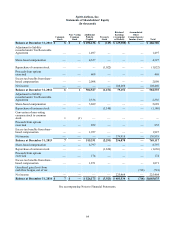

Spirit Airlines 2014 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2014 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

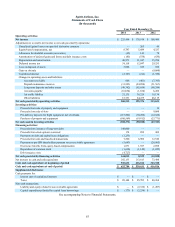

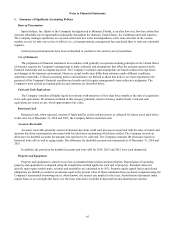

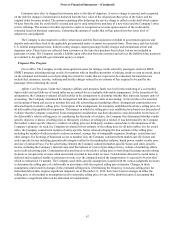

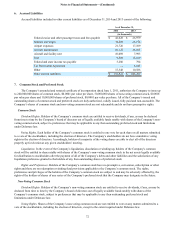

Notes to Financial Statements—(Continued)

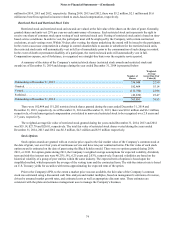

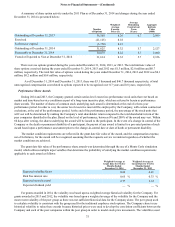

67

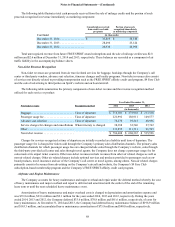

Customers may elect to change their itinerary prior to the date of departure. A service charge is assessed and recognized

on the date the change is initiated and is deducted from the face value of the original purchase price of the ticket, and the

original ticket becomes invalid. The amount remaining after deducting the service charge is called a credit shell which expires

60 days from the date the credit shell is created and can be used towards the purchase of a new ticket and the Company’s other

service offerings. The amount of credits expected to expire is recognized as revenue upon issuance of the credit and is

estimated based on historical experience. Estimating the amount of credits that will go unused involves some level of

subjectivity and judgment.

The Company is also required to collect certain taxes and fees from customers on behalf of government agencies and

airports and remit these back to the applicable governmental entity or airport on a periodic basis. These taxes and fees include

U.S. federal transportation taxes, federal security charges, airport passenger facility charges and international arrival and

departure taxes. These items are collected from customers at the time they purchase their tickets, but are not included in

passenger revenue. The Company records a liability upon collection from the customer and relieves the liability when payments

are remitted to the applicable governmental agency or airport.

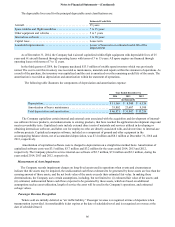

Frequent Flier Program

Flown Miles. The Company records unrecognized revenue for mileage credits earned by passengers under its FREE

SPIRIT program, including mileage credits for members with an insufficient number of mileage credits to earn an award, based

on the estimated incremental cost of providing free travel for credits that are expected to be redeemed. Incremental costs

include fuel, insurance, security, ticketing and facility charges reduced by an estimate of fees required to be paid by the

passenger when redeeming the award.

Affinity Card Program. Under the Company's affinity card program, funds received for the marketing of a co-branded

Spirit credit card and delivery of award miles are accounted for as a mulitple-deliverable arrangement. At the inception of the

arrangement, the Company evaluated all deliverables in the arrangement to determine whether they represent separate units of

accounting. The Company determined the arrangement had three separate units of accounting: (i) travel miles to be awarded,

(ii) licensing of brand and access to member lists and (iii) advertising and marketing efforts. Arrangement consideration was

allocated based on relative selling price. At inception of the arrangement, the Company established the relative selling price for

all deliverables that qualified for separation. The manner in which the selling price was established was based on a hierarchy of

evidence that the Company considered. Total arrangement consideration was then allocated to each deliverable on the basis of

the deliverable’s relative selling price. In considering the hierarchy of evidence, the Company first determined whether vendor

specific objective evidence of selling price or third-party evidence of selling price existed. It was determined by the Company

that neither vendor specific objective evidence of selling price nor third-party evidence existed due to the uniqueness of the

Company’s program. As such, the Company developed its best estimate of the selling price for all deliverables. For the award

miles, the Company considered a number of entity-specific factors when developing the best estimate of the selling price

including the number of miles needed to redeem an award, average fare of comparable segments, breakage, restrictions and

other charges. For licensing of brand and access to member lists, the Company considered both market-specific factors and

entity-specific factors including general profit margins realized in the marketplace/industry, brand power, market royalty rates

and size of customer base. For the advertising element, the Company considered market-specific factors and entity-specific

factors, including the Company’s internal costs (and fluctuations of costs) of providing services, volume of marketing efforts

and overall advertising plan. Consideration allocated based on the relative selling price to both brand licensing and advertising

elements is recognized as revenue when earned and recorded in non-ticket revenue. Consideration allocated to award miles is

deferred and recognized ratably as passenger revenue over the estimated period the transportation is expected to be provided

which is estimated at 14 months. The Company used entity-specific assumptions coupled with the various judgments necessary

to determine the selling price of a deliverable in accordance with the required selling price hierarchy. Changes in these

assumptions could result in changes in the estimated selling prices. Determining the frequency to reassess selling price for

individual deliverables requires significant judgment. As of December 31, 2014, there have been no changes in either the

selling price or the method or assumptions used to determine selling price for any of the identified units of accounting that

would have a significant effect on the allocation of consideration.