Western Union 2007 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2007 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

40

WESTERN UNION 2007 Annual Report

DESCRIPTION

Capitalized Costs

We capitalize certain initial payments for new

and renewed agent contracts.

These capitalized costs are classifi ed in

our consolidated balance sheets as “other

intangible assets”. We evaluate such other

intangible assets for impairment annually and

whenever events or changes in circumstances

indicate the carrying value of such assets may

not be recoverable. In such reviews, estimated

undiscounted cash fl ows associated with these

as sets are compared with their carrying

amounts to determine if a write-down to fair

value (normally measured by the present value

technique) is required.

Goodwill Impairment Testing

We evaluate goodwill for impairment annually

and whenever events or changes in circum-

stances indicate the carrying value of the

goodwill may not be recoverable. Goodwill

impair ment is determined using a two-step

process. The fi rst step is to identify if a potential

impairment exists by comparing the fair value

of each reporting unit to its carrying amount.

If the fair value of a reporting unit exceeds its

carrying amount, goodwill of that reporting

unit is not considered to have a potential impair-

ment and the second step of the impairment

test is not necessary. However, if the carrying

amount of a reporting unit exceeds its fair value,

the second step is performed to determine the

implied fair value of a reporting unit’s goodwill,

by comparing the reporting unit’s fair value to

the allocated fair values of all assets and liabili-

ties, including any unrecognized intangible

assets, as if the reporting unit had been acquired

in a business combination. If the implied fair

value of goodwill exceeds its carrying amount,

goodwill is not considered impaired. However,

if the carrying amount of goodwill exceeds its

implied fair value, an impairment is recognized

in an amount equal to that excess.

We also have subsidiaries within our con-

solidated group with stand-alone reporting

requirements. Goodwill testing with respect to

these subsidiaries is tested for impairment at

the subsidiary level using that subsidiary’s

reporting units, which differ from our consoli-

dated reporting units. Accordingly, if a goodwill

impairment loss were recognized at the sub-

sidiary level, a resulting impairment loss would

be recorded at the consolidated level only to

the extent that the consolidated reporting unit,

where the subsidiary resides, experienced an

impairment loss.

JUDGMENTS AND UNCERTAINTIES

The capitalization of initial payments for new

and renewed contracts is subject to strict

accounting policy criteria and requires manage-

ment judgment as to the appropriate time to

initiate capitalization. Our accounting policy is

to limit the amount of capitalized costs for a

given contract to the lesser of the estimated

future cash fl ows from the contract or the ter-

mination fees we would receive in the event of

early termination of the contract.

We calculate the fair value of each reporting

unit through discounted cash fl ow analyses

which require us to make estimates and

assumptions including, among other items,

revenue growth rates, operating margins, and

capital expenditures based on our budgets

and business plans which take into account

expected, regulatory, marketplace and other

economic factors.

There are also judgments around the deter-

mination of our reporting units. Reporting units

are defi ned as an operating segment or one

level below an operating segment, referred to

as a component.

EFFECT IF ACTUAL RESULTS

DIFFER FROM ASSUMPTIONS

Disruptions to an agent relationship, signifi cant

declines in cash fl ows or transaction volumes

associated with an agent contract, or other

issues signifi cantly impacting an agent’s busi-

ness could require us to evaluate the recover-

ability of our capitalized initial payments for

new and renewed agent contracts prior to the

annual assessment.

These types of events and the resulting

analyses could result in impairment charges in

the future which could signifi cantly impact our

reported earnings in the periods such charges

occur. We did not record any impairment

charges related to other intangible assets

during the years ended December 31, 2007,

2006 or 2005.

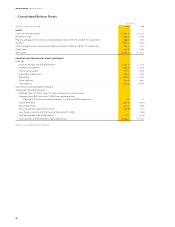

The net carrying value of our capitalized

contract costs at December 31, 2007 was $193.1

million.

We could be required to evaluate the recover-

ability of goodwill prior to the annual assess-

ment if we experience disruptions to the

business, unexpected signifi cant declines in

operating results, a divestiture of a signifi cant

component of our business, signifi cant declines

in market capitalization or other triggering

events. In addition, as our business or the way

we manage our business changes, our reporting

units may also change. These types of events

and the resulting analyses could result in good-

will impairment charges in the future which

could materially impact our reported earnings

in the periods such charges occur. The carrying

value of goodwill as of December 31, 2007 was

$1,639.5 million which represented approxi-

mately 28% of our consolidated assets.

During 2005, we recognized an impairment

charge of $8.7 million relating to our 51% own-

ership interest in EPOSS Limited (“EPOSS”) due

to a change in strategic direction. This impair-

ment was recognized at both the subsidiary

reporting unit and consolidated reporting unit

level as EPOSS was its own reporting unit for

stand-alone and consolidated fi nancial report-

ing. We have not recorded any other goodwill

impairments during the three years ended

December 31, 2007.