eBay 2002 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2002 eBay annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

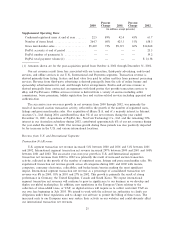

amendments to those reports as soon as reasonably practicable after we electronically Ñle or furnish such

materials to the U.S. Securities and Exchange Commission.

ITEM 2: PROPERTIES

On March 1, 2000, we entered into a Ñve-year lease for general oÇce facilities located in San Jose,

California. This Ñve-year lease is commonly referred to as a synthetic lease because it represents a form of

oÅ-balance sheet Ñnancing under which an unrelated third-party funds 100% of the costs of the acquisition

of the property and leases the asset to us as lessee. Under our lease structure, upon termination or

expiration, at our option, we must either purchase the property from the lessor for a predetermined amount

or sell the real property to a third party. Our San Jose lease consists of approximately 460,000 square feet

of oÇce space. As of December 31, 2002, we occupied approximately 314,000 square feet of this total

oÇce space and subleased additional space in the facility to third parties.

Payments under our lease are based on the $126.4 million cost of the property funded by the third

party and are adjusted as the London Interbank OÅered Rate, or LIBOR, Öuctuates. Under the terms of

the lease agreement, the lease terminates on March 1, 2005, unless extended to September 1, 2006. At any

time prior to the Ñnal 12 months of the lease term, we may, at our option, purchase the property for

approximately $126.4 million. If we elect not to purchase the property, we will undertake to sell the

facility to one or more third parties and have guaranteed to the lessor a residual value equal to

approximately 88% of the $126.4 million cost of the property. Our maximum exposure to loss is the entire

amount of $126.4 million if we default on any of certain lease obligations and Ñnancial covenants. If this

payment were made, we would then receive title to the property. At December 31, 2002, we had not made

a decision with respect to which option we will pursue at the end of the lease term. Management believes

that the contingent liability relating to the residual value guarantee will not have a material adverse eÅect

on our Ñnancial condition, results of operations or cash Öows. See ""Note 9 Ì Operating Lease

Arrangements'' and ""Note 6 Ì Derivative Instruments'' of the notes to our Consolidated Financial

Statements, which are incorporated by reference herein.

In January 2003, the Financial Accounting Standards Board, or FASB, issued FASB Interpretation

No. 46, or FIN 46, ""Consolidation of Variable Interest Entities.'' This interpretation of Accounting

Research Bulletin No. 51, ""Consolidated Financial Statements,'' addresses consolidation by business

enterprises of certain variable interest entities where there is a controlling Ñnancial interest in a variable

interest entity or where the variable interest entity does not have suÇcient equity at risk to Ñnance its

activities without additional subordinated Ñnancial support from other parties. This interpretation applies

immediately to variable interest entities created after January 31, 2003 and applies in the Ñrst year or

interim period beginning after June 15, 2003 to variable interest entities in which an enterprise holds a

variable interest that it acquired before February 1, 2003. We expect that the adoption of FIN 46 will

require us to include our San Jose facilities lease and potentially certain investments in our Consolidated

Financial Statements eÅective July 1, 2003. In connection with our San Jose facilities lease arrangement,

our balance sheet following the July 1, 2003 adoption of FIN 46 will reÖect changes to record assets of

$126.4 million, liabilities of $122.5 million and non-controlling interests of $3.9 million. In addition, our

post-adoption income statement will reÖect the reclassiÑcation of rent expense payments from operating

expenses to interest expense as well as the recognition of depreciation expense, within operating expenses,

for our use of the buildings. We estimate that the income statement impact of consolidating our San Jose

facilities lease will consist of a charge against earnings, net of taxes, of $5.6 million upon the adoption of

FIN 46 on July 1, 2003. This charge will reÖect the accumulated depreciation charges that would have

been recorded in previous periods had consolidation of the San Jose facilities been required. Additionally,

we have not decided whether we will keep the existing Ñnancing arrangement or purchase the San Jose

facilities. Whether or not we keep the existing Ñnancing arrangement, we anticipate recording additional

annual operating expenses of $1.7 million, net of taxes, for the recognition of depreciation expense on the

buildings. In the event we purchase the San Jose facilities, we will also pay $126.4 million, eliminate

Ñnancing payments and settle our two interest rate swaps we used to establish a Ñxed rate of interest for

$95 million of our Ñnancing arrangement. During the year ended December 31, 2002, our Ñnancing

16