HSBC 2006 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

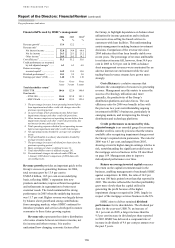

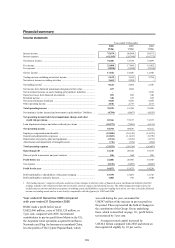

Report of the Directors: Financial Review (continued)

Critical accounting policies

112

• the amount and timing of expected receipts and

recoveries;

• the likely dividend available on liquidation or

bankruptcy;

• the extent of other creditors’ commitments

ranking ahead of, or pari passu with, HSBC and

the likelihood of other creditors continuing to

support the company;

• the complexity of determining the aggregate

amount and ranking of all creditor claims and

the extent to which legal and insurance

uncertainties are evident;

• the realisable value of security (or other credit

mitigants) and likelihood of successful

repossession;

• the likely deduction of any costs involved in

recovery of amounts outstanding;

• the ability of the borrower to obtain, and make

payments in, the currency of the loan if not

denominated in local currency; and

• when available, the secondary market price of

the debt.

Impairment losses are calculated by discounting

the expected future cash flows of a loan at its

original effective interest rate, and comparing the

resultant present value with the loan’s current

carrying amount.

The carrying amount of impaired loans on the

balance sheet is reduced through the use of an

allowance account. HSBC’s policy requires a review

of the level of impairment allowances on individual

facilities above materiality thresholds at least half-

yearly, or more regularly when individual

circumstances require. This normally includes a

review of collateral held (including re-confirmation

of its enforceability) and an assessment of actual and

anticipated receipts.

Collectively assessed loans

Impairment is assessed on a collective basis in two

circumstances:

• to cover losses which have been incurred but

have not yet been identified on loans subject to

individual assessment; and

• for homogeneous groups of loans that are not

considered individually significant.

Incurred but not yet identified impairment

Individually assessed loans for which no evidence of

loss has been specifically identified on an individual

basis are grouped together according to their credit

risk characteristics for the purpose of calculating an

estimated collective loss. This reflects impairment

losses incurred at the balance sheet date which will

only be individually identified in the future.

The collective impairment allowance is

determined after taking into account:

• historical loss experience in portfolios of similar

credit risk characteristics (for example, by

industry sector, loan grade or product);

• the estimated period between impairment

occurring and the loss being identified and

evidenced by the establishment of an

appropriate allowance against the individual

loan; and

• management’s experienced judgement as to

whether current economic and credit conditions

are such that the actual level of inherent losses is

likely to be greater or less than that suggested by

historical experience.

The period between a loss occurring and its

identification is estimated by local management for

each identified portfolio.

Homogeneous groups of loans

For homogeneous groups of loans that are not

considered individually significant, two alternative

methods are used to calculate allowances on a

portfolio basis:

When appropriate empirical information is

available, HSBC utilises roll-rate methodology. This

methodology employs statistical analysis of

historical trends of delinquency and default to

estimate the likelihood that loans will progress

through the various stages of delinquency and

ultimately prove irrecoverable. The estimated loss is

the difference between the present value of expected

future cash flows, discounted at the original effective

interest rate of the portfolio, and the carrying amount

of the portfolio. Current economic conditions are

also evaluated when calculating the appropriate level

of allowance required to cover inherent loss. In

certain highly developed markets, sophisticated

models also take into account behavioural and

account management trends as revealed in, for

example, bankruptcy and rescheduling statistics.

In other cases, when the portfolio size is small

or when information is insufficient or not reliable

enough to adopt a roll-rate methodology, HSBC

adopts a formulaic approach which allocates

progressively higher percentage loss rates the longer

a customer’s loan is overdue. Loss rates are