Spirit Airlines 2014 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2014 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

43

payments that are substantively and contractually related to the maintenance of the leased asset are accounted for as

maintenance deposits. Maintenance deposits expected to be recovered from lessors are reflected as prepaid maintenance

deposits in the accompanying balance sheets. When it is not probable we will recover amounts currently on deposit with a

lessor, such amounts are expensed as supplemental rent. Because we are required to pay maintenance reserves for our operating

leased aircraft, and we choose to apply the deferral method for maintenance accounting, management expects that the final

heavy maintenance events will be amortized over the remaining lease term rather than over the next estimated heavy

maintenance event. As a result, our maintenance costs in the last few years of leases could be significantly in excess of the costs

in earlier periods. In addition, these late periods could include additional costs from unrecoverable maintenance reserve

payments required in the late years of the lease. We expensed $1.6 million, $1.9 million and $2.0 million of paid maintenance

reserves as supplemental rent during 2014, 2013 and 2012, respectively.

As of December 31, 2014 and 2013, we had prepaid maintenance deposits of $250.0 million and $220.7 million,

respectively, on our balance sheets. We have concluded that these prepaid maintenance deposits are probable of recovery

primarily due to the rate differential between the maintenance reserve payments and the expected cost for the related next

maintenance event that the reserves serve to collateralize.

These master lease agreements also provide that most maintenance reserves held by the lessor at the expiration of the

lease are nonrefundable to us and will be retained by the lessor. Consequently, we have determined that any usage-based

maintenance reserve payments after the last major maintenance event are not substantively related to the maintenance of the

leased asset and therefore are accounted for as contingent rent. We accrue contingent rent beginning when it becomes probable

and reasonably estimable we will incur such nonrefundable maintenance reserve payments. We make certain assumptions at the

inception of the lease and at each balance sheet date to determine the recoverability of maintenance deposits. These

assumptions are based on various factors such as the estimated time between the maintenance events, the cost of future

maintenance events and the number of flight hours the aircraft is estimated to be utilized before it is returned to the lessor.

Maintenance reserves held by lessors that are refundable to us at the expiration of the lease are accounted for as prepaid

maintenance deposits on the balance sheet when they are paid.

Leased Aircraft Return Costs. Our aircraft lease agreements often contain provisions that require us to return aircraft

airframes and engines to the lessor in a certain maintenance condition or pay an amount to the lessor based on the airframe and

engine's actual return condition. Lease return costs will be recognized as expense beginning when it is probable that such costs

will be incurred and they can be estimated. Incurrence of lease return costs becomes probable and the amount of those costs can

typically be estimated near the end of the lease term (that is, after the aircraft has completed its last maintenance cycle prior to

being returned). We will evaluate all lease return conditions after the second to last maintenance event as it relates to the

respective component or airframe from the lease return. If at this point it becomes both probable and estimable that a return

cost will be incurred, we will accrue the cost on a straight-line basis as contingent rent through the remaining lease term. Return

costs are recorded as a component of supplemental rent.

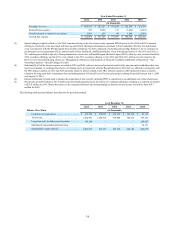

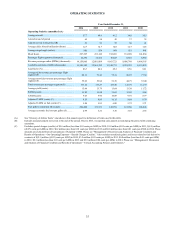

Results of Operations

In 2014, we generated operating revenues of $1,931.6 million and operating income of $355.3 million resulting in an

18.4% operating margin and net earnings of $225.5 million. In 2013, we generated operating revenues of $1,654.4 million and

operating income of $282.3 million resulting in a 17.1% operating margin and net earnings of $176.9 million. Operating

revenues increased year over year mainly as a result of an 18.0% increase in traffic, as compared to prior year. The increase in

operating income in 2014 over 2013 of $73.0 million, is mainly due to a 16.8% increase in revenue partially offset by increased

fuel and other expenses resulting from an increase in operations. Fuel costs increased by $61.2 million during 2014 compared

to 2013, primarily driven by a 16.6% increase in consumption offset by a lower fuel cost per gallon year over year. Operating

expenses increased primarily due to our growth in capacity resulting from the addition of eleven aircraft to our fleet and our

route network expansion.

As of December 31, 2014, our cash and cash equivalents grew to $632.8 million, an increase of $102.2 million compared

to the prior year, mainly driven by cash from our operating activities offset by cash used to fund PDPs and capital expenditures.