholder over the lifetime of the policy.

However, if the policy is terminated early,

deductions made to that point may be less than the

costs incurred for managing the product. This risk is

mitigated by retaining the ability to apply charges on

early surrender. Mortality, disability and morbidity

risks can also arise with this product and are

managed by applying the techniques set out above

for non-linked lines of business.

Non-life insurance business

(Audited)

Non-life insurance contracts include motor, fire and

other damage, accident and health, repayment

protection and commercial and liability business.

Within accident and health insurance, potential

accumulations of personal accident risks are

mitigated by the purchase of catastrophe reinsurance.

Motor insurance business covers vehicle

damage and liability for personal injury. Reinsurance

protection is required to be arranged where

necessary to avoid excessive exposure to larger

losses, particularly those relating to personal injury

claims.

Fire and other damage business is written in all

major markets, most significantly in Europe. The

predominant focus in most markets is insurance for

home and contents while cover for selected

commercial customers is largely written in Asian

and Latin American markets. Portfolios at risk from

catastrophic losses are required to be protected by

reinsurance in accordance with information obtained

from professional risk-modelling organisations.

A very limited portfolio of liability business is

written in major markets.