Proctor and Gamble 2016 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2016 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

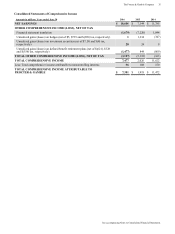

|

|

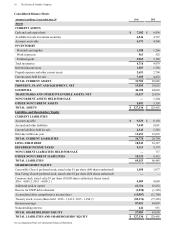

28 The Procter & Gamble Company

The costs of determinable-lived intangible assets are amortized

to expense over their estimated lives. The value of indefinite-

lived intangible assets and residual goodwill is not amortized,

but is tested at least annually for impairment. Our impairment

testing for goodwill is performed separately from our

impairment testing of indefinite-lived intangible assets. We

test goodwill for impairment by reviewing the book value

compared to the fair value at the reporting unit level. We test

individual indefinite-lived intangible assets by comparing the

book values of each asset to the estimated fair value. We

determine the fair value of our reporting units and indefinite-

lived intangible assets based on the income approach. Under

the income approach, we calculate the fair value of our

reporting units and indefinite-lived intangible assets based on

the present value of estimated future cash flows. Considerable

management judgment is necessary to evaluate the impact of

operating and macroeconomic changes and to estimate future

cash flows to measure fair value. Assumptions used in our

impairment evaluations, such as forecasted growth rates and

cost of capital, are consistent with internal projections and

operating plans. We believe such assumptions and estimates

are also comparable to those that would be used by other

marketplace participants.

Most of our goodwill reporting units are comprised of a

combination of legacy and acquired businesses and as a result

have fair value cushions that, at a minimum, exceed two times

their underlying carrying values. Certain of our continuing

goodwill reporting units, in particular Shave Care and

Appliances, are comprised entirely of acquired businesses and

as a result have fair value cushions that are not as high. While

both of these wholly-acquired reporting units have fair value

cushions that currently exceed the underlying carrying values,

the Shave Care cushion, as well as certain of the related

indefinite-lived intangible assets, have been reduced to below

20% due in large part to significant currency devaluations in

a number of countries relative to the U.S. dollar that began in

recent years and continued during fiscal 2016. As a result, this

unit is more susceptible to impairment risk from adverse

changes in business operating plans and macroeconomic

environment conditions, including any further significant

devaluation of major currencies relative to the U.S. dollar. Any

such adverse changes in the future could reduce the underlying

cash flows used to estimate fair values and could result in a

decline in fair value that could trigger future impairment

charges of the business unit's goodwill and indefinite-lived

intangibles.

The business unit valuations used to test goodwill and

intangible assets for impairment are dependent on a number of

significant estimates and assumptions, including

macroeconomic conditions, overall category growth rates,

competitive activities, cost containment and margin expansion

and Company business plans. We believe these estimates and

assumptions are reasonable. Changes to, or a failure to, achieve

these business plans or a further deterioration of the

macroeconomic conditions could result in a valuation that

would trigger an impairment of the goodwill and intangible

assets of these businesses.

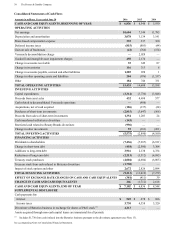

See Note 4 to the Consolidated Financial Statements for

additional discussion on goodwill and intangible asset

impairment testing results.

New Accounting Pronouncements

Refer to Note 1 to the Consolidated Financial Statements for

recently adopted accounting pronouncements and recently

issued accounting pronouncements not yet adopted as of

June 30, 2016.

OTHER INFORMATION

Hedging and Derivative Financial Instruments

As a multinational company with diverse product offerings,

we are exposed to market risks, such as changes in interest

rates, currency exchange rates and commodity prices. We

evaluate exposures on a centralized basis to take advantage of

natural exposure correlation and netting. Except within

financing operations, we leverage the Company's diversified

portfolio of exposures as a natural hedge and prioritize

operational hedging activities over financial market

instruments. To the extent we choose to further manage

volatility associated with the net exposures, we enter into

various financial transactions which we account for using the

applicable accounting guidance for derivative instruments and

hedging activities. These financial transactions are governed

by our policies covering acceptable counterparty exposure,

instrument types and other hedging practices. See Note 9 to

the Consolidated Financial Statements for a discussion of our

accounting policies for derivative instruments.

Derivative positions are monitored using techniques including

market valuation, sensitivity analysis and value-at-risk

modeling. The tests for interest rate, currency rate and

commodity derivative positions discussed below are based on

the CorporateManager™ value-at-risk model using a one-year

horizon and a 95% confidence level. The model incorporates

the impact of correlation (the degree to which exposures move

together over time) and diversification (from holding multiple

currency, commodity and interest rate instruments) and

assumes that financial returns are normally distributed.

Estimates of volatility and correlations of market factors are

drawn from the RiskMetrics™ dataset as of June 30, 2016. In

cases where data is unavailable in RiskMetrics™, a reasonable

proxy is included.

Our market risk exposures relative to interest rates, currency

rates and commodity prices, as discussed below, have not

changed materially versus the previous reporting period. In

addition, we are not aware of any facts or circumstances that

would significantly impact such exposures in the near term.

Interest Rate Exposure on Financial Instruments. Interest

rate swaps are used to hedge exposures to interest rate

movement on underlying debt obligations. Certain interest rate

swaps denominated in foreign currencies are designated to

hedge exposures to currency exchange rate movements on our

investments in foreign operations. These currency interest rate

swaps are designated as hedges of the Company's foreign net

investments.