Proctor and Gamble 2016 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2016 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

26 The Procter & Gamble Company

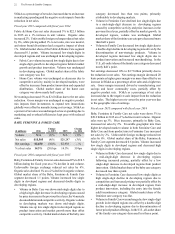

Contractual Commitments

The following table provides information on the amount and payable date of our contractual commitments as of June 30, 2016.

Amounts in millions Total Less Than 1 Year 1-3 Years 3-5 Years After 5 Years

RECORDED LIABILITIES

Total debt $ 30,221 $ 11,635 $ 3,660 $ 3,467 $ 11,459

Capital leases 45 16 21 5 3

Uncertain tax positions

(1)

247 247———

OTHER

Interest payments relating to long-term debt 6,439 684 1,249 979 3,527

Operating leases

(2)

1,563 237 464 360 502

Minimum pension funding

(3)

640 215 425 — —

Purchase obligations

(4)

1,794 881 391 234 288

TOTAL CONTRACTUAL COMMITMENTS $ 40,949 $ 13,915 $ 6,210 $ 5,045 $ 15,779

(1)

As of June 30, 2016, the Company's Consolidated Balance Sheet reflects a liability for uncertain tax positions of $1.2 billion, including

$343 million of interest and penalties. Due to the high degree of uncertainty regarding the timing of future cash outflows of liabilities for

uncertain tax positions beyond one year, a reasonable estimate of the period of cash settlement beyond twelve months from the balance

sheet date of June 30, 2016, cannot be made.

(2)

Operating lease obligations are shown net of guaranteed sublease income.

(3)

Represents future pension payments to comply with local funding requirements. These future pension payments assume the Company

continues to meet its future statutory funding requirements. Considering the current economic environment in which the Company operates,

the Company believes its cash flows are adequate to meet the future statutory funding requirements. The projected payments beyond fiscal

year 2019 are not currently determinable.

(4)

Primarily reflects future contractual payments under various take-or-pay arrangements entered into as part of the normal course of business.

Commitments made under take-or-pay obligations represent future purchases in line with expected usage to obtain favorable pricing. This

includes service contracts for information technology, human resources management and facilities management activities that have been

outsourced. While the amounts listed represent contractual obligations, we do not believe it is likely that the full contractual amount would

be paid if the underlying contracts were canceled prior to maturity. In such cases, we generally are able to negotiate new contracts or

cancellation penalties, resulting in a reduced payment. The amounts do not include other contractual purchase obligations that are not take-

or-pay arrangements. Such contractual purchase obligations are primarily purchase orders at fair value that are part of normal operations

and are reflected in historical operating cash flow trends. We do not believe such purchase obligations will adversely affect our liquidity

position.

SIGNIFICANT ACCOUNTING POLICIES AND

ESTIMATES

In preparing our financial statements in accordance with U.S.

GAAP, there are certain accounting policies that may require

a choice between acceptable accounting methods or may

require substantial judgment or estimation in their application.

These include income taxes, certain employee benefits and

goodwill and intangible assets. We believe these accounting

policies, and others set forth in Note 1 to the Consolidated

Financial Statements, should be reviewed as they are integral

to understanding the results of operations and financial

condition of the Company.

The Company has discussed the selection of significant

accounting policies and the effect of estimates with the Audit

Committee of the Company's Board of Directors.

Income Taxes

Our annual tax rate is determined based on our income,

statutory tax rates and the tax impacts of items treated

differently for tax purposes than for financial reporting

purposes. Also inherent in determining our annual tax rate are

judgments and assumptions regarding the recoverability of

certain deferred tax balances, primarily net operating loss and

other carryforwards, and our ability to uphold certain tax

positions.

Realization of net operating losses and other carryforwards is

dependent upon generating sufficient taxable income in the

appropriate jurisdiction prior to the expiration of the

carryforward periods, which involves business plans, planning

opportunities and expectations about future outcomes.

Although realization is not assured, management believes it is

more likely than not that our deferred tax assets, net of valuation

allowances, will be realized.

We operate in multiple jurisdictions with complex tax policy

and regulatory environments. In certain of these jurisdictions,

we may take tax positions that management believes are

supportable, but are potentially subject to successful challenge

by the applicable taxing authority. These interpretational

differences with the respective governmental taxing authorities

can be impacted by the local economic and fiscal environment.

Our operating principles are that our tax structure is based on

our business operating model, such that profits are earned in

line with the business substance and functions of the various

legal entities. However, we may have income tax exposure

related to the determination of the appropriate transfer prices