Spirit Airlines 2014 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2014 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

53

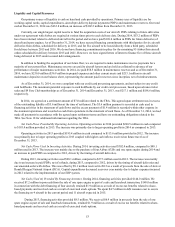

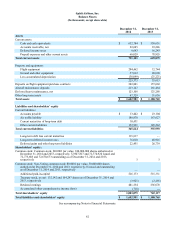

Liquidity and Capital Resources

Our primary source of liquidity is cash on hand and cash provided by operations. Primary uses of liquidity are for

working capital needs, capital expenditures, aircraft pre-delivery deposit payments (PDPs) and maintenance reserves. Our total

cash at December 31, 2014 was $632.8 million, an increase of $102.2 million from December 31, 2013.

Currently, our single largest capital need is to fund the acquisition costs of our aircraft. PDPs relating to future deliveries

under our agreement with Airbus are required at various times prior to each delivery date. During 2014, $53.2 million of PDPs

have been returned related to delivered aircraft in the period and we have paid $169.0 million in PDPs for future deliveries of

aircraft and spare engines. As of December 31, 2014, we have secured financing commitments with third parties for six aircraft

deliveries from Airbus, scheduled for delivery in 2015, and for five aircraft to be leased directly from a third party, scheduled

for delivery between 2015 and 2016. We do not have financing commitments in place for the remaining 95 Airbus firm aircraft

orders scheduled for delivery between 2015 and 2021. However, we have signed letters of intent to finance five of these aircraft

being delivered in 2015 under secured debt arrangements.

In addition to funding the acquisition of our future fleet, we are required to make maintenance reserve payments for a

majority of our current fleet. Maintenance reserves are paid to aircraft lessors and are held as collateral in advance of our

performance of major maintenance activities. In 2014, we paid $58.5 million in maintenance reserves and as of December 31,

2014, we have $250.0 million ($36.9 million in prepaid expenses and other current assets and $213.1 million in aircraft

maintenance deposits) on our balance sheet, representing the amount paid in reserves since inception, net of reimbursements.

As of December 31, 2014, we were compliant with our credit card processing agreements, and not subject to any credit

card holdbacks. The maximum potential exposure to cash holdbacks by our credit card processors, based upon advance ticket

sales and $9 Fare Club memberships as of December 31, 2014 and December 31, 2013, was $217.1 million and $188.6 million,

respectively.

In 2014, we agreed on a settlement amount of $7.0 million related to the TRA. This agreed upon settlement was in excess

of the outstanding liability of $5.6 million at the time of settlement. The $5.6 million payment is recorded as cash used in

financing activities in the statement of cash flows and the excess payment of $1.4 million is recorded within other expense in

the statement operations and recorded as cash from operations in the statement of cash flows. As of December 31, 2014, we had

made all payments in accordance with the agreed upon settlement terms and have no outstanding obligations related to the

TRA. See Note 18 for additional information regarding the TRA.

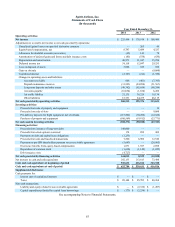

Net Cash Flows Provided By Operating Activities. Operating activities in 2014 provided $260.5 million in cash compared

to $195.4 million provided in 2013. The increase was primarily due to larger operating profits in 2014 as compared to 2013.

Operating activities in 2013 provided $195.4 million in cash compared to $113.6 million provided in 2012. The increase

was primarily due to larger operating profits in 2013 coupled with higher cash inflows received on future travel as of

December 31, 2013.

Net Cash Flows Used In Investing Activities. During 2014, investing activities used $302.4 million, compared to $90.1

million used in 2013. The increase was mainly due to the purchase of four Airbus A320s and one spare engine during 2014 and

an increase in paid PDPs as compared to 2013, driven by the timing of aircraft deliveries.

During 2013, investing activities used $90.1 million, compared to $27.3 million used in 2012. The increase was mainly

due to an increase in paid PDPs, net of refunds, during 2013, compared to 2012, driven by the timing of aircraft deliveries and

our amended order with Airbus. This was offset by $9.1 million received in 2012 as a result of proceeds from the sale of slots at

Ronald Reagan National Airport (DCA). Capital expenditures decreased year over year mainly due to higher expenses incurred

in 2012 related to the implementation of our ERP system.

Net Cash (Used in) Provided By Financing Activities. During 2014, financing activities provided $144.0 million. We

received $7.2 million in proceeds from the sale of one spare engine as part of a sale and leaseback transaction, $148.0 million

in connection with the debt financing of four aircraft, retained $1.9 million as a result of excess tax benefits related to share-

based payments and received cash as a result of exercised stock options. We spent $4.7 million in debt issuance cost to secure

the financing on 4 aircraft in the current period and 11 aircraft expected in 2015.

During 2013, financing activities provided $8.5 million. We received $6.9 million in proceeds from the sale of one

spare engine as part of sale and leaseback transactions, retained $1.9 million as a result of excess tax benefits related to share-

based payments and received cash as a result of exercised stock options.