Pottery Barn 2007 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2007 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

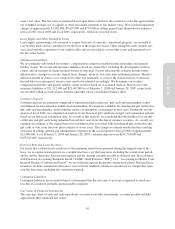

Memphis-Based Distribution Facilities Obligation

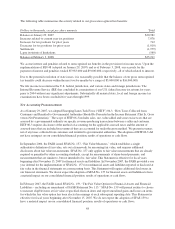

See Note F for a discussion on our bond-related debt pertaining to our Memphis-based distribution facilities.

Mississippi Industrial Development Bonds

In June 2004, in an effort to utilize tax incentives offered to us by the state of Mississippi, we entered into an

agreement whereby the Mississippi Business Finance Corporation issued $15,000,000 in long-term variable rate

industrial development bonds, the proceeds, net of debt issuance costs, of which were loaned to us to finance the

acquisition and installation of leasehold improvements and equipment located in our Olive Branch, Mississippi

distribution center. The bonds are marketed through a remarketing agent and are secured by a letter of credit

issued under our $300,000,000 line of credit facility. The bonds mature on June 1, 2024. The bond rate resets

each week based upon current market rates. The rate in effect at February 3, 2008 was 3.4%.

The bond agreement allows for each bondholder to tender their bonds to the trustee for repurchase, on demand, with

seven days advance notice. In the event the remarketing agent fails to remarket the bonds, the trustee will draw upon

the letter of credit to fund the purchase of the bonds. As of February 3, 2008, $13,150,000 remained outstanding on

these bonds and was classified as current debt. The bond proceeds were restricted for use in the acquisition and

installation of leasehold improvements and equipment located in our Olive Branch, Mississippi distribution center.

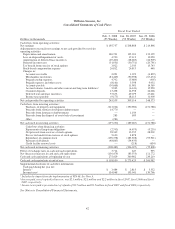

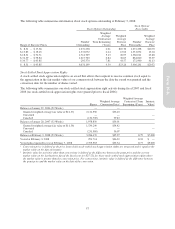

The aggregate maturities of long-term debt at February 3, 2008 were as follows:

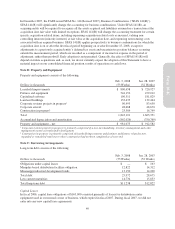

Dollars in thousands

Fiscal 2008 $14,734

Fiscal 2009 1,438

Fiscal 2010 1,461

Fiscal 2011 1,414

Fiscal 2012 1,535

Thereafter 5,390

Total $25,972

Credit Facility

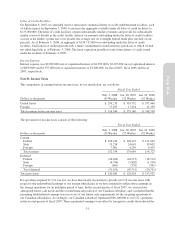

As of February 3, 2008, we have a credit facility that provides for a $300,000,000 unsecured revolving line of credit

that may be used for loans or letters of credit and contains certain financial covenants, including a maximum

leverage ratio (funded debt adjusted for lease and rent expense to EBITDAR), and covenants limiting our ability to

dispose of assets, make acquisitions, be acquired, incur indebtedness, grant liens and make investments. Prior to

April 4, 2011, we may, upon notice to the lenders, request an increase in the new credit facility of up to

$200,000,000, to provide for a total of $500,000,000 of unsecured revolving credit. The credit facility contains

events of default that include, among others, non-payment of principal, interest or fees, violation of covenants,

inaccuracy of representations and warranties, bankruptcy and insolvency events, material judgments, cross defaults

to certain other indebtedness and events constituting a change of control. The occurrence of an event of default will

increase the applicable rate of interest by 2.0% and could result in the acceleration of our obligations under the

credit facility and an obligation of any or all of our U.S. subsidiaries to pay the full amount of our obligations under

the credit facility. The credit facility matures on October 4, 2011, at which time all outstanding borrowings must be

repaid and all outstanding letters of credit must be cash collateralized.

We may elect interest rates calculated at Bank of America’s prime rate (or, if greater, the average rate on

overnight federal funds plus one-half of one percent) or LIBOR plus a margin based on our leverage ratio.

During fiscal 2007, we had borrowings under the credit facility of $189,000,000, however, no amounts were

outstanding under the credit facility as of February 3, 2008. No amounts were borrowed under the credit facility

in fiscal 2006. As of February 3, 2008, $36,229,000 in issued but undrawn standby letters of credit was

outstanding under the credit facility. The standby letters of credit were issued to secure the liabilities associated

with workers’ compensation, other insurance programs and certain debt transactions. As of February 3, 2008, we

were in compliance with our financial covenants under the credit facility.

50