Spirit Airlines 2014 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2014 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

42

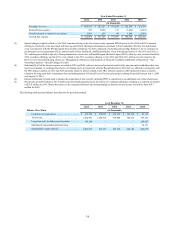

security, ticketing and facility charges reduced by an estimate of amounts required to be paid by the passenger when redeeming

the award.

Under our affinity card program, funds received for the marketing of a co-branded Spirit credit card and delivery of

award miles are accounted for as a mulitple-deliverable arrangement. At the inception of the arrangement, we evaluated all

deliverables in the arrangement to determine whether they represent separate units of accounting. We determined the

arrangement had three separate units of accounting: (i) travel miles to be awarded, (ii) licensing of brand and access to member

lists and (iii) advertising and marketing efforts. At inception of the arrangement, we established the relative selling price for all

deliverables that qualified for separation, as arrangement consideration should be allocated based on relative selling price. The

manner in which the selling price was established was based on the applicable hierarchy of evidence. Total arrangement

consideration was then allocated to each deliverable on the basis of the deliverable's relative selling price. In considering the

hierarchy of evidence, we first determined whether vendor-specific objective evidence of selling price or third-party evidence

of selling price existed. We determined that neither vendor-specific objective evidence of selling price nor third-party evidence

existed due to the uniqueness of our program. As such, we developed our best estimate of the selling price for all deliverables.

For the selling price of travel, we considered a number of entity-specific factors including the number of miles needed to

redeem an award, average fare of comparable segments, breakage, restrictions and other charges. For licensing of brand and

access to member lists, we considered both market-specific factors and entity-specific factors, including general profit margins

realized in the marketplace/industry, brand power, market royalty rates and size of customer base. For the advertising and

marketing element, we considered market-specific factors and entity-specific factors including, our internal costs (and

fluctuations of costs) of providing services, volume of marketing efforts and overall advertising plan. Consideration allocated

based on the relative selling price to both brand licensing and advertising elements is recognized as revenue when earned and

recorded in non-ticket revenue. Consideration allocated to award miles is deferred and recognized ratably as passenger revenue

over the estimated period the transportation is expected to be provided which is currently estimated at 14 months. We used

entity-specific assumptions coupled with the various judgments necessary to determine the selling price of a deliverable in

accordance with the required selling price hierarchy. Changes in these assumptions could result in changes in the estimated

selling prices. Determining the frequency to reassess selling price for individual deliverables requires significant judgment. For

additional information, please see “Notes to Financial Statements—1. Summary of Significant Accounting Policies—Frequent

Flier Program”.

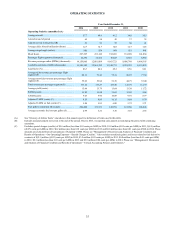

Aircraft Maintenance, Materials, Repair Costs and Related Heavy Maintenance Amortization. We account for heavy

maintenance under the deferral method. Under the deferral method the cost of heavy maintenance is capitalized and amortized

as a component of depreciation and amortization expense until the earlier of the next estimated heavy maintenance event or the

aircraft's return at the end of the lease term. Amortization of engine and aircraft overhaul costs was $35.8 million, $23.6 million

and $9.1 million for the years ended December 31, 2014, 2013 and 2012, respectively. If heavy maintenance costs were

amortized within maintenance, material and repairs expense in the statement of operations, our maintenance, material and

repairs expense would have been $109.8 million, $83.8 million and $58.6 million for the years ended December 31, 2014, 2013

and 2012, respectively. During the years ended December 31, 2014, 2013 and 2012, we capitalized $33.6 million, $70.8 million

and $61.6 million of costs for heavy maintenance, respectively. The timing of the next heavy maintenance event is estimated

based on assumptions including estimated usage, FAA-mandated maintenance intervals and average removal times as

suggested by the manufacturer. These assumptions may change based on changes in our utilization of our aircraft, changes in

government regulations and suggested manufacturer maintenance intervals. In addition, these assumptions can be affected by

unplanned incidents that could damage an airframe, engine or major component to a level that would require a heavy

maintenance event prior to a scheduled maintenance event. To the extent our planned usage increases, the estimated life would

decrease before the next maintenance event, resulting in additional expense over a shorter period. Heavy maintenance events

include 6-year and 12-year airframe checks, engine overhauls, LLP replacement and overhauls to major components. Certain

maintenance functions are outsourced under contracts that require payment based on a performance measure such as flight

hours. Costs incurred for maintenance and repair under flight hour maintenance contracts, where labor and materials price risks

have been transferred to the service provider, are accrued based on contractual payment terms. Routine cost for maintaining the

airframes and engines and line maintenance are charged to maintenance, materials and repairs expense as performed.

Maintenance Reserves. Some of our master lease agreements provide that we pay maintenance reserves to aircraft lessors

to be held as collateral in advance of our performance of major maintenance activities. These lease agreements provide that

maintenance reserves are reimbursable to us upon completion of the maintenance event in an amount equal to either (1) the

amount of the maintenance reserve held by the lessor associated with the specific maintenance event or (2) the qualifying costs

related to the specific maintenance event. Substantially all of these maintenance reserve payments are calculated based on a

utilization measure, such as flight hours or cycles and are used solely to collateralize the lessor for maintenance time run off the

aircraft until the completion of the maintenance of the aircraft.

At lease inception and at each balance sheet date, we assess whether the maintenance reserve payments required by the

master lease agreements are substantively and contractually related to the maintenance of the leased asset. Maintenance reserve