Western Union 2008 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2008 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84

|

|

7373

Notes to Consolidated

Financial Statements

15. Borrowings

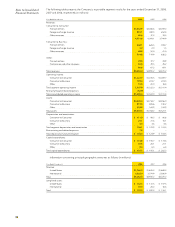

The Company’s outstanding borrowings at December 31, 2008 and 2007 consist of the following (in millions):

December 31, 2008 December 31, 2007

Carrying Value Fair Value (d) Carrying Value Fair Value (d)

Due in less than one year:

Commercial paper $ 82.9 $ 82.9 $ 338.2 $ 338.2

Term loan 500.0 500.0 — —

Floating rate notes, due November 2008

(a) — — 500.0 495.2

Due in greater than one year:

5.400% notes, net of discount, due 2011

(b) 1,042.8 962.9 1,002.8 1,012.0

5.930% notes, net of discount, due 2016

(c) 1,014.4 903.5 999.7 1,001.2

6.200% notes, net of discount, due 2036 497.4 391.4 497.3 473.1

Other borrowings 6.0 6.0 — —

Total borrowings $3,143.5 $2,846.7 $3,338.0 $3,319.7

(a) The floating rate notes were redeemed upon maturity on November 17, 2008.

(b) At December 31, 2008 and 2007, the Company held interest rate swaps related to the 5.400% notes due 2011 (“2011 Notes”) with an aggregate notional amount of

$550 million and $75 million, respectively. The carrying value of the 2011 Notes has been adjusted for the impact of these hedges. During the fourth quarter of 2008,

the Company terminated an aggregate notional amount of $195 million of interest rate swaps. The Company received cash of $10.7 million on the termination of these

swaps, the offset of which is reflected in “Borrowings” and will be reclassified as a reduction to “Interest expense” over the life of the 2011 notes. For further information

regarding the interest rate swaps, refer to Note 14, “Derivatives.”

(c) At December 31, 2008, the Company held an interest rate swap related to the 5.930% notes due 2016 (“2016 Notes”) with an aggregate notional amount of

$110 million. The carrying value of the 2016 Notes has been adjusted for the impact of these hedges. For further information regarding the interest rate swap, refer to

Note 14, “Derivatives.”

(d) The fair value of commercial paper approximates its carrying value due to the short-term nature of the obligations. The fair value of the term loan approximates its

carrying value as it is a variable rate loan and Western Union credit spreads did not move significantly between the date of the borrowing (December 5, 2008) and

December 31, 2008. The fair value of the fixed rate notes is determined by obtaining quotes from multiple, independent banks.

Exclusive of discounts and the fair value of the interest

rate swaps, maturities of borrowings as of December 31,

2008 are $582.9 million in 2009, $1.0 billion in 2011 and

$1.5 billion thereafter. There are no contractual maturities

on borrowings during 2010 and 2012.

The Company’s obligations with respect to its outstand-

ing borrowings, as described below, rank equally.

Commercial Paper Program

On November 3, 2006, the Company established a com-

mercial paper program pursuant to which the Company

may issue unsecured commercial paper notes (the

“Commercial Paper Notes”) in an amount not to exceed

$1.5 billion outstanding at any time. The Commercial

Paper Notes may have maturities of up to 397 days from

date of issuance. Interest rates for borrowings are based

on market rates at the time of issuance. The Company’s

commercial paper borrowings at December 31, 2008 and

2007 had weighted-average interest rates of approximately

4.1% and 5.5%, respectively, and weighted-average initial

terms of 27 days and 36 days, respectively.

Revolving Credit Facility

On September 27, 2006, the Company entered into a five-

year unsecured revolving credit facility, which includes a

$1.5 billion revolving credit facility, a $250.0 million letter

of credit sub-facility and a $150.0 million swing line sub-

facility (the “Revolving Credit Facility”). The Revolving

Credit Facility contains certain covenants that, among

other things, limit or restrict the ability of the Company

and other significant subsidiaries to grant certain types

of security interests, incur debt or enter into sale and

leaseback transactions. The Company is also required to

maintain compliance with a consolidated interest cover-

age ratio covenant.

On September 28, 2007, the Company entered into

an amended and restated credit agreement, the primary

purpose of which was to extend the maturity by one year

from its original five-year $1.5 billion facility entered into

in 2006. No other material changes were made in the

amended and restated facility. As of December 31, 2008,

the Company had $1.4 billion available to borrow, which

is net of the Company’s current commercial paper bor-

rowings backed by this revolving credit facility. The revolv-

ing credit facility, which is diversified through a group of

globally recognized banks, is used to provide general

liquidity for the Company and to support the commercial

paper program, which the Company believes enhances

its short-term credit rating.

Interest due under the Revolving Credit Facility is fixed

for the term of each borrowing and is payable according

to the terms of that borrowing. Generally, interest is

calculated using a selected LIBOR rate plus an interest rate

margin of 19 basis points. A facility fee of 6 basis points

on the total facility is also payable quarterly, regardless

of usage. The facility fee percentage is determined based

on the Company’s credit rating assigned by Standard &

Poor’s Ratings Services (“S&P”) and/or Moody’s Investor

Services, Inc. (“Moody’s”). In addition, to the extent the

aggregate outstanding borrowings under the Revolving

Credit Facility exceed 50% of the related aggregate

commitments, a utilization fee of 5 basis points as of

December 31, 2008 based upon such ratings is payable

to the lenders on the aggregate outstanding borrowings.