Pottery Barn 2004 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2004 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

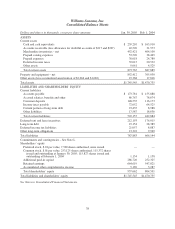

|

|

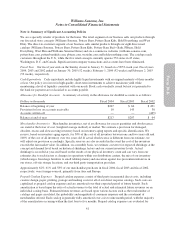

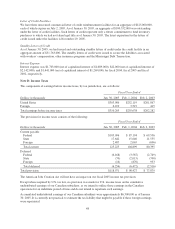

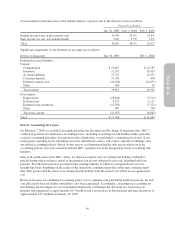

realizability on a monthly basis by comparing the carrying amount associated with each catalog to the estimated

probable remaining future profitability (remaining net revenues less merchandise cost of goods sold, selling

expenses and catalog related-costs) associated with that catalog. If the catalog is not expected to be profitable, the

carrying amount of the catalog is impaired accordingly. Catalog advertising expenses were $278,169,000,

$250,337,000 and $205,792,000 in fiscal 2004, fiscal 2003 and fiscal 2002, respectively.

Property and Equipment Property and equipment are stated at cost. Depreciation is computed using the

straight-line method over the estimated useful lives of the assets below. Any reduction in the estimated lives

would result in higher depreciation expense for the related assets.

Leasehold improvements

Shorter of estimated useful life or lease term

(generally 3 – 22 years)

Fixtures and equipment 2 – 20 years

Buildings and building improvements 12 – 40 years

Capitalized software 2 – 10 years

Corporate aircraft 20 years (20% salvage value)

Capital leases

Shorter of estimated useful life or lease term

(generally 4 – 5 years)

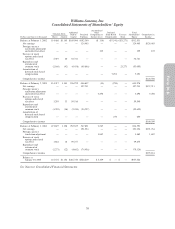

Internally developed software costs are capitalized in accordance with American Institute of Certified Public

Accountants Statement of Position 98-1, “Accounting for the Costs of Computer Software Developed or

Obtained for Internal Use.”

Interest costs related to assets under construction and software projects are capitalized during the construction or

development period. We capitalized interest costs of $1,689,000, $2,142,000 and $1,269,000 in fiscal 2004, fiscal

2003 and fiscal 2002, respectively.

For any early store closures where a lease obligation still exists, we record the estimated future liability

associated with the rental obligation on the date the store is closed in accordance with Statement of Financial

Accounting Standards (“SFAS”) No. 146, “Accounting for Costs Associated with Exit or Disposal Activities.”

However, most store closures occur upon the lease expiration.

We review the carrying value of all long-lived assets for impairment whenever events or changes in

circumstances indicate that the carrying value of an asset may not be recoverable. In accordance with SFAS No.

144, “Accounting for the Impairment or Disposal of Long-Lived Assets,” we review for impairment all stores for

which current cash flows from operations are negative or the construction costs are significantly in excess of the

amount originally expected. Impairment results when the carrying value of the assets exceeds the undiscounted

future cash flows over the life of the lease. Our estimate of undiscounted future cash flows over the lease term

(typically 5 to 22 years) is based upon our experience, historical operations of the stores and estimates of future

store profitability and economic conditions. The future estimates of store profitability and economic conditions

require estimating such factors as sales growth, employment rates, lease escalations, inflation on operating

expenses and the overall economics of the retail industry for up to twenty years in the future, and are therefore

subject to variability and difficult to predict. If a long-lived asset is found to be impaired, the amount recognized

for impairment is equal to the difference between the carrying value and the asset’s fair value. The fair value is

estimated based upon future cash flows (discounted at a rate that approximates our weighted average cost of

capital) or other reasonable estimates of fair market value.

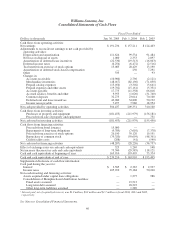

Lease Rights and Other Intangible Assets Lease rights, representing costs incurred to acquire the lease of a

specific commercial property, are recorded at cost in other assets and are amortized over the lives of the

respective leases. Other intangible assets include fees associated with the acquisition of our credit facility and are

recorded at cost in other assets and amortized over the life of the facility.

Self-Insured Liabilities We are primarily self-insured for workers’ compensation, employee health benefits and

product and general liability insurance. We record self-insurance liabilities based on claims filed, including the

42