Entergy 2002 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2002 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84

|

|

76

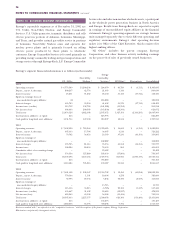

Two of the unconsolidated 50/50 joint ventures, Entergy-

Koch and RS Cogen, have obtained debt financing for their

operations. As of December 31, 2002, the debt financing

outstanding for those two entities totals $818 million, which

is included in the liability figures given above. This debt is

nonrecourse to Entergy.

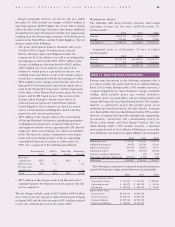

RELATED-PARTY TRANSACTIONS AND GUARANTEES

During 2002 and 2001, Entergy procured various services from

Entergy-Koch consisting primarily of pipeline transportation

services for natural gas and risk management services for

electricity and natural gas. The total cost of such services in 2002

and 2001 was approximately $11.2 million and $7.8 million,

respectively. Entergy’s operating transactions with its other equity

method investees were not material in 2002, 2001, or 2000.

One of the contracts transferred to Entergy-Koch by Entergy’s

power marketing and trading business is backed by an Entergy

Corporation guarantee authorized in the amount of $35 million.

The guarantee term is through the expiration of the underlying

contract, which ends in 2018.

EntergyShaw is currently constructing the Harrison County

project for Entergy. Entergy has guaranteed the obligations of

EntergyShaw to construct the plant, and Entergy’s maximum

liability on the guarantee is $232.5 million. The project is

expected to be completed in 2003.

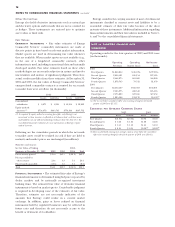

NOTE 14. ACQUISITIONS AND DISPOSITIONS

ASSET ACQUISITIONS

Vermont Yankee

In July 2002, Entergy’s Non-Utility Nuclear business purchased

the 510 MW Vermont Yankee nuclear power plant located in

Vernon, Vermont, from Vermont Yankee Nuclear Power

Corporation for $180 million. Entergy received the plant,

nuclear fuel, inventories, and related real estate. The liability

to decommission the plant, as well as related decommissioning

trust funds of approximately $310 million, was also transferred

to Entergy. The acquisition included a 10-year power purchase

agreement (PPA) under which the former owners will buy the

power produced by the plant, which is through the expiration

of the current operating license for the plant. The PPA

includes an adjustment clause where the prices specified in

the PPA will be adjusted downward annually, beginning in

2006, if power market prices drop below the PPA prices.

The acquisition was accounted for using the purchase

method. The results of operations of Vermont Yankee

subsequent to the purchase date have been included in

Entergy’s consolidated results of operations. The purchase

price has been preliminarily allocated to the assets acquired

and liabilities assumed based on their estimated fair values on

the purchase date. The allocation was based on preliminary

information and the final allocation may differ, although

management does not expect the difference to be material.

Indian Point 2

In September 2001, Entergy’s Non-Utility Nuclear business

acquired the 970 MW Indian Point 2 nuclear power plant

located in Westchester County, New York from Consolidated

Edison. Entergy paid approximately $600 million in cash at the

closing of the purchase and received the plant, nuclear fuel,

materials and supplies, a purchase power agreement (PPA), and

assumed certain liabilities. On the second anniversary of the

Indian Point 2 acquisition, Entergy’s nuclear business will also

begin to pay NYPA $10 million per year for up to 10 years in

accordance with the Indian Point 3 purchase agreement. Under

the PPA, Consolidated Edison will purchase 100% of Indian

Point 2’s output through 2004. Consolidated Edison transferred

a $430 million decommissioning trust fund, along with the

liability to decommission Indian Point 2 and Indian Point 1, to

Entergy. Entergy acquired Indian Point 1 in the transaction,

a plant that has been shut down and in safe storage since

the 1970s.

The acquisition was accounted for using the purchase method.

The results of operations of Indian Point 2 subsequent to the

purchase date have been included in Entergy’s consolidated

results of operations. The purchase price has been allocated to

the acquired assets, including identifiable intangible assets, and

liabilities assumed based on their estimated fair values on the

purchase date. Intangible assets are being amortized straight-line

over the remaining life of the plant.

Indian Point 3 and FitzPatrick

In November 2000, Entergy’s Non-Utility Nuclear business

acquired from NYPA the 825 MW James A. FitzPatrick nuclear

power plant near Oswego, New York, and the 980 MW Indian

Point 3 nuclear power plant located in Westchester County,

New York, in exchange for $50 million at closing and notes to

NYPA with payments totaling $906 million. Entergy will also be

required to make certain additional payments to NYPA in the

event that the plants’ license lives are extended.

The acquisition encompassed the nuclear plants, materials

and supplies, and nuclear fuel, as well as the assumption of

$124 million in liabilities. The purchase agreement provides

that NYPA will purchase a substantial majority of the output of

the units at specified prices through 2004. The purchase

agreement also provides that NYPA will retain the decommis-

sioning obligations and related trust funds through the

original license expiration date (approximately 2015). At that

time, NYPA is required either to transfer the decommissioning

liability to Entergy along with a specified amount in the

decommissioning trust funds, or to retain Entergy to perform

decommissioning services for a specified price that may be

limited by the amount in the trust. In the purchase price

allocation, Entergy recorded an asset representing its estimate

of the net present value of the decommissioning contract

obtained in the acquisition, based on an independent

decommissioning cost study and other projections. The asset

increases by monthly accretion based on the discount rate

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS continued