Vodafone 2001 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2001 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

30

Vodafone Group Plc

Annual Report & Accounts

for the year ended

31 March 2001

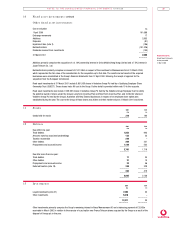

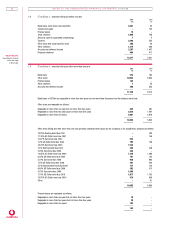

STATEMENT OF ACCOUNTING POLICIES continued

Goodwill

Goodwill is calculated as the surplus of cost over fair value attributed to the net assets (excluding goodwill) of subsidiary, joint venture or

associated undertakings acquired.

For acquisitions made after the financial year ended 31 March 1998, goodwill is capitalised and held as a foreign currency denominated asset,

where applicable. Goodwill is amortised on a straight line basis over its estimated useful economic life. For acquired network businesses, whose

operations are governed by fixed term licences, the amortisation period is determined primarily by reference to the unexpired licence period and

the conditions for licence renewal. For other acquisitions, including customer bases, the amortisation period for goodwill is typically between

5 and 10 years.

For acquisitions made before the adoption of Financial Reporting Standard 10, “Goodwill and Intangible Assets”, on 1 April 1998, goodwill was

written off directly to reserves. Goodwill written off directly to reserves is reinstated in the profit and loss account when the related business

is sold.

Oth er in tangible fixed assets

Purchased intangible fixed assets, including licence fees, are capitalised at cost.

Network licence costs are amortised over the periods of the licences. Amortisation is charged from commencement of service of the network.

The annual charge is calculated in proportion to the expected usage of the network during the start up period and on a straight line basis

thereafter.

Tan gible fixed assets

Tangible fixed assets are stated at cost less accumulated depreciation.

Depreciation is not provided on freehold land. The cost of other tangible fixed assets is written off, from the time they are brought into use, by

equal instalments over their expected useful lives as follows:

Freehold buildings 25 – 50 years

Leasehold premises the term of the lease

Motor vehicles 4 years

Computers and software 3 – 5 years

Equipment, fixtures and fittings 5 – 10 years

The cost of tangible fixed assets include directly attributable incremental costs incurred in their acquisition and installation.

In ve stm en ts

The consolidated financial statements include investments in associated undertakings using the equity method of accounting. An associated

undertaking is an entity in which the Group has a participating interest and, in the opinion of the directors, can exercise significant influence

in its management. The profit and loss account includes the Group’s share of the operating profit or loss, exceptional items, interest income or

expense and attributable taxation of those entities. The balance sheet shows the Group’s share of the net assets or liabilities of those entities,

together with loans advanced and attributed goodwill.

The consolidated financial statements include investments in joint ventures using the gross equity method of accounting. A joint venture is an

entity in which the Group has a long term interest and exercises joint control. Under the gross equity method, a form of the equity method of

accounting, the Group’s share of the aggregate gross assets and liabilities underlying the investment in the joint venture is included in the

balance sheet and the Group’s share of the turnover of the joint venture is disclosed in the profit and loss account.

Other investments, held as fixed assets, comprise equity shareholdings and other interests. They are stated at cost less provision for any

impairment. Dividend income is recognised upon receipt and interest when receivable.

Stocks

Stocks are valued at the lower of cost and estimated net realisable value.

Deferred taxation

Provision is made for deferred taxation only where there is a reasonable probability that a liability or asset will crystallise in the foreseeable

future.

No provision is made for any tax liability which may arise if undistributed profits of certain international subsidiary undertakings, joint ventures

and associated undertakings are remitted to the UK, except in respect of planned remittances.

Leases

Rental costs under operating leases are charged to the profit and loss account in equal annual amounts over the periods of the leases.

Assets acquired under finance leases, which transfer substantially all the rights and obligations of ownership, are accounted for as though

purchased outright. The fair value of the asset at the inception of the lease is included in tangible fixed assets and the capital element of the

leasing commitment included in creditors. Finance charges are calculated on an actuarial basis and are allocated over each lease to produce a

constant rate of charge on the outstanding balance.

Lease obligations which are satisfied by cash and other assets deposited with third parties are set-off against those assets in the Group’s

balance sheet.