Shaw 2014 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2014 Shaw annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

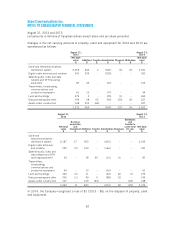

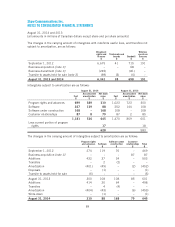

Shaw Communications Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

August 31, 2014 and 2013

[all amounts in millions of Canadian dollars except share and per share amounts]

Adoption of recent accounting pronouncements

The adoption of the following standards and amendments effective September 1, 2013 had no

impact on the Company’s consolidated financial statements other than additional disclosure

requirements.

ŠIFRS 10 Consolidated Financial Statements replaces previous consolidation guidance and

outlines a single consolidation model that identifies control as the basis for consolidation

of all types of entities.

ŠIFRS 11 Joint Arrangements replaces IAS 31 Interests in Joint Ventures and SIC 13

Jointly Controlled Entities – Non-Monetary Contributions by Venturers. The new standard

classifies joint arrangements as either joint operations or joint ventures.

ŠIFRS 12 Disclosure of Interests in Other Entities sets out required disclosures on

application of IFRS 10, IFRS 11 and IAS 28 (amended 2011).

ŠIAS 27 Separate Financial Statements was amended in 2011 for the issuance of IFRS 10

and retains the same guidance for separate financial statements.

ŠIAS 28 Investments in Associates was amended in 2011 for changes based on issuance

of IFRS 10 and IFRS 11 and provides guidance on accounting for joint ventures, as

defined by IFRS 11, using the equity method.

ŠIFRS 13 Fair Value Measurement defines fair value, provides guidance on its

determination and introduces consistent requirements for disclosure of fair value

measurements.

The Company has elected to early adopt the amendments to IAS 36 Impairment of Assets for

the year ended August 31, 2014. The amendments limit the requirement to disclose the

recoverable amount to assets (including goodwill) for which an impairment loss was recognized

or reversed in the period, instead of the recoverable amount for each CGU to which significant

goodwill or indefinite-life intangible assets have been allocated. Under the amendments,

recoverable amount is required to be disclosed only when an impairment loss has been

recognized or reversed.

Standards, interpretations and amendments to standards issued but not yet effect

The Company has not yet adopted certain standards and interpretations that have been issued

but are not yet effective. The following pronouncements are being assessed to determine the

impact on the Company’s results and financial position.

ŠIFRIC 21 Levies provides guidance on when to recognize a financial liability imposed by a

government, if the levy is accounted for in accordance with IAS 37 Provisions, Contingent

Liabilities and Contingent Assets, or where the timing and amount of the levy is certain.

This interpretation is effective for the annual period commencing September 1, 2014 and

is not expected to have an impact on the Company’s financial statements.

ŠClarification of Acceptable Methods of Depreciation and Amortization (Amendments to

IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets) prohibits revenue

from being used as a basis to depreciate property, plant and equipment and significantly

80