Shaw 2014 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2014 Shaw annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

|

|

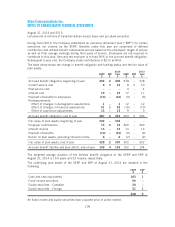

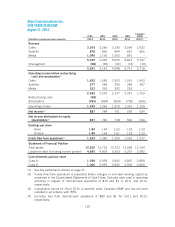

Shaw Communications Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

August 31, 2014 and 2013

[all amounts in millions of Canadian dollars except share and per share amounts]

The tables below show the significant weighted-average assumptions used to measure the

pension obligation and cost for these plans.

Accrued benefit obligation

2014

%

2013

%

Discount rate 4.09 4.84

Rate of compensation increase 3.00 3.50

Benefit cost for the year

2014

%

2013

%

Discount rate 4.84 4.67

Rate of compensation increase 3.50 3.50

The calculation of the accrued benefit obligation is sensitive to the assumptions above. A one

percentage point decrease in the discount rate would have increased the accrued benefit

obligation at August 31, 2014 by $31. A one percentage point increase in the rate of

compensation increase would have increased the accrued benefit obligation by $6.

When calculating the sensitivity of the defined benefit obligation to significant actuarial

assumptions, the present value of the defined benefit obligation has been calculated using the

projected benefit method which is the same method that is applied in calculating the defined

benefit liability recognized in the statement of financial position. The sensitivity analysis

presented above may not be representative of the actual change in the accrued benefit

obligation as it is unlikely that the change in assumptions would occur in isolation of one

another as some assumptions may be correlated.

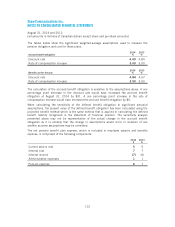

The net pension benefit plan expense, which is included in employee salaries and benefits

expense, is comprised of the following components:

2014

$

2013

$

Current service cost 55

Interest cost 77

Interest income (7) (6)

Administrative expenses 11

Pension expense 67

112