Entergy 2002 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2002 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

would face in implementing this proposal, it is improbable that

the County could condemn or municipalize Indian Point.

LITIGATION

Entergy and its subsidiaries are involved in the ordinary course

of business in a substantial amount of employment, asbestos,

hazardous material and other environmental and rate-related

proceedings and litigation, a significant portion of which

originates in Louisiana, Mississippi, and Texas. Entergy uses

legal and appropriate means to contest litigation threatened

or filed against it, but the litigation environment in these states

poses a significant business risk.

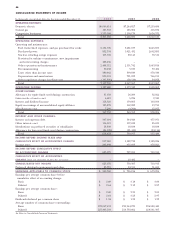

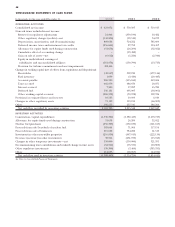

CRITICAL ACCOUNTING ESTIMATES

The preparation of Entergy’s financial statements in conformity

with generally accepted accounting principles requires man-

agement to make estimates and judgments that can have a

significant effect on reported financial position, results of

operations, and cash flows. Management has identified the

following estimates as critical accounting estimates because

they are based on assumptions and measurements that involve

an unusual degree of uncertainty, and there is the potential

that different assumptions and measurements could produce

estimates that are significantly different than those recorded in

Entergy’s financial statements.

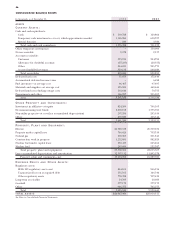

NUCLEAR DECOMMISSIONING COSTS

Entergy owns a significant number of nuclear generation facil-

ities in both its U.S. Utility and Non-Utility Nuclear business

units. Regulations require that these facilities be decommis-

sioned after the facility is taken out of service, and funds are

collected and deposited in trust funds during the facilities’

operating lives in order to provide for this obligation. Entergy

conducts periodic decommissioning cost studies (typically

updated every three to five years) to estimate the costs that will

be incurred to decommission the facilities. Note 9 to the

consolidated financial statements contains details regarding

Entergy’s most recent studies and the obligations recorded

by Entergy related to decommissioning. The following key

assumptions have a significant effect on these estimates:

COST ESCALATION FACTORS –Entergy’s decommissioning

revenue requirement studies include an assumption that

decommissioning costs will escalate over present cost levels

by annual factors ranging from 3.0% to 5.5%. A 50 basis

point change in this assumption could change the ultimate

cost of decommissioning a facility by as much as 11.0%.

TIMING –In projecting decommissioning costs, two assump-

tions must be made to estimate the timing of plant decom-

missioning. First, the date of the plant’s retirement must be

estimated. The expiration of the plant’s operating license is

typically used for this purpose, or an assumption could be

made that the plant will be relicensed and operate for some

time beyond the original license term. Second, an assump-

tion must be made whether decommissioning will begin

immediately upon plant retirement, or whether the plant

will be held in “safestore” status for later decommissioning,

as permitted by applicable regulations. While the impact of

these assumptions cannot be determined with precision,

assuming either license extension or use of a “safestore”

status can significantly decrease the present value of

these obligations.

SPENT FUEL DISPOSAL –Federal regulations require the

Department of Energy to provide a permanent repository

for the storage of spent nuclear fuel, and recent legislation

has been passed by Congress to develop this repository

at Yucca Mountain, Nevada. However, until this site is

available, nuclear plant operators must provide for interim

spent fuel storage on the nuclear plant site, which can

require the construction and maintenance of dry cask

storage sites or other facilities. The costs of developing and

maintaining these facilities can have a significant impact

(as much as 16% of estimated decommissioning costs).

Entergy’s decommissioning studies include cost estimates

for spent fuel storage, except for ANO 1 and 2. A study

including these costs for ANO 1 and 2 is currently under-

way. However, these estimates could change in the future

based on the timing of the opening of the Yucca Mountain

facility, the schedule for shipments to that facility when it is

opened, or other factors.

TECHNOLOGY AND REGULATION –To date, there is limited

practical experience in the U.S. with actual decommis-

sioning of large nuclear facilities. As experience is gained

and technology changes, cost estimates could also change.

If regulations regarding nuclear decommissioning were to

change, this could have a potentially significant impact on

cost estimates. The impact of these potential changes is not

presently determinable. Entergy’s decommissioning cost

studies assume current technologies and regulations.

The implications of these estimates vary significantly between

Entergy’s U.S. Utility and Non-Utility Nuclear businesses.

Separate discussions of these implications by business unit follow.

U.S. Utility

Entergy collects substantially all of the projected costs of decom-

missioning the nuclear facilities in its U.S. Utility business unit

through rates charged to customers, except for portions of River

Bend, which is discussed in more detail below. The amounts

collected through rates, which are based upon decommissioning

cost studies, are deposited in decommissioning trust funds.

These collections plus earnings on the trust fund investments are

generally estimated to be sufficient to fund the future decom-

missioning costs. Accordingly, U.S. Utility decommissioning costs

have no impact on Entergy’s earnings, as accrued costs are offset

by earnings on trust funds and collections from customers. For

the U.S. Utility segment, if decommissioning cost study estimates

were changed and approved by regulators, collections from

customers would also change.

Approximately half of River Bend is not currently subject to

cost-based ratemaking. When Entergy Gulf States obtained the

MANAGEMENT’S FINANCIAL DISCUSSION AND ANALYSIS continued

38