Samsung 2010 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2010 Samsung annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

46 47

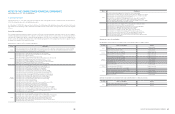

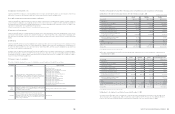

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Capitalized interest is added to the cost of the underlying assets.

The acquisition cost of property, plant and equipment acquired

under a finance lease is determined at the lower of the present

value of the minimum lease payments and the fair market value of

the leased asset at the inception of the lease. Property, plant and

equipment acquired under a finance lease, leasehold improvements

are depreciated over the shorter of the lease term or useful life.

Land is not depreciated. Depreciation on other assets is calculated

using the straight-line method to allocate their cost to their residual

values over their estimated useful lives, as follows:

The assets’ residual values and useful lives are reviewed, and

adjusted if appropriate, at the end of each reporting period.

An asset’s carrying amount is written down immediately to its

recoverable amount if the asset’s carrying amount is greater than its

estimated recoverable amount. Gains and losses on disposals are

determined by comparing the proceeds with the carrying amount

and are recognized within the statement of income.

2.10 Intangible Assets

1) Goodwill

Goodwill represents the excess of the cost of an acquisition over

the fair value of the group’s share of the net identifiable assets

of the acquired subsidiary at the date of acquisition. Goodwill

on acquisitions of subsidiaries is included in intangible assets.

Goodwill is tested annually for impairment and carried at cost less

accumulated impairment losses. Impairment losses on goodwill are

not reversed. Gains and losses on the disposal of an entity include

the carrying amount of goodwill relating to the entity sold.

2) Capitalized development costs

The Company capitalizes certain development costs when outcome

of development plan is for practical enhancement, probability of

technical and commercial achievement for the development plans

are high, and the necessary cost is reliably estimable. Capitalized

costs, comprising direct labor and related overhead, are amortized

by straight-line method over their useful lives. In presentation,

accumulated amortization amount and accumulated impairment

amount are deducted from capitalized costs associated with

development activities.

3) Other intangible assets

Patents, trademarks, software licenses for internal use are

capitalized and amortized using straight-line method over their

useful lives, generally 5 to 10 years. Certain club membership is

regarded as having an indefinite useful life because there is no

foreseeable limit to the period over which the asset is expected to

generate net cash inflows for the entity; such asset is not amortized.

Where an indication of impairment exists, the carrying amount of

any intangible asset is assessed and written down its recoverable

amount.

2.11 Impairment of Non-financial Assets

Assets that have an indefinite useful life, for example goodwill, are

not subject to amortization and are tested annually for impairment.

Assets that are subject to amortization are reviewed for impairment

whenever events or changes in circumstances indicate that the

carrying amount may not be recoverable. An impairment loss is

recognized for the amount by which the asset’s carrying amount

exceeds its recoverable amount. The recoverable amount is the

higher of an asset’s fair value less costs to sell and value in use. For

the purposes of assessing impairment, assets are grouped at the

lowest levels for which there are separately identifiable cash flows

(cash-generating units). Non-financial assets other than goodwill

that suffered impairment are reviewed for possible reversal of the

impairment at each reporting date.

2.12 Borrowings

Borrowings are recognized initially at fair value, net of transaction

costs. Borrowings are subsequently measured at amortized cost;

any difference between cost and the redemption value is recognized

in the statement of income over the period of the borrowings using

the effective interest method. If the Company has an indefinite right

to defer payment for a period longer than 12 months after the end

of the reporting date, such liabilities are recorded as non-current

liabilities. Otherwise, they are recorded as current liabilities.

2.13 Employee Benefits

1) Retirement benefit obligation

The Company has either defined benefit or defined contribution

plans at respective company level. A defined contribution plan is a

pension plan under which the Company pays fixed contributions

into a separate entity. The Company has no legal or constructive

obligations to pay further contributions if the fund does not hold

sufficient assets to pay all employees the benefits relating to

employee service in the current and prior periods. A defined benefit

plan is a pension plan that is not a defined contribution plan.

Typically defined benefit plans define an amount of pension benefit

that an employee will receive on retirement, usually dependent

on one or more factors such as age, years of service and

compensation.

The liability recognized in the statement financial position in respect

of defined benefit pension plans is the present value of the defined

benefit obligation at the end of the reporting period less the fair

value of plan assets, together with adjustments for unrecognized

past-service costs. The defined benefit obligation is calculated

annually by independent actuaries using the projected unit credit

method. The present value of the defined benefit obligation is

determined by discounting the estimated future cash outflows using

interest rates of high-quality corporate bonds that are denominated

in the currency in which the benefits will be paid, and that have

terms to maturity approximating to the terms of the related pension

liability.

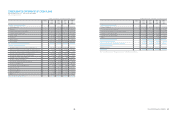

Estimated useful lives

Buildings and auxiliary facilities 15, 30 years

Structures 15 years

Machinery and equipment 5 years

Tools and fixtures 5 years

Vehicles 5 years

Actuarial gains and losses are recognized using the corridor

approach. The company recognizes actuarial gains and losses

in excess of a de minimis over the remaining working lives of

employees. The de minimis amount, which is also referred to as the

‘corridor limit’, is the greater of ten per cent of the present value of

the defined benefit obligation at the end of the previous reporting

period (before deducting plan assets) and ten per cent of the fair

value of any plan assets at that date.

For defined contribution plans, the Company pays contributions on

a mandatory, contractual or voluntary basis. The Company has no

further payment obligations once the contributions have been paid.

The contributions are recognized as employee benefit expense

when they are due. Prepaid contributions are recognized as an

asset to the extent that a cash refund or a reduction in the future

payments is available.

2) Profit-sharing and bonus plans

The Company recognizes a liability and an expense for bonuses

and profit-sharing, based on a formula that takes into consideration

the profit attributable to the company’s shareholders after certain

adjustments. The Company recognizes a provision where

contractually obliged or where there is a past practice that has

created a constructive obligation.

2.14 Provisions

Where there are a number of similar obligations, the likelihood

that an outflow will be required in settlement is determined by

considering the class of obligations as a whole. A provision is

recognized even if the likelihood of an outflow with respect to any

one item included in the same class of obligations may be small.

Provisions are measured at the present value of the expenditures

expected to be required to settle the obligation using a pre-tax rate

that reflects current market assessments of the time value of money

and the risks specific to the obligation. The increase in the provision

due to passage of time is recognized as interest expense.

When there is a probability that an outflow of economic benefits will

occur due to a present obligation resulting from a past event, and

whose amount is reasonably estimable, a corresponding amount of

provision is recognized in the financial statements. However, when

such outflow is dependent upon a future event, is not certain to

occur, or cannot be reliably estimated, a disclosure regarding the

contingent liability is made in the notes to the financial statements.

2.15 Leases

The Company leases certain property, plant and equipment.

Lease of property, plant and equipment where the Company has

substantially all the risks and rewards of ownership are classified

as finance leases. Finance leases are capitalized at the lease’s

commencement at the lower of the fair value of the leased property

and the present value of the minimum lease payments. Each lease

payment is allocated between the liability and finance charges

so as to achieve a constant rate on the outstanding balance.

The corresponding rental obligations, net of finance charges, are

included in other long-term payables. The interest element of the

finance cost is charged to the statement of income over the lease

period so as to produce a constant periodic rate of interest on the

remaining balance of the liability for each period. The property, plant

and equipment acquired under finance leases is depreciated over

the shorter of the useful life of the asset and the lease term.

Leases in which a significant portion of the risks and rewards of

ownership are retained by the lessor are classified as operating

leases. Payments made under operating leases (net of any incentives

received from the lessor) are charged to the statement of income on

a straight-line basis over the period of the lease.

2.16 Derivative Instruments

All derivative instruments are accounted for at fair value with the

resulting valuation gain or loss recorded as an asset or liability. If the

derivative instrument is not designated as a hedging instrument, the

gain or loss is recognized in the statement of income in the period

of change.

Fair value hedge accounting is applied to a derivative instrument

with the purpose of hedging the exposure to changes in the

fair value of an asset or a liability or a firm commitment (hedged

item) that is attributable to a particular risk. Hedge accounting is

applied when the derivative instrument is designated as a hedging

instrument and the hedge accounting criteria have been met. The

gain or loss, both on the hedging derivative instrument and on

the hedged item attributable to the hedged risk, is reflected in the

statement of income.

2.17 Dividend Distribution

Dividend distribution to SEC’s shareholders is recognized as a

liability in the Company’s consolidated financial statements in the

period in which the dividends are declared.

2.18 Share-based Compensation

The Company uses the fair-value method in determining

compensation costs of stock options granted to its employees and

directors. The compensation cost is estimated using the Black-

Scholes option-pricing model and is accrued and charged to

expense over the vesting period, with a corresponding increase in a

separate component of equity.

2.19 Revenue Recognition

Revenue comprises the fair value of the consideration received or

receivable for the sale of goods and services in the ordinary course

of the Company’s activities. Revenue is shown net of value-added

tax, returns, rebates and discounts and after eliminating sales within

the Company.

The Company recognizes revenue when specific recognition

criteria have been met for each of the Company’s activities as

described below. The Company bases its estimates on historical

results, taking into consideration the type of customer, the type of

transaction and the specifics of each arrangement.