Western Union 2008 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2008 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

|

|

7171

Notes to Consolidated

Financial Statements

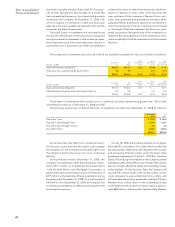

The Company also uses short duration foreign cur-

rency forward contracts, generally with maturities from a

few days up to one month, to offset foreign exchange rate

fluctuations on settlement assets and obligations between

initiation and settlement. In addition, forward contracts,

typically with maturities of less than one year, are utilized

to offset foreign exchange rate fluctuations on certain

foreign currency denominated cash positions. None of

these contracts are designated as hedges pursuant to

SFAS No. 133.

The aggregate United States dollar notional amount of

foreign currency forward contracts held by the Company

as of December 31, 2008 are (in millions):

Contracts not designated as hedges:

Euro $276.2

British pound $34.6

Other $26.6

Contracts designated as hedges:

Euro $556.3

British pound $106.8

Canadian dollar $101.3

Other $75.2

Interest Rate Hedging

The Company utilizes interest rate swaps to effectively

change the interest rate payments on a portion of its notes

due 2011 and 2016 from fixed-rate payments to short-term

LIBOR-based variable rate payments in order to manage

its overall exposure to interest rates. The Company des-

ignates these derivatives as fair value hedges utilizing

the short-cut method in SFAS No. 133, which permits an

assumption of no ineffectiveness if certain criteria are met.

The change in fair value of the interest rate swaps is offset

by a change in the balance of the debt being hedged

within the Company’s “Borrowings” in the Consolidated

Balance Sheets and interest expense has been adjusted

to include the effects of payments made and received

under the swaps.

At December 31, 2008 and 2007, the Company held

interest rate swaps in an aggregate notional amount of

$660 million and $75 million, respectively. The notional

amounts outstanding at December 31, 2008 included

interest rate swaps entered into by the Company to reduce

the economic exposure from fluctuations in interest rates

that will impact the return on pretax income the Company

receives under its existing agreement with IPS (Note 7).

During the fourth quarter of 2008, the Company ter-

minated an aggregate notional amount of $195 million

of interest rate swaps. The Company received cash of

$10.7 million on the termination of these swaps, the off-

set of which was recognized in “Borrowings” and will be

reclassified as a reduction to “Interest expense” over the

life of the 2011 notes.

In 2006, the Company executed forward starting inter-

est rate swaps designated as cash flow hedges to fix the

interest rate in connection with an anticipated issuance

of fixed rate debt securities. The Company terminated

the interest rate swaps in conjunction with the November

2006 issuance of the 2011 and 2036 Notes described in

Note 15 by paying cash of approximately $18.6 million

to the counterparties, resulting in ineffectiveness of

$0.6 million, which was immediately recognized in

“Derivative gains/(losses), net” in the Consolidated

Statements of Income. The remaining $18.0 million loss

on the hedges was included in “Accumulated other

comprehensive loss” and is being reclassified as an increase

to “Interest expense” over the life of the related notes.

Balance Sheet

The following table summarizes the fair value of derivatives reported in the Consolidated Balance Sheets as of

December 31, 2008 and 2007 (in millions).

Asset Derivatives Liability Derivatives

Fair Value Fair Value

Balance Sheet Location 2008 2007 Balance Sheet Location 2008 2007

Derivatives—hedges:

Interest rate fair value hedges Otherassets $ 48.9 $3.6 Otherliabilities $ — $ —

Foreign currency cash flow hedges Other assets 65.0 1.6 Other liabilities 6.7 34.7

Total $113.9 $5.2 $ 6.7 $34.7

Derivatives—undesignated:

Foreign currency Other assets $ 2.9 $2.9 Other liabilities $ 4.1 $ 2.5

Total $ 2.9 $2.9 $ 4.1 $ 2.5

Total derivatives $116.8 $8.1 $10.8 $37.2

The following table summarizes the fair value of derivatives held at December31, 2008 and their expected maturi-

ties (in millions):

Total 2009 2010 2011 2012 2013 Thereafter

Foreign currency hedges—cash flow $ 58.3 $40.5 $17.8 $ — $ — $ — $ —

Foreign currency hedges—undesignated (1.2) (1.2) — — — — —

Interest rate hedges—fair value 48.9 16.0 15.2 10.6 1.8 1.5 3.8

Total $106.0 $55.3 $33.0 $10.6 $1.8 $1.5 $3.8