US Cellular 2012 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2012 US Cellular annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

United States Cellular Corporation

Notes to the Consolidated Financial Statements (Continued)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND RECENT ACCOUNTING

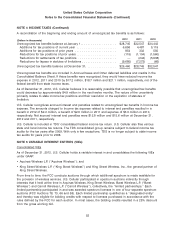

PRONOUNCEMENTS (Continued)

financial information is not readily available, U.S. Cellular records its equity in the earnings of the entity

on a one quarter lag basis.

Property, Plant and Equipment

U.S. Cellular’s Property, plant and equipment is stated at the original cost of construction or purchase

including capitalized costs of certain taxes, payroll-related expenses, interest and estimated costs to

remove the assets.

Expenditures that enhance the productive capacity of assets in service or extend their useful lives are

capitalized and depreciated. Expenditures for maintenance and repairs of assets in service are charged

to System operations expense or Selling, general and administrative expense, as applicable. Retirements

and disposals of assets are recorded by removing the original cost of the asset (along with the related

accumulated depreciation) from plant in service and charging it, together with removal cost less any

salvage realized, to (Gain) loss on asset disposals and exchanges, net.

Costs of developing new information systems are capitalized and amortized over their expected

economic useful lives.

Depreciation

Depreciation is provided using the straight-line method over the estimated useful life of the assets.

U.S. Cellular depreciates leasehold improvement assets associated with leased properties over periods

ranging from one to thirty years; such periods approximate the shorter of the assets’ economic lives or

the specific lease terms.

Useful lives of specific assets are reviewed throughout the year to determine if changes in technology or

other business changes would warrant accelerating the depreciation of those specific assets. Due to the

Divestiture Transaction more fully described in Note 7—Acquisitions, Divestitures and Exchanges, U.S.

Cellular changed the useful lives of certain assets in 2012. There were no material changes to useful

lives of property, plant and equipment in 2011 or 2010.

Impairment of Long-lived Assets

U.S. Cellular reviews long-lived assets for impairment whenever events or changes in circumstances

indicate that the assets might be impaired. The impairment test for tangible long-lived assets is a

two-step process. The first step compares the carrying value of the asset (or asset group) with the

estimated undiscounted cash flows over the remaining asset (or asset group) life. If the carrying value of

the asset (or asset group) is greater than the undiscounted cash flows, the second step of the test is

performed to measure the amount of impairment loss. The second step compares the carrying value of

the asset to its estimated fair value. If the carrying value exceeds the estimated fair value (less cost to

sell), an impairment loss is recognized for the difference.

Quoted market prices in active markets are the best evidence of fair value of a tangible long-lived asset

and are used when available. If quoted market prices are not available, the estimate of fair value is

based on the best information available, including prices for similar assets and the use of other valuation

techniques. A present value analysis of cash flow scenarios is often the best available valuation

technique. The use of this technique involves assumptions by management about factors that are

uncertain including future cash flows, the appropriate discount rate and other inputs. Different

assumptions for these inputs could create materially different results.

43