Spirit Airlines 2014 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2014 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

38

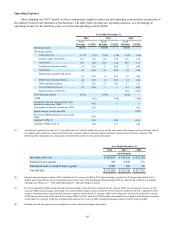

and operational overhead expenses. No individual item included in this category represented more than 5% of our total

operating expenses.

Special Charges (Credits). Special charges (credits) include termination costs, secondary offering costs and the gain on

the sale of take-off and landing slots.

In 2012, we sold four permanent air carrier slots at Ronald Reagan National Airport (DCA) to another airline for $9.1

million. We recognized the $9.1 million gain within special charges (credits) in the third quarter of 2012, the period in which

the FAA operating restriction lapsed and written confirmation of the slot transfer was received by the buyer from the FAA.

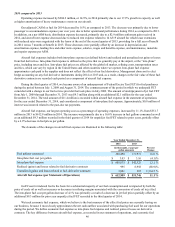

Other Expense (Income)

Interest Expense. Interest expense in 2012 and 2013 primarily related to interest on the TRA. For 2014, interest expense

primarily represented interest related to the financing of purchased aircraft, interest related to the underpayment of prior year jet

fuel FET and interest charged under the TRA.

Capitalized Interest. Capitalized interest represents interest cost incurred during the acquisition period of an aircraft

which theoretically could have been avoided had we not made PDPs for that aircraft. These amounts are capitalized as part of

the cost of the aircraft upon delivery. Capitalization of interest ceases when the asset is ready for service. Capitalized interest

for 2012 and 2013 primarily related to interest incurred in connection with payments owed under the TRA. For 2014,

capitalized interest primarily related to interest incurred on long-term debt, underpayment of prior year jet fuel FET and interest

charged under the TRA.

Other Expense. For 2014, other expense included a charitable contribution of $1.0 million that is specifically creditable

against current income tax in the State of Florida, as allowed under state law.

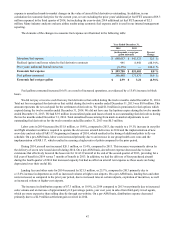

Income Taxes

We account for income taxes using the liability method. We record a valuation allowance to reduce the deferred tax assets

reported if, based on the weight of the evidence, it is more likely than not that some portion or all of the deferred tax assets will

not be realized. Deferred taxes are recorded based on differences between the financial statement basis and tax basis of assets

and liabilities and available tax loss and credit carryforwards. In assessing the realizability of the deferred tax assets, we

consider whether it is more likely than not that some or all of the deferred tax assets will be realized. In evaluating the ability to

utilize our deferred tax assets, we consider all available evidence, both positive and negative, in determining future taxable

income on a jurisdiction by jurisdiction basis.

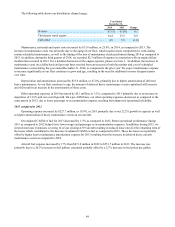

In connection with our IPO in 2011, we entered into the TRA and thereby distributed immediately prior to the completion

of the IPO to the holders of common stock as of such time, or the Pre-IPO Stockholders, the right to receive an amount equal to

90% of the cash savings in federal income tax realized by it by virtue of the use of the federal net operating loss, deferred

interest deductions and alternative minimum tax credits held by us as of March 31, 2011, which was defined as the Pre-IPO

NOL. Cash tax savings were generally computed by comparing actual federal income tax liability to the amount of such taxes

that we would have been required to pay had such Pre-IPO NOLs (as defined in the TRA) not been available. Upon

consummation of the IPO and execution of the TRA, we recorded a liability with an offsetting reduction to additional paid in

capital. The amount and timing of payments under the TRA depended upon a number of factors, including, but not limited to,

the amount and timing of taxable income generated in future periods and any limitations that may have been imposed on our

ability to use the Pre-IPO NOLs. The term of the TRA was to continue until the first to occur (a) the full payment of all

amounts required under the agreement with respect to utilization or expiration of all of the Pre-IPO NOLs, (b) the end of the

taxable year including the tenth anniversary of the IPO or (c) a change in control of the Company.

In accordance with the TRA, we were required to submit a Tax Benefit Schedule showing the proposed TRA payout

amount to the Stockholder Representatives within 45 calendar days of filing our tax return. Stockholder Representatives were

defined as Indigo Pacific Partners, LLC and OCM FIE, LLC, representing the two largest ownership interest of pre-IPO shares.

The Tax Benefit Schedule was to become final and binding on all parties unless a Stockholder Representative, within 45

calendar days after receiving such schedule, provided us with notice of a material objection to such schedule. If the parties, for

any reason, were unable to successfully resolve the issues raised in any notice within 30 calendar days of receipt of such notice,

we and the Stockholder Representatives had the right to employ the reconciliation procedures as set forth in the TRA. If the Tax

Benefit Schedule was accepted, we then had five days after acceptance to make payments to the Pre-IPO stockholders.

Pursuant to the TRA's reconciliation procedures, any disputes that could not be settled amicably, were to be settled by

arbitration conducted by a single arbitrator jointly selected by both parties.