Pottery Barn 2004 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2004 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

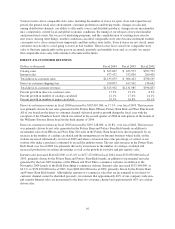

inventory over two years old. If actual obsolescence is different from our estimate, we will adjust our provision

accordingly. Specific reserves are also recorded in the event the cost of the inventory exceeds the fair market

value. In addition, on a monthly basis, we estimate a reserve for expected shrinkage at the concept and channel

level based on historical shrinkage factors and our current inventory levels. Actual shrinkage is recorded at year-

end based on the results of our physical inventory count and can vary from our estimates due to such factors as

changes in operations within our distribution centers, the mix of our inventory (which ranges from large furniture

to small tabletop items) and execution against loss prevention initiatives in our stores, off-site storage locations,

and our third party transportation providers.

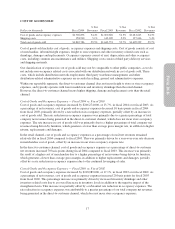

Prepaid Catalog Expenses

Prepaid catalog expenses consist of third party incremental direct costs, including creative design, paper,

printing, postage and mailing costs for all of our direct response catalogs. Such costs are capitalized as prepaid

catalog expenses and are amortized over their expected period of future benefit. Such amortization is based upon

the ratio of actual revenues to the total of actual and estimated future revenues on an individual catalog basis.

Estimated future revenues are based upon various factors such as the total number of catalogs and pages

circulated, the probability and magnitude of consumer response and the assortment of merchandise offered. Each

catalog is generally fully amortized over a six to nine month period, with the majority of the amortization

occurring within the first four to five months. Prepaid catalog expenses are evaluated for realizability on a

monthly basis by comparing the carrying amount associated with each catalog to the estimated probable

remaining future profitability (remaining net revenues less merchandise cost of goods sold, selling expenses and

catalog related-costs) associated with that catalog. If the catalog is not expected to be profitable, the carrying

amount of the catalog is impaired accordingly.

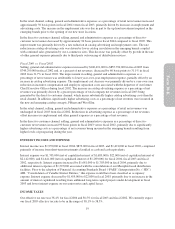

Property and Equipment

Depreciation is computed using the straight-line method over the estimated useful lives of the assets. The

decision to close, relocate, remodel or expand a store prior to the end of its lease term can result in accelerated

depreciation over the revised useful life of the long-lived assets. For any early store closures where a lease

obligation still exists, we record the estimated future liability associated with the rental obligation on the date the

store is closed in accordance with Statement of Financial Accounting Standards (“SFAS”) No. 146, “Accounting

for Costs Associated with Exit or Disposal Activities.” However, most store closures occur upon the lease

expiration.

We review the carrying value of all long-lived assets for impairment whenever events or changes in

circumstances indicate that the carrying value of an asset may not be recoverable. In accordance with SFAS No.

144, “Accounting for the Impairment or Disposal of Long-Lived Assets,” we review for impairment all stores for

which current cash flows from operations are negative or the construction costs are significantly in excess of the

amount originally expected. Impairment results when the carrying value of the assets exceeds the undiscounted

future cash flows over the life of the lease. Our estimate of undiscounted future cash flows over the lease term

(typically 5 to 22 years) is based upon our experience, historical operations of the stores and estimates of future

store profitability and economic conditions. The future estimates of store profitability and economic conditions

require estimating such factors as sales growth, employment rates, lease escalations, inflation on operating

expenses and the overall economics of the retail industry for up to twenty years in the future, and are therefore

subject to variability and difficult to predict. If a long-lived asset is found to be impaired, the amount recognized

for impairment is equal to the difference between the carrying value and the asset’s fair value. The fair value is

estimated based upon future cash flows (discounted at a rate that approximates our weighted average cost of

capital) or other reasonable estimates of fair market value. See Note A to the Consolidated Financial Statements

for additional information regarding property and equipment.

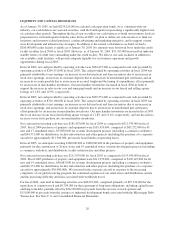

Self-Insured Liabilities

We are primarily self-insured for workers’ compensation, employee health benefits and product and general

liability insurance. We record self-insurance liabilities based on claims filed, including the development of those

claims, and an estimate of claims incurred but not yet reported. Factors affecting this estimate include future

inflation rates, changes in severity, benefit level changes, medical costs, and claim settlement patterns. Should a

26