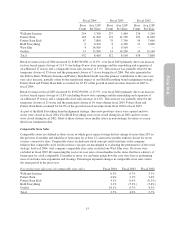

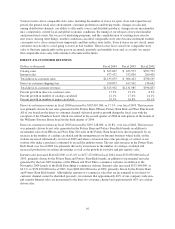

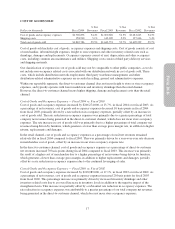

Pottery Barn 2004 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2004 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

The operating lease for this distribution facility requires us to pay annual rent of $618,000 plus interest on the

bonds calculated at a variable rate determined monthly (2.3% in January 2005), applicable taxes, insurance and

maintenance expenses. Although the current term of the lease expires in August 2005, we are obligated to renew

the operating lease until these bonds are fully repaid.

Our other Memphis-based distribution facility includes an operating lease entered into in August 1990 for

another distribution facility that is adjoined to the Partnership 1 facility in Memphis, Tennessee. The lessor is a

general partnership (“Partnership 2”) comprised of W. Howard Lester, James A. McMahan and two unrelated

parties. Partnership 2 does not have operations separate from the leasing of this distribution facility and does not

have lease agreements with any unrelated third parties.

Partnership 2 financed the construction of this distribution facility and related addition through the sale of a total

of $24,000,000 of industrial development bonds in 1990 and 1994. Quarterly interest and annual principal

payments are required through maturity in August 2015. The Partnership 2 industrial development bonds are

collateralized by the distribution facility and require us to maintain certain financial covenants. As of January 30,

2005, $14,659,000 was outstanding under the Partnership 2 industrial development bonds.

The operating lease for this distribution facility requires us to pay annual rent of approximately $2,600,000, plus

applicable taxes, insurance and maintenance expenses. This operating lease has a term of 15 years expiring in

August 2006, with three optional five-year renewal periods. We are, however, obligated to renew the lease until

the bonds are fully repaid.

As of February 1, 2004, the Company adopted FIN 46R, which requires existing unconsolidated variable interest

entities to be consolidated by their primary beneficiaries if the entities do not effectively disperse risks among

parties involved. The two partnerships described above qualify as variable interest entities under FIN 46R due to

their related party relationship and our obligation to renew the leases until the bonds are fully repaid.

Accordingly, the two related party variable interest entity partnerships from which we lease our Memphis-based

distribution facilities were consolidated by us as of February 1, 2004. As of January 30, 2005, the consolidation

had resulted in increases to our consolidated balance sheet of $18,882,000 in assets (primarily buildings),

$17,000,000 in long-term debt, and $1,882,000 in other long-term liabilities. Consolidation of these partnerships

did not have an impact on our net income. However, the interest expense associated with the partnerships’ long-

term debt, shown as occupancy expense in fiscal 2003, is now recorded as interest expense. In fiscal 2004, this

interest expense approximated $1,525,000.

IMPACT OF INFLATION

The impact of inflation on our results of operations for the past three fiscal years has not been significant.

CRITICAL ACCOUNTING POLICIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations is based on our

consolidated financial statements, which have been prepared in accordance with accounting principles generally

accepted in the United States of America. The preparation of these financial statements requires us to make

estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses and related

disclosures of contingent assets and liabilities. The estimates and assumptions are evaluated on an on-going basis

and are based on historical experience and various other factors that we believe to be reasonable under the

circumstances. Actual results may differ significantly from these estimates.

We believe the following critical accounting policies affect the significant judgments and estimates used in the

preparation of our consolidated financial statements.

Merchandise Inventories

Merchandise inventories, net of an allowance for excess quantities and obsolescence, are stated at the lower of

cost (weighted average method) or market. We estimate a provision for damaged, obsolete, excess and slow-

moving inventory based on inventory aging reports and specific identification. We reserve, based on inventory

aging reports, for 50% of the cost of all inventory between one and two years old and 100% of the cost of all

25

Form 10-K